Alexco Turns a Corner on Development

posted on

Oct 07, 2008 04:31AM

Managing Risk, Unlocking Value, Emerging Silver Producer.

http://seekingalpha.com/article/9865...

We see the agreement between Alexco Resource Corp. (AXU) and Silver Wheaton Corp. (SLW) as one of the most important deals in 2008. Coming on the day of the U.S. Congress vote on the bailout, the agreement validates Silver Wheaton's confidence for the potential of Alexco's Keno Hill Silver District and outlook for the price of silver.

Alexco's Keno Hill Silver District, Yukon Territory

Source: Alexco

The deal was made even more interesting as it occurred prior to a positive mine decision or completion of a Feasibility Study on Alexco's Bellekeno project. The deal provides Alexco an opportunity to accelerate development at Bellekeno and the district while limiting shareholder dilution. The agreement bypasses the credit and equity markets, allowing Alexco to create value while providing Silver Wheaton potentially tremendous leverage for future production at higher silver prices over the long-term.

Silver Wheaton will purchase 25% of the life of mine silver produced by Alexco from the Keno Hill Silver District, for an up-front payment of US$50 million, at a price of US$3.90 per ounce (increasing by 1% in the third year). US$15 million of the up-front payment will be disbursed in 30 to 90 days, to be used to maintain Alexco's development schedule, and the remaining US$35 million will build out mine infrastructure and a processing facility at Bellekeno. Alexco management anticipates that this should be sufficient to bring the Bellekeno project to production without further need to approach the capital markets. Alexco has budgeted development at Bellekeno to be C$61.2 million, which includes a 25% contingency, with about C$10 million already spent on the underground program.

Alexco's Bellekeno Project, Keno Hill Silver District, Yukon Territory

Source: Alexco

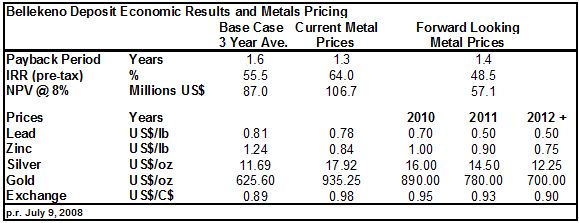

Alexco has received a preliminary economic assessment on the Bellekeno deposit with a base case pre-tax assessment of US$87million (NPV @ 8% discount rate). The assessment estimated average annual production of 3.3 million ounces of silver, 30.1 million pounds of lead, and 24.5 million pounds of zinc over an initial five year mine life. As this includes significant credits for zinc and lead, Alexco management believes the agreement represents less than 15% of the initial revenues from the Bellekeno deposit.

The resource should increase, and mine life should be extended, with exploration drilling from the underground program. From Silver Wheaton's perspective, we suspect that they are anticipating a significantly larger resource to be defined, and in reasonably short order, to make the agreement economic. This demonstrates significant confidence in Alexco management, as well as the Bellekeno project, and the prospects for the district at large.

We believe the Keno Hill Silver District may prove to be one of the world's great silver districts. The district from 1921 to 1988 produced 217 million ounces of silver, with average grades of 40.5 opt silver, 5.6% zinc and 3.1% lead. The district has never been explored comprehensively with modern methods or mined much deeper than several hundred meters. The size of the Keno Hill Silver District and its geology compares favorably to Idaho's Silver Valley, which has produced well over a billion ounces of silver, and in some areas has been mined to depths of over 5,000 feet. Clearly, should the development of Keno Hill equal even a fraction of the Silver Valley, Silver Wheaton shareholders may in time be greatly rewarded.

What Alexco may have given up in terms of long-term silver production, they may have more than made up in maintaining an aggressive construction schedule and by not diluting shareholders during a period of low equity prices and distressed markets. They retain 75% of silver production to be sold at market prices (and the remaining 25% of silver production at US$3.90 per ounce), plus revenues from zinc and lead. We also note that there are several gold placer operations in the Keno Hill Silver District. This suggests potential upside for further hard rock gold deposits. Alexco management also remains in control of the development timing of the balance of the district.

Silver Wheaton and Alexco benefit from Alexco's unique role as the sole provider of environmental remediation of the district for the government in the Yukon Territory. This increases the speed and flexibility in which they may explore and permit projects within the district. While both Alexco and Silver Wheaton have given up either cash or future production to enter into the agreement, it would appear to us that by maintaining the development schedule and accelerating development of the district, both should gain from the increase in value in the near term.

It would appear that Alexco is significantly undervalued. The current market capitalization of Alexco is approximately $61.2 million. This is less than the base case preliminary economic assessment value of $87 million for the Bellekeno project. This estimate includes only the current defined resource (from surface drilling alone), and does not include subsequently defined Onek resource, potential of the Lucky Queen target, or balance of the district. This also does not include value which may be attributed to Alexco's environmental business, the contract for clean-up of the Keno Hill Silver District, or its proprietary environmental patents.

We applaud the management of Alexco and Silver Wheaton for concluding the agreement. Completed at a time of market paralysis, it demonstrates focus and attention to business at a time of great confusion, pessimism, and distraction. Investors interested in Alexco should note progress in the development at Bellekeno, as well as exploration at the project and elsewhere at Keno Hill, and their environmental business.