|

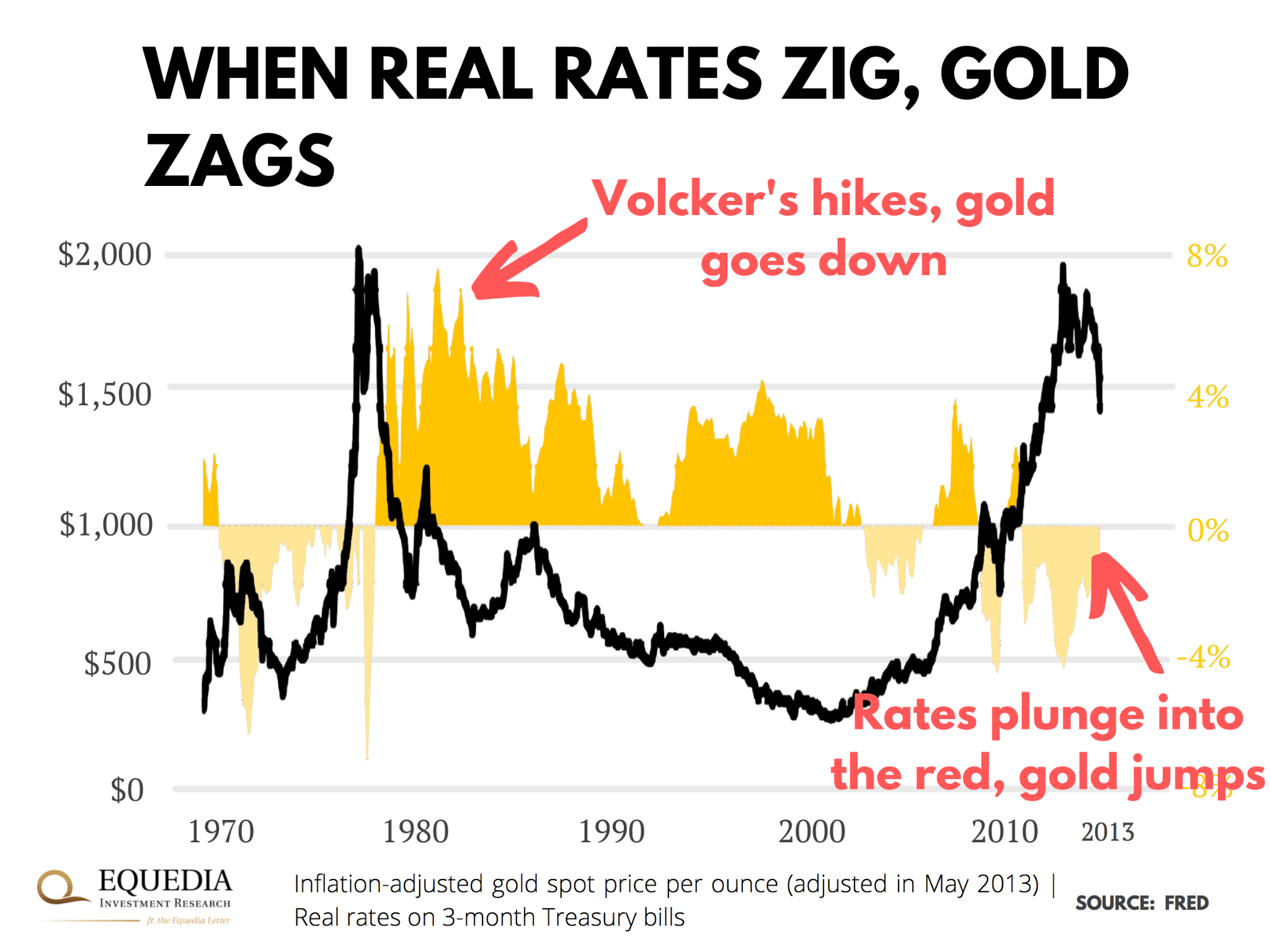

See where Volcker's hikes brought the rates out of the red… and how gold crashed soon after? Or how negative rates after 2000 launched gold into the biggest rally since the '70s?

This gold-rate affair may sound complicated, but...

It all comes down to common sense

Like any other asset class, gold fights for a place in the portfolio with other investments. But unlike most investments, gold doesn't generate earnings or income.

That means holding this metal comes with higher opportunity costs. Or put another way, the more you earn from, say, stocks or bonds, the less you want to invest in a metal that doesn't earn a thing.

This is where real rates come in.

When real interest rates grow, so do bond interest and investors' income from this asset class.

As the appeal of bonds grows, investors move more of their portfolios to this asset class. In turn, demand for gold falls and so does its price.

And vice versa.

If real rates go down (or sink into the red like today), bond investors lose money. So they naturally rebalance to other asset classes—including gold—and bid up their prices.

And that brings us to the most important question at hand...

Where are real rates headed?

To answer it, we first have to understand why central banks fiddle with rates in the first place.

As you may know, interest rates are one of the three tools in a central banker's toolbox. They use them to control the price of money, which lets them stimulate or cool off the economy as needed.

Here's how it works.

When the central bank raises rates, it props up interest on all debt. As a result, the cost of borrowing money goes up. In turn, spending goes down, and the economy slows.

Now, when rates drop, so do borrowing costs. More people and businesses can borrow money for cheap. They lease cars, take out mortgages, and otherwise spend it, which props up the economy.

Think the housing boom after the Fed's rate cuts during Covid...

So, where does this leave us today?

Inflation is rising. And many estimates show that consumer prices will keep marching higher for the coming years.

Meanwhile, real interest rates are the lowest since the 1970s. Even the riskiest junk bonds earn negative real interest. That's nuts. Investors are essentially losing money even by risking it on garbage companies.

Not much appeal in bonds, I would say.

Are rates coming back up anytime soon? Probably not.

The Fed pledged to keep rates at the ground floor well into 2023. The Bank of Canada isn't crazy about raising rates either - especially if the U.S. holds still. And when the economy is so fragile, no central banker is in the mood for pulling off surprises.

That means that, at the very least, there won't be any significant hikes before the end of 2022.

Even after that, central bankers will be very, very cautious about raising rates - especially if politicians have their way.

Of course, the flip side is trying to understand what the Bankers really have planned for us.

In the past, these bankers flexed their muscles by contracting the money supply (raising rates). If the politicians in power weren't bending to the will of the Bankers, most notably to renew central bank charters, the Bankers would flex. Contract the money supply and you contract the economy. This flex led to the Federal Reserve central banking system - a system that gave the Bankers carte blanche control over the world's biggest monetary system.

Where does that leave us today?

The Bankers already have full control of the monetary system and the biggest governments around the world owe them trillions upon trillions of dollars. Surely they don't want to collapse the financial system they built. Surely they don't want people to lose faith in their dollars.

Or perhaps they're going after the "Great Reset" we talked about in a previous letter.

The world has amassed the biggest mountain of debt in history (relative to GDP).

The stock market is as leveraged as ever, and so is housing.

National deficits are through the roof.

Imagine the domino chain of defaults higher rates could set off. And who would be willing to take the blame for it?

This is why we believe real rates aren't going anywhere significant anytime soon. And that means there's still plenty of upside left for precious metals and stocks tied to them.

And lastly, one could argue that the Bankers' role is diminishing as people fight back via cryptocurrencies such as Bitcoin. But this is a worthless argument today.

Why?

Because today, the Bankers have an unlimited supply of money. And with that, they could easily control the majority supply of Bitcoin. It is mostly anonymous after all, no?

|