Silex Systems: The Future Of The Uranium Enrichment Industry

posted on

Jun 06, 2013 08:03AM

A premier intermediate uranium producer in North America

Disclosure: I am long SILXY.PK, SILXF.PK, USU. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

Silex Systems (SILXY.PK SILXF.PK) is an Australian based alternative energy company. The company operates four primary divisions: Laser uranium enrichment, solar, translucent and chronologic.

I've written about the uranium enrichment industry before regarding USEC here and here.

Below is a brief description of each of Silex's divisions from a recent investor presentation:

The primary industry to focus on is uranium enrichment.

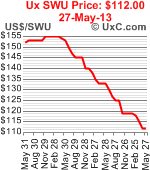

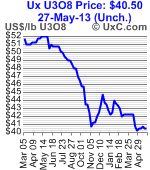

Over the last year SWU prices have declined by over 50% which has been slightly more precipitous than the price decline in uranium (U3O8). But according to the vast majority of analysts, this decline is only temporary.

JPMorgan for example recently revised its spot price forecast to "US$43 per pound in 2013 (US$46 previously), US$58 in 2014 (from US$60), US$70 in 2015 (from US$90) and US$90 in 2016 (from US$70)," and noted that "despite this push out, we have a favorable outlook for uranium over the long term due to relatively predictable demand and high inducement prices, which are limiting supply growth."

According to JPMorgan uranium prices are projected to more than double in the next 3 years. Part of this is due to demand. There are currently 434 operable nuclear reactors worldwide with 64 under construction and another 160 planned. The other part is due to supply as the industry is not investing in additional capacity currently due to lower uranium prices.

SWU prices will likely increase even further than uranium due to the upcoming decommissioning of USEC's Paducah's gaseous diffusion plant.

All of this is good news for Silex as GLE (Global Laser Enrichment), which licenses the laser technology from them, only plans to begin construction for the initial commercial plant sometime in 2014. The first plant is being planned for Wilmington, NC, and is expected to have a capacity of 6 million SWU. At a conservative SWU price of $125, GLE at max capacity would have revenues of $750 million per year from this facility. Silex would receive royalties of between 7-12% ($50m - $90m).

There is a potential that GLE will be able to utilize Silex's technology even sooner as they are in the processing of submitting a bid for DOE's Paducah plant which USEC is in the process of leaving. Originally it looked like USEC (USU) may stay at the facility longer or bid for the facility, but considering the lawsuit which they filed today it looks like they will not even be considered as a potential bidder. This will shorten the already very short list of potential bidders for the facility. If GLE does win it could be a big catalyst for Silex.

Silex's market cap is currently around $400 million and has about $90m of cash on hand with no debt. Revenues are around $6 million but should increase in the near term due to the expected completion of several solar projects this year. It also receives milestone payments for several projects. For example in April it will receive a $15m milestone payment related to laser technology for uranium enrichment.

If you were just buying the uranium unit alone the company would be an interesting investment opportunity and the current valuation could be somewhat justified. But when you factor in the company's solar and other businesses it becomes clear that the current valuation offers some downside protection and major upside potential.

The company is currently in the planning stages for a 100 MW solar facility with the Australian government expected to contribute $110 million of the development cost.

Overall there is a lot to be excited about Silex.

There are many upcoming potential catalysts such as milestone payments and news on the development on the GLE uranium plant and the Midura solar facility.

It is also important to note that North American institutional investors currently only make up 2% of shareholders in the company. Considering the strong relationship with U.S. based General Electric (GE) and Canadian based Cameco (CCJ) it is likely that more North American institutions will want to invest in the company in the future.

One additional risk to note is that investors are exposing themselves to the Australian dollar through this investment. I personally look at this as a positive as I was looking to further diversify my currency exposures.