analysis

posted on

Nov 28, 2012 11:34AM

Edit this title from the Fast Facts Section

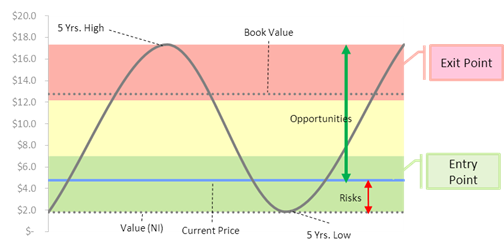

Chart 1 : 5 Years Analysis

Chart 2 : 52 Weeks Analysis

If we look at the 52 week’s pricing trend, low is $4.17 and high is $6.69.The current price is towards the lower side based on 52 week’s price range. If we look at the 5 years pricing trend, the low is $1.85 and the high is $17.35, the current price is again towards the lower side based on 5 years price trend. This indicates that it is a good entry point. (See chart 1 and 2)

Table 1: High / Low Prices

The Ambatovy Project is the largest nickel and cobalt project located in Madagascar. The project is planned to be mined for 29 years. The Ambatovy Project is expected to be one of the worlds biggest in lateritic nickel mining, processing and refining operations.

Sherritt is the operator of this project (with 40% interest) with the following as its partners. Sumitomo Corporation (with 27.5% interest), Korea esources Corporation (with 27.5% interest) and SNC Lavalin Inc. (with 5% interest) (collectively referred to as the Ambatovy Partners). The deposits from the ore will be delivered through pipeline to a processing plant and refinery. The Ambatovy Project has reserves of 169.9 million tons of grading 0.95% nickel and 0.08% cobalt. Forecast for Annual production capacity is at 60,000 tons (100% basis) of nickel and 5,600 tons (100% basis) of cobalt.

Project estimated cost is $5.5 billion (Sherritt share 40% * $5.5B = $2.2B). Out of the total $5.5billions, $5.3 is already spent.

The Ambatovy Project is facing political risks and is under Scrutiny from the government of Madagascar. The government of Madagascar has announced the audit of economic and environment impact of the mining sector. The project has received six-month Operating Permit to commercially operate the processing plant in Toamasina and Madagascar which will be converted automatically to life of mine Operating Permit at the end of the six month.

Table 2: Impact of Ambatovy Project

Sherritt’s maximum expected loss from the project is $7.4 per share ($2.2B ÷ 296.9M shares). Its book value is $12.59 per share. So, if we remove Ambatovy Investment from its book value, still the remaining book value is $5.19 ($12.59 – $7.40). Its market price is $4.77 which is lower than its book value without Ambatovy. Risk associated with Ambatovy Project is already reflected in the price.

Further, Sherritt’s earning is low due to lower nickel spot price and volume and lower export thermal coal volumes, which are transient in my opinion.

Average daily volume is 1.1M shares, which is equivalent to $5.2M based on the current price. This means that the deals that are equivalent to average $5.2M, complete in one day. The maximum level of $52k is suggested for the investment to keep the liquidity high.

N/A

Table 3: Valuation of stock

Sherritt’s liquidation value and book value is $12.78. Its Net Present Value (Based on Net Income) is 2.31 and Net Present Value (Based on Free Cash Flow) is $1.83.

Risk vs. Opportunity ratio may be defined as the comparison between the strength of the opportunity and the risk involved in the investment. For Sherritt, the opportunity is 3x of the risk based on 52 week’s analysis and 4x based on 5 year’s analysis. (See chart 1 & 2)

Price Earnings Ratio for Sherritt is lower than the Mining & Metals – Specialty industry. This shows that there is a potential to grow in Sherritt to align with industry.

Dividend yield is yet another factor which an investor needs to know before investing. Generally, a dividend paying company is considered to be a mature company in their business as it does not have any investment opportunities to grow and earn more than their capital cost. These companies are consistently making profit. Since these companies make consistent profit and they do not have any opportunity to invest further, they distribute dividend to their shareholders. Big returns cannot be expected by investing in these companies, but we are at the least risk in investing in the same.

Sherritt (S) is a having a dividend yield of 3.4%.

Based on the above analysis, it is worth investing in Sherritt International Corporation (S). The value of the investment is less risky than the opportunity available.

http://www.miningwatch.ca/article/another-mining-horror-story-sherritt-international-corporation-s-ambatovy-project-madagascar

http://www.sherritt.com/Operations/Metals/Ambatovy-Joint-Venture

http://tripwow.tripadvisor.com/tripwow/ta-00d6-7bfa-bee9

http://www.youtube.com%2Fwatch%3Fv%3DGrQxCtAMt7E&ei=hVygUJ7OF8XTyAHSl4GYAw&usg=AFQjCNGD_xbuRO5bHZiniGwmGU406wcw2A&sig2=UtnEW4uNzO8bfIAVs621aw

Enter your email address to receive new post by email.

Join 87 other followers