The definition of the invisible hand may have changed, but it is still the market that reacts on extremes. Below three excellent analyses by Eric de Groot.

Thursday, May 3, 2012

How bad has the gold shares under performance to gold been since 2010? The first response might be bad, but the the correct observation should be extreme.

- The gold shares to gold ratio produced 4.3 cycle Z-score reading of -2.35. This suggests severe under performance of the gold shares relative to gold through May 2012.

- This reading is the lowest reading since 2007.05 and seventh lowest since 1922.

- +/-1.96 implies a data point that exceeds 97.5% of the readings over the past 4.3 years assuming a normal distribution. A -2.35 reading pushes this percentage above 99%.

- The lowest 4.3 cycle reading was -3.22 and was generated in 1940. This was followed by one of the lowest 8.6 cycle readings of -2.27 in 1942. The lowest combined 4.3 and 8.6 cycle readings of -2.97 and -2.77 was generated in 1973. This was a majority entry point for gold share investors. A similar combined reading of -2.01 and -2.80 was generated in late 2008. This was also a major entry point for long-term gold share investors.

- The extreme under performance of the gold shares has been driven by either intense emotional selling or a flight of capital ahead of yet another shock within the evolving sovereign debt crisis. For example, the extreme under performance of gold in mid 2007 which produced a Z-score reading of -2.33 represented a flight of capital from the gold shares (risk) to gold (risk aversion). The extreme readings of 2007 and 2008 preceded the financial crisis of late 2008. Cycles work, however, places the next shock within the global crisis between late 2015 to early 2016, so probabilities favor intense emotional selling rather than flight of capital. This suggest a comparison to 1978 rather than 2007.

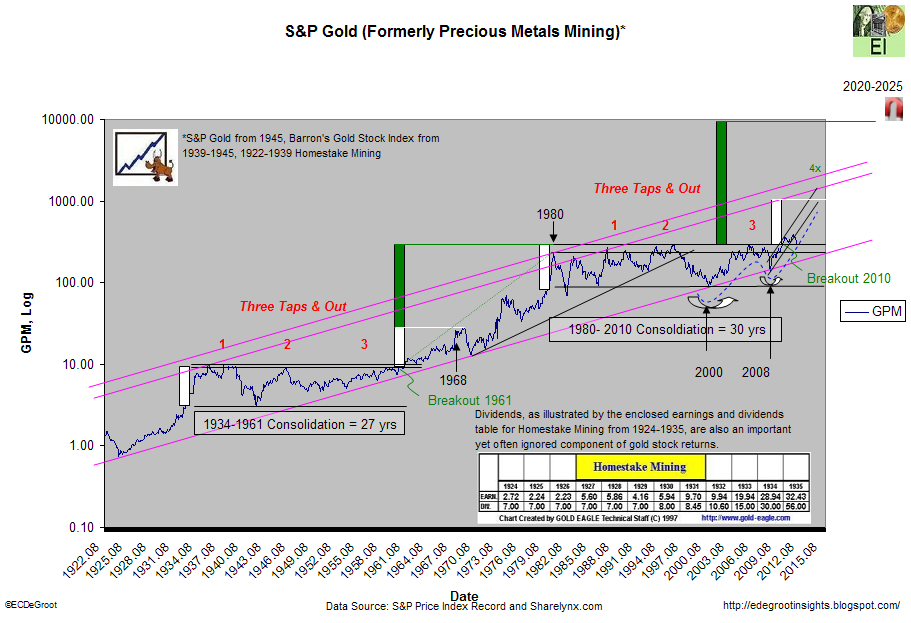

Chart: S&P Gold (Formerly Precious Metals Mining)* to Gold Ratio: * S&P Gold from 1945, Barron's Gold Stock Index from 1939-1945, 1922-1939 Homestake Mining

Testing previous resistance as support after the breakout is nothing more than ebb and flow within a market. Those trading short-term technical patterns better be expert traders, because nothing has reversed the long-term breakout and secular up trend.

Double tops, heads and shoulders formations, etc, offer only limited reentry guidance. This game is all about control and control resides in the paper market. When the invisible hand regains control of the paper market, the mining shares will be released again regardless of the technical formations in play.

Chart: S&P Gold (Formerly Precious Metals Mining)*

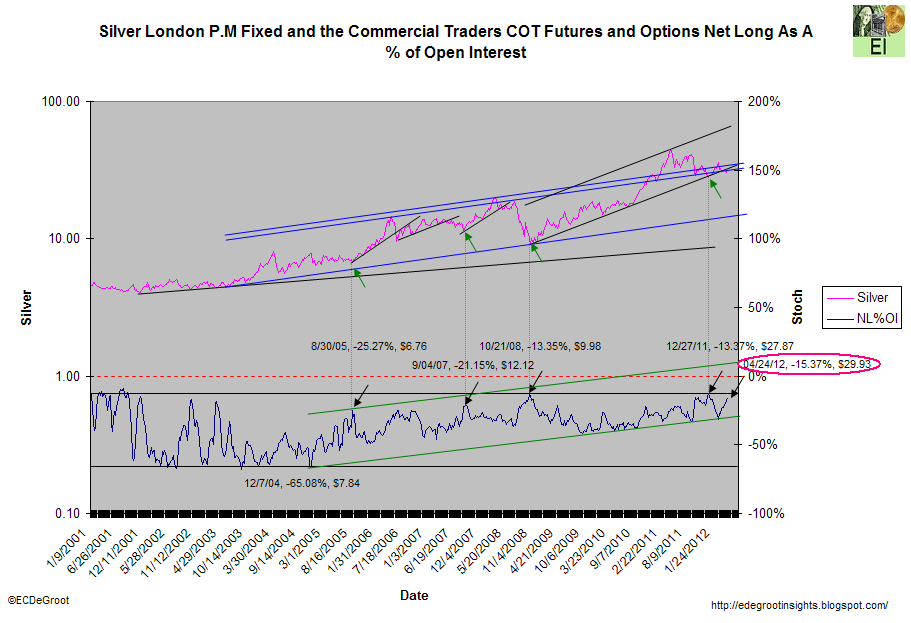

A short-term peak in the composite lease spread on 4/3 suggested that the invisible hand had started leaning on silver again. The price of silver was $31.98. As of 4/24 composite lease spreads and price of silver continue to decline. As I wrote Monday, "

Negative lease spreads tend to reverse into weakness unless the trend becomes uncontrollable."

The invisible hand remains in complete control of the silver trend. I anticipate that controlling interests will continue to reduce their leveraged short positions into this weakness and net long as percentage of open interest will surpass the all-time high of -13.35% set on October 21st, 2008 by June 2012.

Chart: Silver London P.M Fixed and the Commercial Traders COT Futures and Options Net Long As A % of Open Interest

http://edegrootinsights.blogspot.fr/2012/05/gold-shares-under-performance-to-gold.html

http://edegrootinsights.blogspot.fr/2012/05/dont-get-caught-chasing-your-tail.html

http://edegrootinsights.blogspot.fr/2012/05/invisible-hand-abusing-silver-investors.html