Re: VERY good article......quester... up 70% soon

in response to

by

posted on

Dec 04, 2013 09:15AM

(Edit this message through the "fast facts" section)

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More...)

Questerre Energy Corporation (OTCPK:QTEYF), an independent energy company, which engages in exploration and production of non-conventional oil & gas resources, has witnessed a 69% upside in 2013. The rally is not speculative and is backed by strong fundamental factors. This research discusses the factors for the upside in 2013 and the reasons for concluding that the stock can rally another 70% with a one-year time horizon.

More on Questerre Energy's Assets

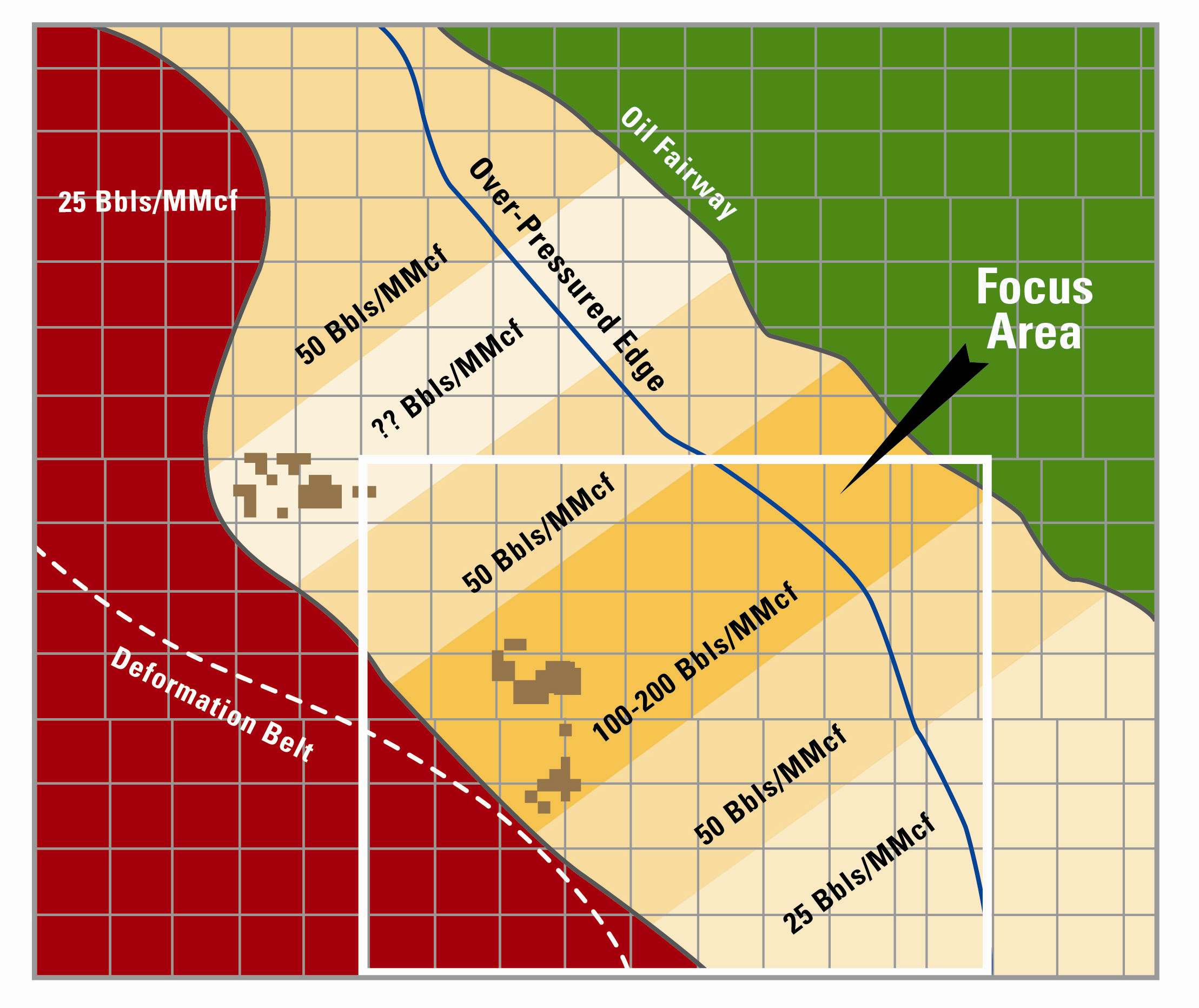

The assets of Questerre Energy are primarily non-conventional oil & gas resources. One of the primary assets of the company is located in the Kakwa-Resthaven area. The area is prospective for liquids-rich natural gas in the deep, over-pressured fairway of the Montney shale at a depth of approximately 3,100m to 3,600m. The company holds an average 76% working interest in 37,600 acres in this area. What is important to mention here (and will be discussed later in details) is that the company's activity has targeted a sweet spot where the natural gas liquids range as high as 195bbls/MMcf.

(click to enlarge)

Through its equity investment in Red Leaf Resources (a private Utah-based oil shale and technology company), Questerre has acquired an interest in two oil shale projects in Utah and Wyoming. The 6% equity capital of Red Leaf has been acquired for a consideration of $41 million and it gives Questerre Energy licensing rights to the EcoShale In-Capsule process and a 20% working interest in oil shale acreage in Wyoming.

Questerre Energy and its partner Talisman Energy (TLM) also have interest in the St. Lawrence Lowlands between Montréal and Québec City. According to the company's presentation, the acreage has 18 Tcf prospective recoverable resources (4.4 Tcf net to Questerre Energy). The area is currently undergoing a strategic environmental assessment and I will not consider the asset in my valuation at this point of time. The reason being that monetisation of the asset will take time and it might be too early for the stock to discount the growth from the asset.

Questerre Energy also has 100% interest in approximately 39,000 high-graded acres at Pasquia Hills. The company drilled 16 wells in the interest in 2012 with good quality shale encountered in all the wells drilled. The company's production from Saskatchewan was 413 boepd as of 3Q13.

Valuing The Montney acreage - Taking cues from the recent Talisman deal

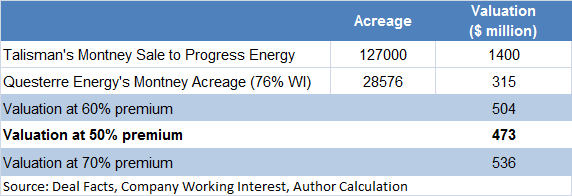

As mentioned earlier, the Montney acreage (76% working interest in 37,600 acres) is one of the primary assets of the company. Valuing the asset can give an important direction towards valuing Questerre Energy. My job is relatively simplified by a recent deal by Talisman Energy to sell Montney assets to Progress Energy Canada for $1.4 billion. The sale involves a total acreage of 127,000 with the company still retaining 48,000 acres of prospective Montney land.

Before I use this deal as an indicator to value Questerre Energy's assets, I must point out here that the valuation of the asset depends largely on the average liquid content in the acreage. Higher the liquid content, the better would be the valuations. According to Talisman Energy's third quarter news release:

In the Montney, Talisman initiated a 27-well completion program in Farrell Creek. The company is operating two drilling rigs targeting the liquids-rich area of the play. Recent completions have shown a 40 bbls/mmcf condensate-to-gas ratio on test.

In sharp contrast to this, Questerre Energy's acreage is in a sweet spot and exploration results over the past one year have shown that the liquid content in the acreage ranges between 100 bbls/mmcf to 200 bbls/mmcf.

Going back the timeline, which will also explain the company's 104% rise in share price in 2013, the first Montney well had an average condensate to natural gas rate of 100 bbls per mmcf. The second well, which wastested in January 2013, had an average condensate to natural gas ratio of 200 bbls per mmcf. Most recently, the company fifth liquid rich Montney well tested at 1,400 boepd and had an average condensate to natural gas rate of 195 bbls/mmcf.

These results point to a conclusion that Questerre Energy's Montney asset will command a significant premium compared to Talisman Energy's assets based on the condensate to natural gas rate. Below is the valuation of Questerre Energy's acreage considering the Talisman deal as a ball-park valuation estimate and assigning a premium for a higher liquid condensate.

(click to enlarge)

Based on the stake sale by Talisman Energy, Questerre Energy's 28,576 acres of working interest area should be valued at approximately $315 million. The significant point here is the premium that needs to be assigned to the company's assets, which have a significantly higher condensate to natural gas ratio. The best idea is to consider a scenario analysis with different premiums assigned over the base valuation. I must also mention here that I have taken conservative premiums to stress test the valuation in case of lower oil prices. Even if I consider that the average condensate to natural gas ratio is 80 bbls per mmcf over the acreage and oil prices witness a 10-15% decline from current levels, I can still assign a 50% premium to the acreage over the Talisman deal. The valuations can be significantly higher and I would therefore look at a 60% premium and a 70% premium as well. The base case scenario would however be a 50% premium over the Talisman deal.

Based on the base deal and the premium assigned, Questerre Energy's Montney acreage has a rough valuation of $470 million.

The Red Lead Resources Stake Valuation

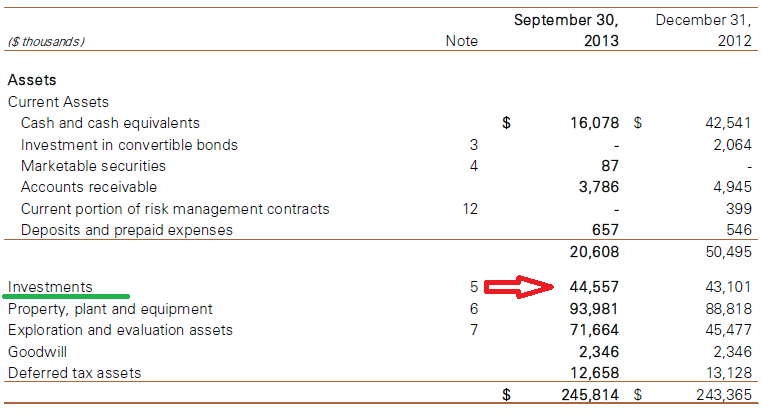

As mentioned earlier, Questerre Energy had bought a nearly 6% stake in Red leaf Resources for a consideration of $41 million. The stake is shown in the company's balance sheet as investments and has a current value of $44 million. To be as conservative as possible, the stake can just be valued at the same assuming that Questerre Energy puts up the stake for sale.

(click to enlarge)

A deeper look into the stake and the participating players does lead to a conclusion that the valuation of the 6% stake in Red Leaf Resources will increase going forward. The confidence comes from the presence of oil major, Total S.A. (TOT) in the joint venture. I must remind readers that Total had acquired its stake in the Utica Shale from Chesapeake Energy (CHK) in 2012 for $2.3 billion. The company has been active in shale resources, which potentially contain more than ten times the resources of oil sands.

Coming to the current joint venture, the press release related to the JV states:

Red Leaf and Total intend to launch an advanced commercial scale project on approximately 11,000 acres of jointly owned oil shale leaseholds that are estimated to contain several hundred million barrels of recoverable hydrocarbons. Total will also fund an 80 percent share of the first $200 million of the commercial production phase of operations. As part of this agreement, Total has the right to license the EcoShale™ technology for use on other future oil shale projects worldwide and has become a shareholder in Red Leaf Resources, Inc.

The most important point here relates to the funding for development of the resource. With Total making a major contribution, the development will not face funding issues and should start creating value for stake holders in 2014 and beyond when the first commercial scale production is expected to be initiated. For now, I will assume that the stake has a value of $45 million.

I have not initiated any discussion for St. Lawrence Lowlands as the asset will take time for monetization and the value of the assets might not be discounted immediately in the stock. However, the Montney asset should provide a revenue bump-up in 2015 and 2016. For the same reason, I have considered a one-year time horizon for the valuation gap to be filled. On considering the current market capitalization and the valuation of two prime assets, the case for a 70% upside is established.

I must mention that the company has no debt on its books. I have considered the $26.5 million undrawn facility as used for my valuation assumption.

Risk Factors

Risk One - One of the primary concerns related to non-conventional energy resources is the impact on the environment. Change in regulations on this front can result in cost escalation or delay in projects and potentially impact the growth.

Risk Two - The Montney acreage will require more funding in the future for development. While Questerre has sufficient financial bandwidth, any dilution of equity can impact valuations on the downside.

Risk Three - The company's projects have a relatively high breakeven price. If oil prices ease due to a decline in tensions in the Middle East, growth can be impacted. I have however incorporated lower oil prices in my assumption and valuation of Montney assets.

Conclusion

Questerre Energy still has a lot of potential in terms of stock price upside as well as in terms of growth related to the company's assets. The 69% upside in 2013 is just the beginning of a long-term uptrend in the stock. In the immediate future, the stock has another 70% upside based on its asset valuation. This is a conservative view and hence the stock is a strong buy at these levels. As the Montney asset development continues, the stock will completely price in the potential. The investment in Red Leaf Resources can potentially trigger another wave of upside and the developments in that asset need to be monitored before a re-rating.