Re: Cisco Looks to Acquire Acacia Communications

in response to

by

posted on

Jul 15, 2019 01:48PM

Wake, a little more on this from a SA contributor

Cisco reports a five-pronged strategy for its acquisitions in its attempt in capitalizing on the latest innovations in an efficient manner.

The company's acquisition strategy in relation to its overall free cash flow picture has been conservative and seems to be continuing that way.

Both of the two largest acquisitions that Cisco has made in 2018 and 2019, Broadsoft and Acacia, seem to have the most synergy potential.

As reported by Seeking Alpha News on July 9, 2019, Cisco (CSCO) announced plans to acquire one of its suppliers Acacia in a $2.6 billion transaction. Cisco has a long tradition of making acquisitions as part of its growth strategy, and it has the cash flows to do it consistently. The company has had a very good problem as of late, plenty of cash and seemingly not enough places to put it. The company turned heads last year with its announcement of $25B in share buybacks and has spent a considerable amount of money on acquisitions along the way.

In fact, 2017 marked the year that Cisco made its 200th acquisition, and last fiscal year (2018), the company completed eight acquisitions. In this article, I will examine those purchases and how they relate to this recent Acacia one to see if we can speculate on the effectiveness of this particular use of free cash flow.

From the 2018 annual report, the company looks to exploit the most recent innovations in its growth strategy by relying on what it calls a five-pronged approach. This strategy includes various components of running its very profitable business, summarized as "Build, Buy, Partner, Invest, and Co-Develop".

As you can see, each of these five components can directly or indirectly lead to revenue or contributions to the bottom line, so it may not be fair to evaluate each acquisition based on a purely numbers-based focus. An acquisition in a profitless business may not be a failure even if the business remains profitless if it indirectly contributes to Cisco's success in other ways. This makes it difficult to evaluate each of its past acquisitions in a totally concrete way. However, the numbers still help us paint an accurate story and can be compared to the financials of the entire company in order to better understand if money is being allocated wisely.

There are no perfect ways to do this, and the idea of evaluating acquisitions is a fine art in and of itself. What I can tell you from my experience in buying stocks where poor allocations have been made is that the biggest sign of a huge waste of investor capital is in a goodwill impairment (as I discussed on the podcast I co-host with fellow Seeking Alpha contributor David Ahern). This can't really be foreseen ahead of time with any sort of certainty, but we can use the knowledge of goodwill impairment to identify cases where the chances of a large goodwill impairment are minimized. That's what this article will focus on as the primary evaluation of Cisco's eight acquisitions from 2018.

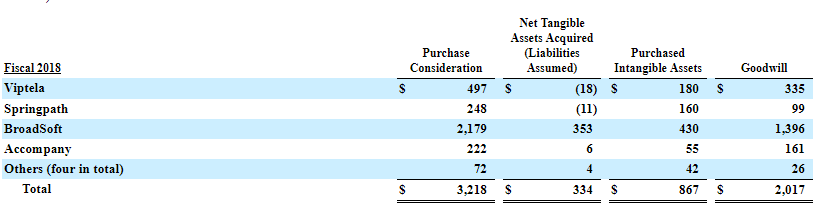

Let's look at the financials behind these acquisitions. A complete table with this data from the Cisco 10-K is displayed below. Four of the acquisitions only contributed about $72 million of the $2.8 billion allocated, so these will be ignored. Of the remainder, the Broadsoft acquisition cost about $2.2 billion and as such should make up the primary focus. Viptela cost $497 million with Springpath contributing $248 million and Accompany contributing $222 million. Note that of the total cost of $3.218 billion, Cisco reported spending $3 billion of net cash for the year.

Source: CSCO 10-K

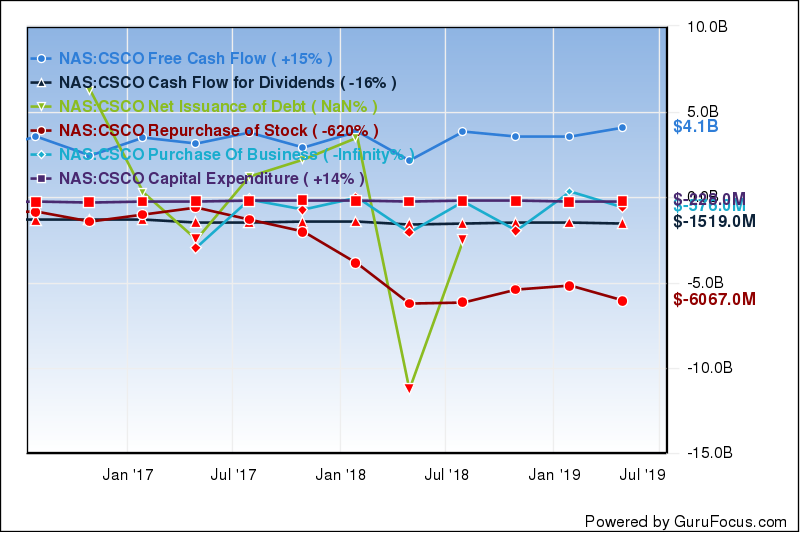

Which brings us to the free cash flow picture of the equation, a crucial part of evaluating the effectiveness of Cisco's use of cash. As quoted in the 10-K: "We further regard free cash flow as a useful measure because it reflects cash that can be used to, among other things, invest in our business, make strategic acquisitions, repurchase common stock, and pay dividends on our common stock, after deducting capital investments".

As we can see nicely from the chart, free cash flow has been steady even with the company's large repurchases (keep in mind that the figures above are quarterly figures and add up to the total sum reported online). Dividends paid keep a pretty straight line as expected. Capital expenditures are up +14% over the reported period (indicating healthy reinvestment into the business outside of acquisitions), and you can also see the large debt payoff in green in between the Jan 18 and July 18 section (over $10B). The purchases of businesses (acquisitions) are marked in the light blue line, and the overall picture doesn't seem to have been a terribly aggressive way for Cisco to invest its free cash flows.

With that in mind, I think the first conclusion can be that Cisco can afford to make these acquisitions, and if I'm blunt, can afford to overpay for some of them. An acquisition that may seem like a waste in the short term can be a great play in the long term, and Cisco can afford to be patient in major buys like that. Having that context is an important part of evaluating the company's five-pronged acquisition strategy, and how it's made decisions during the 2018 fiscal year.

Now let's examine the biggest spend of 2018, Broadsoft. At the time of purchase, the company was a global leader in UCaaS (United Communications as a Service) and CCaaS (Contact Center as a Service). With Cisco envisioning a move away from hardware and more to software and SaaS with its market-leading WebEx collaboration software, this synergy seems so incredibly natural. Broadsoft's over 19 million business subscribers don't help either and can make for a valuable asset on top of its other tangibles.

Speaking of the tangibles, let's revisit the financial data from this acquisition. Net tangible assets from the purchase total $353 million, leaving the remaining 83.8% to make up the intangible assets and goodwill. With such a large percentage of the purchase making up goodwill, this is where the biggest problem can be (spoiler alert). Over 50% of this purchase is going to goodwill, which means that Cisco could be overpaying by this amount. Only time will tell, but a substantial goodwill impairment in this business segment could indicate a waste in investor capital that could've been better spent perhaps with further share buybacks.

But where does it fit in the Cisco five-prong strategy? Well, this seems to squarely hit the nail on the head of the Partner component. There's the potential for the experience of Cisco in online meetings and collaborations with these UCaaS and CCaaS revenue drivers, as well as a way for Cisco to further dip its toes into the small- and medium-sized businesses' customer base. With the weighted average useful life of the intangible assets that Broadsoft brings right at a figure of four years, it seems that investors should find out in the next several years whether those synergies bear fruit or not.

Two of these acquisitions also come with a steep price in relation to total assets compared to Goodwill (Viptela (67.4%), and Accompany (72.5%)). Springpath seems like the safest option with Goodwill only comprising of 40% of the overall purchase price, but as with any business, the risk is still there of a failing model in one way or the other.

Viptela also looks like a nice fit with its recurring revenue model and bolsters Cisco's position in the SD-WAN (software defined wide area network) industry. With the company's push to cloud-based technology solutions, the company should have nice synergy with its acquirer, at least as it sounds from a qualitative perspective. The numbers indicate that there's a risk that Cisco overpaid, in my view, more so with this rather than with Broadsoft. From what I gather from the preliminary news surrounding both acquisitions, it seems like there's more of a possibility for revenue to be created from synergies with Broadsoft, but we should have more clarity in the next couple years as more income data gets reported.

Finally, the purchase of Accompany is an attempt of Cisco to springboard off of companies that have established themselves in high technology spaces such as the AI field that Accompany resides in. This one is also slated to enhance the WebEx suite, and the reports indicate that the valuable IP seems to come more in the databases that the company has built rather than in more direct types of measurable financial data like clients, subscriptions or total revenues. I'd say this falls into the Partner category of the five-pronged strategy as well in contrast to Viptela which could be more of a direct Buy play.

The latest acquisition has the attention now. How this plays out makes for an interesting potential power play by Cisco. Acacia was a major supplier to Cisco and also supplied other competitors such as ZTE, Infinera Corp, and ADVA Optical Networking. This can give Cisco a lot of options in the way that it chooses to utilize this asset. On top of that, most of Acacia's $339.9 million of revenue would contribute to Cisco's top line immediately were that business model to remain constant.

With Cisco's large free cash flows, the company has had money to play with and continues to flex its buying power. So far, the history of the company's acquisitions has played out well, with no signs of major goodwill impairment markdowns. Cisco has a specific five-pronged strategy for the implementation of its acquisitions, and some of the ones discussed above won't directly contribute to the company's financials, at least in the short term. By keeping an eye out on these developments and comparing them to the company's overall capital allocation strategy, investors can feel confident in the future of the company and continue to hold for expected future share price growth. I know that's what this investor is doing.