Actual GLD Vault

There seems to be a misunderstanding in the gold market that when you buy or sell shares of GLD you are putting pressure on the price of gold. That selling shares of GLD into the exchange is somehow analogous to selling physical into the marketplace. Or that buying shares of GLD is somehow, somewhere down the chain, removing physical gold from the marketplace.

We often look at apparent correlation and assume a certain cause and effect. GLD is

designed to track the price of gold. It is not actively managed to track the price of gold. Instead, it does so through opportunities that arise whenever it doesn't. Imagine GLD as a big lump of gold just sitting there in Town Square. The price of gold is "discovered" elsewhere and shares in this big lump just trade based on that elsewhere-discovered price. If the share price is too high, then an opportunity exists to sell your share and buy "gold" elsewhere. Likewise, if it is too low, there is an opportunity to sell elsewhere and buy into this lump on display.

Occasionally, lately, someone comes along and shaves a chunk off of the lump, reducing its overall size. And financial reporters and analysts everywhere are struggling to correlate the price of gold and the GLD holdings with some semblance of cause and effect:

The Street – Alix Steel

Gold prices were breaking even after another double-digit selloff Tuesday as investors dumped their holdings. The SPDR Gold Shares exchange-traded fund dropped more than 30 tons of gold on Tuesday.

Reuters

Traders in Asia reported strong physical gold buying, particularly from China, on Friday, but large bullion-backed exchange-traded funds continued to see outflows.

Reuters - Amanda Cooper and Jan Harvey

But investor sentiment towards gold has soured in the last few sessions, as evidenced by the largest one-day outflow in three months from the world’s biggest exchange-traded gold fund. Holdings in the SPDR Gold Trust fell 10.926 tonnes to 1,260.843 tonnes on Jan 24.

Funny. When we're talking about gold, an outflow to one person is an inflow to another, is it not? Randy Strauss at USAGold.com rightly responded to these silly reports with the truth [emphasis mine]:

RS View: Silly reporters. Instead of calling these “outflows” from the ETFs, it should be called what it is — a redemption of a basket of shares for physical gold by the Authorized Participants (e.g. bullion banks). Such share redemptions would actually be a bullish sign because it entails a reduction in the global supply of paper gold while at the same time signifying a preference by the redeeming party for having the metal over the ETF shares. That is, of course, unless the drawdown in physical gold merely represented the routine sales of the gold inventory that occur to cover the ETF’s administrative expenses.

RS View: I’ve said it before and I’ll say it again now, the reporters are getting it wrong when they equate outflows of gold from the ETFs with “sour” investor sentiment. What they need to work harder to understand is that these are NOT actively managed funds whose gold inventory is tweaked to ebb and flow based on public sentiment in the shares. Instead, the ETFs are more like a central coat-check room in which the various bullion banks have temporarily hung out their own inventories (i.e., meaning, their unallocated stock which they hold loosely on behalf of their depositors). And whereas the claim tickets (ETF shares) may freely circulate on the open market, any significant outflow of physical inventory is simply and primarily indicative of a bullion bank reclaiming the original inventory based on a heightened need or desire for physical metal in a tightening market — for example, to meet the demands emerging from Asia.Here's another one. I found this to be an interesting post, even though the blogger is toeing the same line as the reporters above [emphasis mine]:

Gold Bubble?

Usually in a bubble, investors are holding a bag.

Usually in a bubble, investors are holding a bag.

Investors have been net sellers of about 100 tonnes in the last 7 months. The IMF has disposed of another few hundred tonnes. Yet gold price is higher by around 10% in the same period.

To put this into context, since December 21st alone, 2.2M ounces have been sold from the ETF, basically a bit more than an entire quarter of production from Barrick gold (the world's largest producer). The normal run rate of global recycling plus mine production is approximately 2.95M ounces per month. So in the same period, assuming GLD was the only source of outflow, total global absorbed gold supply was 5.15M ounces. If outflows continued at the current rate, the GLD ETF (the largest investor depository of gold by far) would have no gold in 18 months.

Supply increased 75% in the short term to see price only fall 4.5%.

Someone else is doing the buying, clearly.

2.2M ounces is more than

68 tonnes... since December 21! Who is taking this stuff?

Now here's a bloodhound that might be on to a scent worth following. Lance Lewis, in his

subscriber newsletter, follows what he calls

"the GLD puke indicator" which tracks GLD physical gold regurgitations [emphasis mine]:

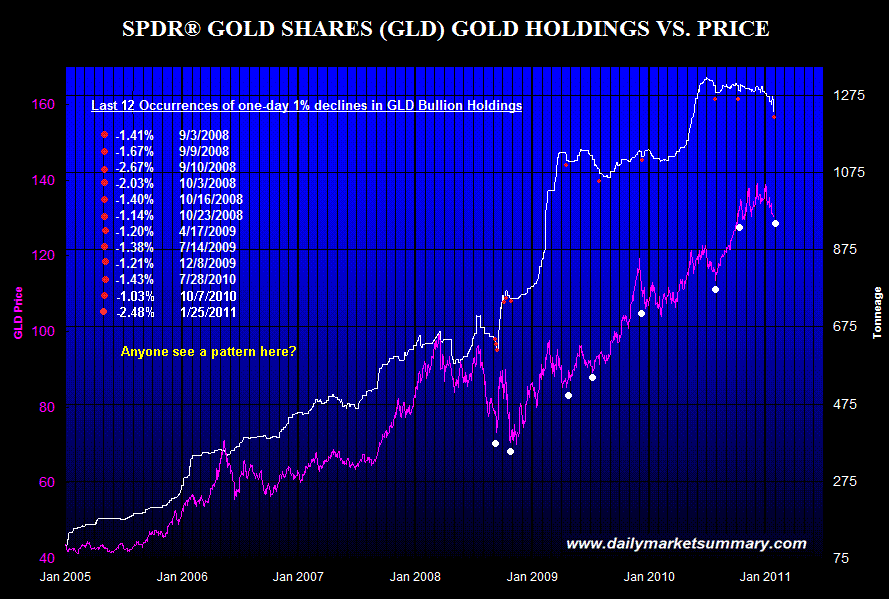

Just in case anyone missed it in last night’s letter, our GLD puke indicator that has nearly a flawless record at marking lows in gold triggered a buy signal yesterday after the ETF spit up 31 tonnes (and some blood) to trigger a 2.48% decline in its bullion holdings.

As we’ve noted before, one-day declines in the holdings of this ETF of over 1% have tended to be capitulatory in nature and have typically occurred near important lows in the gold price during gold’s secular bull market.

As we’ve noted before, one-day declines in the holdings of this ETF of over 1% have tended to be capitulatory in nature and have typically occurred near important lows in the gold price during gold’s secular bull market.

Consider that since the GLD ETF’s creation back in 2004, it has seen 1%+ one-day declines in its bullion holdings only 41 other times. When one goes back and looks at where these declines in bullion holdings have occurred, virtually all of them occurred “at” or were “clustered at” important lows in the gold price.

When we update this familiar (see above) chart for today’s 1%+ decline in bullion holdings, we can once again see where I have labeled the past eleven 1%+ declines in the ETF’s bullion holdings (plus today’s decline) with red dots and then placed a corresponding white dot below the price of GLD in order to show where that decline (or clusters of declines, as was the case in 2008) occurred relative to the price of the GLD, which is obviously tied to spot gold.

You will recall that we most recently used this indicator back on July 28th, 2010 in order to identify what was then the summer low in the gold price, and we used it again on October 7th, 2010 to recognize that a sudden 1 percent slide in gold from an all-time high was actually a just a one-day setback that led to new all-time highs being hit once again just a few days later.

The pattern you see emerge after today’s 1%+ puke, just as on those prior occasions, is that these “pukes” of bullion by the GLD ETF have always tended to occur at or very close to important lows in the gold price, and declines of over 2% have only occurred at MAJOR lows, such as the two major lows that were hit in 2008.

Note that one of those lows on September 9, 2008, which is the closest in size to today’s puke, also occurred just one day before a 5-day short squeeze/meltup of 30 percent in the gold price that kicked off on September 12, 2008. Perhaps the remaining shorts in the gold market will now pay a similar price for betting against a bull market?

Perhaps history will repeat and perhaps it won’t with respect to such a short squeeze, but given this indicator’s near flawless record at marking lows in gold, it's not to be ignored.What we appear to have here is a severely tight noose around the supply of Bullion Bank deliverable physical gold at a time when the Giants are chomping it up! Bullion Banks have many means at their disposal to shuffle around a globally limited quantity of gold reserves and get it to where it needs to go. Especially when "important clients," like those in the East or Middle East, come calling for physical delivery or allocation.

Upon getting requests from unallocated depositors for either outright withdrawal, or more simply for transfer into allocated accounts, any Bullion Bank has options. Yes, it can seek to acquire (through borrowing or purchase) the requisite ETF shares for redemption of a "basket" in its special capacity as an Authorized Participant of GLD, or it can pursue alternate avenues such as buying gold on the open market or, better still, borrowing it from either its own unallocated pool of deposits or turning to other members in the BB fraternity to borrow the adequate quantity to cover the immediate needs. Whatever combo is deemed most efficient or cost-effective is what the bank will do.

But what if those other options are disappearing faster than a sack of currency left on the COMEX trading floor? If gold (in size) on the open market is scarce, the unallocated pool is spoken for (in other words, undergoing allocation) and the fraternity brothers are all suffering the same noose, what do you think becomes the most efficient and cost-effective option? Raiding the GLD reservoir perhaps?

Did you even know that you could take physical delivery from GLD? Apparently many didn't. I was just chatting (online) with one of my supporters yesterday, let's call him "Small Giant" (a term explained in my

last post) because he

is in that eight figure savings bracket that might find this information useful. On top of that, he makes his living assisting funds in their management of eleven figures.

So he says to me:

Small Giant [6:10 P.M.]: I think very very few people realize that you can convert GLD shares to actual physical

Small Giant [6:10 P.M.]: can't say I know of anyone who has ever done that

Okay, let me back up.

Small Giant [5:47 P.M.]: there is clearly panic in the ranks of the longs

FOFOA [5:47 P.M.]: The more it goes down, the bigger the pressure on physical. I think the draw down in GLD suggests other options for physical delivery in size are gone.

Small Giant [5:47 P.M.]: I agree

FOFOA [5:49 P.M.]: With $13 million, you could take possession of a basket of physical from GLD at a good price.

Small Giant [5:49 P.M.]: what is the minimum threshold?

FOFOA [5:50 P.M.]: 100,000 shares is a basket. Must be redeemed through an "Authorized Participant"...

Small Giant [5:50 P.M.]: wow this is getting very very interesting

FOFOA [5:50 P.M.]: Authorized Participants are: BMO Capital Markets Corp., CIBC World Markets Corp., Citigroup Global Markets Inc., Credit Suisse Securities (USA) LLC, Deutsche Bank Securities Inc., EWT, LLC, Goldman, Sachs & Co., Goldman Sachs Execution & Clearing, L.P., HSBC Securities (USA) Inc., J.P. Morgan Securities Inc., Merrill Lynch Professional Clearing Corp., Morgan Stanley & Co. Incorporated, Newedge USA LLC, RBC Capital Markets Corporation, Scotia Capital (USA) Inc., and UBS Securities LLC

Small Giant [5:51 P.M.]: so how would that work?

Small Giant [5:51 P.M.]: you buy 100K shares of GLD

Small Giant [5:51 P.M.]: then what?

FOFOA [5:53 P.M.]: You've got to go to one of those APs and have them create a basket for you. That gold is then transferred from the GLD allocated account into your broker's unallocated account. Then you redeem your basket and have your broker allocate the gold to you.

Small Giant [5:54 P.M.]: so it's really is that easy?

FOFOA [5:55 P.M.]: I'm working on a post tentatively called "Who is Draining GLD" using a lot of snips from the prospectus. The entire world of confused financial analysts is misinterpreting the GLD inventory reduction as if it is gold negative. But it is precisely the opposite. GLD doesn't buy gold when it's going up and sell when it's going down. Doesn't work that way. But that's what everyone thinks.

FOFOA [5:57 P.M.]: GLD might be the last reservoir for the giants to drink from. That's my Thought of the day. Because there should be easier ways to buy a tonne of gold.

Small Giant [5:58 P.M.]: u lost me

Small Giant [5:59 P.M.]: count me as a confused financial analyst

So after this chat I started thinking that I should write this post for other "small giants" out there that might be looking for tonnes of physical at a good, off-market price.

Does anyone remember the Jim Rickards comment I quoted in

Open Letter to EMU Heads of State? Here it is:

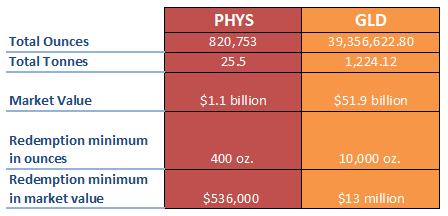

"One point that does not get enough attention is the impact of size in the physical market. It’s one thing to say that COMEX is $1,100 per ounce and physical might be $1,200 per ounce for one metric tonne if you can find it. But what about 100 tonnes? 500 tonnes? Physical orders of that size are impossible to execute outside of official channels. Size of order is relevant in any market but I have never seen a market (short of a full blown manipulation or short squeeze) with as much price inelasticity as physical gold which is why the buy side overhang keep their intentions to themselves."Now you are probably thinking, "why bother with GLD where a minimum "basket" is a whopping 100,000 shares (around 10,000 ounces) for $13 million dollars when you can take delivery of as little as a 400 ounce "LGD bar" from Eric Sprott's PHYS for just over a half million dollars?" If you thought that, then you are not thinking like a Giant. Read Jim Rickards' comment again. Giants like to keep their intentions to themselves. Why? Because they prefer to buy in off-market transactions – ones that do not influence the price of gold – in order to maximize the number of ounces they receive for their normally market-moving quantities of currency. They know that the size they want to convert would move the price, and then they would get less gold for their money.

Now let's compare PHYS with GLD and try to think like a real Giant for a minute.

The one day drain from GLD just the other day was larger than the entire PHYS ETF by more than 5 tonnes. So what would have completely emptied the Sprott warehouse was only 2.48% of GLD. The amount drained from GLD since Dec. 21st was 268% of Eric Sprott's PHYS. And what has it caused but barely a blip on the radar? Can you imagine the fuss (or price explosion!) if one single billionaire decided to clean out PHYS? That's right. PHYS represents maybe one real Giant. That's not exactly a "reservoir" for the giant class to drink from.

If you are a Giant, or even a Small Giant, you should know about this off-market opportunity to take giant amounts of physical into your possession at a good price. And you should know this before it is all gone. As my Small Giant friend wrote, "very very few people realize that you can convert GLD shares to actual physical." He didn't know until yesterday. But it's all there in the prospectus. It tells you how to do it, and who to contact to get it done. If one of the Authorized Participants refuses your business, just call the next one on the list. There are 16 of them!

I am reposting portions of the prospectus from the SPDR Gold Shares (GLD) website right here. It may seem like a lot to read, but trust me, this is a highly abbreviated version of the 46 page prospectus. This is actually from the reader-friendly "FAQ" section of the website, although some of it comes directly from the prospectus. This is all you really need to know!

From:

http://www.spdrgoldshares.com/sites/us/faqs/8.Can you take physical possession of the gold?

The Trustee, Bank of New York, does not deal directly with the public. The trust handles creation and redemption orders for the shares with Authorized Participants, who deal in blocks of 100,000 shares. An individual investor wishing to exchange shares for physical gold would have to come to the appropriate arrangements with his or her broker.

14.How is the gold price set?

The spot price for gold is determined by market forces in the 24-hour global over-the-counter (OTC) market for gold. The OTC market accounts for most global gold trading, and prices quoted reflect the information available to the market at any given time. The spot price can be found on: www.thebulliondesk.com.

The London Bullion Market Association (LBMA) has about 70 full members, as well as many associate members. Twice daily during London trading hours the ten market making members of the LBMA fix a gold reference price for the day’s trading. These prices are based upon the actual buy and sell orders for gold in the global OTC market. A good analogy for the London fix versus OTC trading would be to consider the London fixes similar to opening/closing prices for stocks and to consider the spot price for gold as the continuous market price throughout the trading day.

The COMEX division of the New York Mercantile Exchange (NYMEX) is a futures and options exchange that acts as a marketplace to trade futures and options contracts on metals, including gold. Gold futures contracts typically trade at a premium to the spot price. Further discussion can be found in the prospectus.

15.What is the relationship between the GLD Net Asset Value, the GLD share price and the gold spot price?

The investment objective of the Trust is for the value of the shares to reflect the price of gold bullion, less the expenses of the Trust’s operations.

The Net Asset Value (NAV) of the Trust is determined by the Trustee each day that the NYSE Arca is open for regular trading. The NAV of the Trust is calculated based on the total ounces of gold owned by the Trust valued at the Gold London PM fix of that day plus any cash held by the Trust less accrued expenses. The NAV of each GLD share is the NAV of the Trust divided by the total number of shares outstanding.

The gold spot price is determined by market forces in the 24-hour global over-the-counter market for gold and reflects the information available to the market at any given time. The Indicative Intraday Value per GLD share published on the www.spdrgoldshares.com website is based on the mid-point of the bid/offer gold spot price adjusted for the Trust’s daily accrued expenses.

The NYSE Arca is an electronic exchange which displays orders simultaneously to both buyer and seller. Once orders are submitted, all trades are executed in the manner designated by the party entering the national best bid or offer. The buy and sell offers are posted on NYSE Arca in price order from best to worst and if the prices match up, they are ordered based on the time the buy order or sell order was posted (earliest to latest). These prices reflect the supply and demand for shares which is influenced by factors including the gold spot price and its impact on the NAV.

20.How is gold transferred to or withdrawn from the Trust?

The Bank of New York Mellon, as trustee of the Trust, or the Trustee, and the Custodian have entered into agreements which establish the Trust’s unallocated account and the Trust’s allocated account. The Trust’s unallocated account is principally used to facilitate the transfer of gold between Authorized Participants and the Trust in connection with the creation and redemption of Baskets (a “Basket” equals a block of 100,000 SPDR® Gold Shares). The Trust’s Authorized Participants are the only persons that may place orders to create and redeem Baskets and, in connection with the creation of Baskets, are solely responsible for the delivery of gold to the Trust. The Trust never purchases gold in connection with the creation or redemption of Baskets or for any other reason. All gold transferred in and out of, and held by, the Trust must comply with the rules, regulations, practices and customs of the LBMA, including “The Good Delivery Rules for Gold and Silver Bars.” The specifications of a London Good Delivery Bar are discussed below. The Trust’s unallocated account is also used to facilitate the monthly sales of gold made by the Trustee to pay the Trust’s expenses.

Except when gold is transferred in and out of the Trust or when a small amount of gold remains credited to the Trust’s unallocated account at the end of a business day (which the Custodian is directed to limit to no more than 430 ounces), the gold transferred to the Trust is held in the Trust’s allocated account in bar form. When Baskets are created or redeemed, the Custodian transfers gold in and out of the Trust through the unallocated accounts it maintains for each Authorized Participant and the unallocated and allocated gold accounts it maintains for the Trust. After gold has been first credited to an Authorized Participant’s unallocated account in connection with the creation of a Basket, the Custodian transfers the credited amount from the Authorized Participant’s unallocated account to the Trust’s unallocated account. The Custodian then allocates specific bars of gold from unallocated bars which the Custodian holds, or instructs a subcustodian to allocate specific bars of gold from unallocated bars held by or for the subcustodian, so that the total of the allocated gold bars represents the amount of gold credited to the Trust’s unallocated account to the extent such amount is representable by whole bars. The amount of gold represented by the allocated gold bars is debited from the Trust’s unallocated account and the allocated gold bars are credited to and held in the Trust’s allocated account. The process of withdrawing gold from the Trust for a redemption of a Basket follows the same general procedure as for transferring gold to the Trust for a creation of a Basket, only in reverse.

The Custodian updates its records at the end of each business day (London time) to identify the specific bars of gold allocated to the Trust and provides the Trustee with regular reports detailing the gold transfers in and out of the Trust’s unallocated account and the Trust’s allocated account. The Trust’s website includes a list of the gold bars held in the Trust’s allocated account. The list identifies each bar by bar number, brand, weight, fineness and fine weight and is updated once a week.

21.Who are the Trust’s Authorized Participants and what is their function?

Authorized Participants are the only persons that may place orders to create and redeem Baskets; the Trust does not deal directly with individual investors. Authorized Participants must be (1) registered broker-dealers or other securities market participants, such as banks and other financial institutions, which are not required to register as broker-dealers to engage in securities transactions and (2) Depository Trust Company (DTC) participants. Each Authorized Participant must establish an unallocated account with the Custodian in order to be able to process the gold transfers associated with creating and redeeming Baskets. Authorized Participants can place an order to create or redeem one or more Baskets on every day the NYSE Arca is open for trading. The Trust issues new Baskets to Authorized Participants in exchange for their delivery of gold to the Trust upon a creation and transfers gold to Authorized Participants in exchange for their delivery of Baskets to the Trust upon a redemption. In creating or redeeming Baskets, Authorized Participants may act for their own accounts or as agents for broker-dealers, custodians and other securities market participants that wish to create or redeem Baskets. An order for one or more Baskets may be placed by an Authorized Participant on behalf of multiple clients. A list of the Trust’s current Authorized Participants may be found in the Annual Report or Prospectus of the Trust most recently filed with the Securities and Exchange Commission.

22.What is an unallocated account?

An unallocated account is an account with a bullion dealer, which may also be a bank, to which a fine weight amount of gold is credited. Transfers to or from an unallocated account are made by crediting or debiting the number of ounces of gold being deposited or withdrawn. As gold held in an unallocated account is not segregated from the bullion dealer’s assets, credits to an unallocated account represent only the bullion dealer’s obligation to deliver gold and do not constitute ownership of any specific bars of gold. The account holder is entitled to direct the bullion dealer to deliver an amount of physical gold equal to the amount of gold standing to the credit of the account holder. When delivering gold, the bullion dealer allocates physical gold from its general stock to the account holder with a corresponding debit being made to the amount of gold credited to the unallocated account.

The Trust’s unallocated account is only used for the transfer of gold to and from the Trust’s allocated account.

23.What is an allocated account?

An allocated account is an account with a bullion dealer, which may also be a bank, to which individually identified gold bars owned by the account holder are credited. The gold bars in an allocated account are specific to that account and are identified by a list which shows, for each gold bar, the refiner, assay or fineness, serial number and gross and fine weight. The account holder has full ownership of the gold bars.

The Trust’s allocated account is only used for holding the allocated gold bars of the Trust.

26.Is the Trust’s gold ever traded, leased or loaned?

Gold held in the Trust’s allocated account in bar form or credited to the Trust’s unallocated account is the property of the Trust and is not traded, leased or loaned under any circumstances.And from the latest 10K filed with the SEC, here is the list of the current Authorized Participants [emphasis mine]:

Authorized Participants may act for their own accounts or as agents for broker-dealers, custodians and other securities market participants that wish to create or redeem Baskets. An order for one or more Baskets may be placed by an Authorized Participant on behalf of multiple clients. As of the date of this report:

BMO Capital Markets Corp.

CIBC World Markets Corp.

Citigroup Global Markets Inc.

Credit Suisse Securities (USA) LLC

Deutsche Bank Securities Inc.

EWT, LLC

Goldman, Sachs & Co.

Goldman Sachs Execution & Clearing, L.P.

HSBC Securities (USA) Inc.

J.P. Morgan Securities Inc.

Merrill Lynch Professional Clearing Corp.

Morgan Stanley & Co. Incorporated

Newedge USA LLC

RBC Capital Markets Corporation

Scotia Capital (USA) Inc.

UBS Securities LLC

…have each signed a Participant Agreement with the Trust and may create and redeem Baskets as described above. Persons interested in purchasing Baskets should contact the Sponsor or the Trustee to obtain the contact information for the Authorized Participants. Shareholders who are not Authorized Participants will only be able to redeem their Shares through an Authorized Participant.

So now I offer up a scenario, not as a statement of fact, but as fodder for thought and discussion. In this scenario I am not assuming that the drain on GLD to date has been the direct redemption of ETF shares by Giants. I presume it is simply redemptions by Bullion Banks in order to meet the delivery demands of "important clients," real Giants, perhaps from Asia and the Middle East. And because the BBs would normally have better options than plundering GLD, I am assuming those options are either gone or far more problematic than legalized looting.

Also, following Lance Lewis' "puke indicator," one could be forgiven for suspecting that the Bullion Banks have some way to temporarily "pound" the price of gold down on the COMEX in order to buy back ETF shares during a "good price window" with the intention of redeeming those shares into deliverable gold for clients that purchased it at a higher price. Perhaps it would take, what, a month or so to churn such a profit from a Giant delivery? Reminds me of that fella Jim Rickards spoke of on King World News:

Jim Rickards - Swiss Bank Client Denied His $40 Million in GoldJim: “Correct and upon request to move the gold...the bank demurred, the bank said, ‘Well, no, not so fast’ and he said, ‘What do you mean?’ Anyway, long story short I could see that taking a day or two...This took thirty days to complete delivery. Now if the gold is sitting there it shouldn’t take thirty days. Oh, and by the way I should add that the individual had to threaten to go public, in effect say I’ll call Reuters or I’ll call King World News or I’ll call Dow Jones and let them know that you don’t have the gold, you’re not good for it.”

Eric: "And he had his lawyers get involved?"

Jim: “Correct, and through all of that eventually the individual did get his gold, but this is something that should have taken two days, three days, a week at the most, although I would say even a week is a long time. But it took thirty days, and it took lawyers, it took threats of publicity, it took a lot of pressure to do that, which my inference is that that gold was not there. The bank had to scramble, go out and find it somewhere before they could make good delivery.”

I wonder when that was. And I wonder if GLD "puked" any "baskets" around that time.

Someone is draining GLD of its gold. Someone is taking in millions of ounces and tonnes of physical gold at off-market prices while the paper bug cheerleaders call it "dumping" or "offloading" the gold. Again, one man's "outflow" is another man's pickup truck (or dump truck as the case may be) backed right up to the loading dock at the GLD depository.

As of 2008, some analysts estimated there were still 15,000 tonnes of unallocated (un-spoken-for) gold floating around the Bullion Banking system. Of course some of that is still there, along with a decreasing supply from the mines and a scrap supply that, after rising since 2006, appears to have plateaued in 2010. You can continue to go after that diminishing flow "on market" by playing the paper game like

Dan Shak. But one day soon, it will all be spoken for. And you don't want to be left holding only paper on that day. And if the BBs are raiding GLD like it seems, that 15,000 tonnes may be closer to 1,200 tonnes than you or I would be comfortable knowing about.

Jim Rickards wrote about 100 tonne and 500 tonne lots being impossible to come by "outside of official channels" meaning off-market prices. But from what I can tell, there are still twelve 100 tonne lots or two 500 tonne lots available through one of the 16 dealers listed above. The instructions are all there. This isn't like the private sector trying to buy gold from the public sector, like Sprott being

turned down by the IMF. This is the reverse! Go for it, I say. Why not?

And for those of you GLD fans that think you will simply hold onto your shares until the bitter end, I have a warning for you. These Giants don't need to over-bid your shares away from you. They can always buy them at the price of paper gold trading in London and New York. And there will come a point when you are watching the premium on physical coins jump from 5% over GLD to 50% on its way to 500% over the paper gold price. How long are you going to stubbornly hold onto your precious paper before you finally relinquish it to that last Giant's delivery "basket?" Remember, unless you've got $13 million, you've only got paper.

Sincerely,

FOFOA

January 29, 2011 2:14 AM  Jenn

Jenn said...

Sixteen men on a dead man's chest for sure.

--Jenn

January 29, 2011 2:20 AM

mortymer said...

Here is next from history lessons:

Council Directive 1998/80/EC of 12 October 1998, supplementing the common system of value added tax and amending Directive 77/388/EEC - Special scheme for investment gold. [Official Journal L 281 of 17.10.1998]

http://europa.eu/legislation_summaries/taxation/l31012_en.htm

It would be nice who proposed this directive. Any takers?

January 29, 2011 2:30 AM

mortymer said...

...note the small hint at the end:

"In certain circumstances, Member States may designate the PURCHASER rather than the SELLER as the person liable to pay the tax (reverse charge procedure) in order to prevent tax fraud and reduce the costs of the transaction.

With regard to transactions on a REGULATED gold bullion market, Member States may be authorised not to apply the special scheme and introduce simplification measures."

January 29, 2011 2:34 AM

Jenn said...

"In order to promote the use of gold as a financial instrument, this Directive introduces a tax exemption for supplies of investment gold."

@mortymer

I don't know how you manage to find these nuggets, but as always your posts are exceedingly insightful. Please keep them coming.

--Jenn

January 29, 2011 2:39 AM

mortymer said...

2004: This year’s annual assembly of the European Association for Banking History was held in Athens. It was associated with conferences on the themes of Archives and the Culture of Corporations, and the Human Factor in Banking. A year after the meeting at the National Bank of Slovakia, the Greek Alpha Bank was joint organizer of the event.

The session of the EABH in Athens changed the statutes. The new name of the EABH is the European Association for Banking and Financial History. There was also a change in the leadership of the association. The former head of the European Central Bank Willem Frederik Duisenberg became the new chairman of the Executive Committee of the EABH in place of Sir Evelyn de Rothschild, who headed the association for thirteen years.

2006 Jean-Claude Trichet, President of the European Central Bank and chairman of the EABH, awarded the French-German Culture Prize by Pro-Europa 4 September

January 29, 2011 3:48 AM

J said...

Wow..very interesting. I wonder if any frustrated giants will read this and now have a glimmer of hope.

It will be fun to watch if the giants grab their straws

January 29, 2011 3:54 AM

costata said...

FOFOA,

From Monty Python's Holy Grail: The Holy Hand Grenade Of Antioch.

"And the LORD spake, saying, "First shalt thou take out the Holy Pin, then shalt thou count to three, no more, no less. Three shall be the number thou shalt count, and the number of the counting shall be three. Four shalt thou not count, neither count thou two, excepting that thou then proceed to three. Five is right out. Once the number three, being the third number, be reached, then lobbest thou thy Holy Hand Grenade of Antioch towards thy foe, who being naughty in My sight, shall snuff it." Amen."

http://en.wikipedia.org/wiki/Holy_Hand_Grenade_of_Antioch

Great post, Cheers

January 29, 2011 4:49 AM

Bron said...

The reason one cannot correlate gold price and GLD holdings is because authorized participants (AP) don't have to create and redeem GLD shares on a daily basis in response to investor activity in GLD.

For example, if you're an AP and have a view that the market is bullish, then you expect over time to see net buying of GLD. Therefore, if on one day there is net selling of GLD, then you can:

1. Buy GLD shares

2. Immediately lease gold and sell it (or just short futures).

3. AP is now long GLD and short unallocated gold or futures. Important to note they have no exposure to gold price movements.

4. Sit on the GLD shares and when investor bullish sentiment returns

5. Sell your GLD shares

6. Buy unallocated gold and repay your lease (or close out your short future).

The above process means that the AP avoids GLD share redemption and creation costs.

Same thing happens in the face of net buying - an AP borrows gold and delivers it to GLD for shares, which they sit on an over a period of time sell into demand for GLD.

This is a way of minimising transaction costs when making a market in GLD or SLV or any other ETF.

The end result is that we see lumpy creation and redemptions, reflecting accumulated buying or selling activity over a number of days.

In the case of large lumpy redemptions, that can reflect an AP who held on to GLD shares in the expectation they would be able to offload them later into expected buying. If that buying does not eventuate, then the AP offloads the lump of GLD share they have as they are incurring ongoing funding costs.

You are correct in that redemptions of GLD cannot really be used to infer too much about what is going on re investor sentiment. The GLD bought back by an AP and gold redeemed is just sold by the AP to someone else, ultimately.

All GLD holding movements tell us is the sentiment of GLD holders. All that futures tell us is the sentiment of futures traders. Are these markets representative of the all private investors in gold. Maybe, maybe not.

What commentators miss is the OTC "dark pool". Consider that ETFs + Futures only represent less than 10% of estimate privately held gold http://goldchat.blogspot.com/2010/08/gold-leader-board-july-2010.html

In that case, we should not get too excited by the activity we see with ETFs and futures as it is not where the real giants are.

Consider also that bullion banks know their activities in ETFs and futures can be seen/deduced in some way. Therefore you must assume they let you see what they want you to see, with their real position and activities hidden in the "dark" OTC market.

Usually in a bubble, investors are holding a bag.

Usually in a bubble, investors are holding a bag. As we’ve noted before, one-day declines in the holdings of this ETF of over 1% have tended to be capitulatory in nature and have typically occurred near important lows in the gold price during gold’s secular bull market.

As we’ve noted before, one-day declines in the holdings of this ETF of over 1% have tended to be capitulatory in nature and have typically occurred near important lows in the gold price during gold’s secular bull market.