Bob Moriarty recomendation

posted on

Jan 05, 2010 06:03PM

Edit this title from the Fast Facts Section

Bob Moriarty

Archives

Jan 4, 2010

During the last week of the year, I shot out to Spokane, Washington to visit two junior mining companies. I left early Monday morning and got back in time on New Year's Eve to duel with the amateur drunks. I use the word Junior lightly; one of those companies isn't going to be a junior for long.

In the last cycle, the Voisey's Bay nickel deposit was the "Really Big Thing." It contains 141 million tons of 1.6% nickel worth about $8.50 a pound right now. That works out to a theoretical metal in the ground value of $38 billion dollars.

Steve Jobs of Apple Computer is quoted as saying "The very best thing about the internet is that it gives everyone a voice." He's absolutely right. If you have a computer connected to the Internet, you have the ability to communicate to billions of people.

He is also quoted as saying, "The very worst thing about the internet is that it gives everyone a voice." He's dead right there as well; lots of people aren't worth listening to. You can find them on every chat board where the possession of a keyboard seems to mean that not only do you have a voice, everyone on earth should be forced to listen to you. I'm amazed at the number of people on chat boards who consider themselves experts on everything and they are going to share their knowledge with you.

It seems one of the best ways to show that you are an expert is to naysay everything and everyone else. This is really popular with geologists; you can pick nits off of every project.

On Wednesday of the last week in December I went to see a company named Mosquito Consolidated Gold Mines (MSQ-V). As you can probably surmise from the name, they own 100% of a giant copper-rich moly porphyry project near Boise, Idaho.

I'm a bit of a naysayer as well and the first thing they need to do is dump that name. It may have historical connotations to it but it's a rotten name for the owner of the world's largest open pit moly-copper project.

The project is called the CuMo project for copper (Cu) and moly. (Mo) Since the value of the moly is about four times greater than the copper, it seems to me that to be fair, the project name should be MoCu but that doesn't work very much better than Mosquito. I wouldn't be unhappy if they dumped that name as well and named both the project and the company Monster Moly.

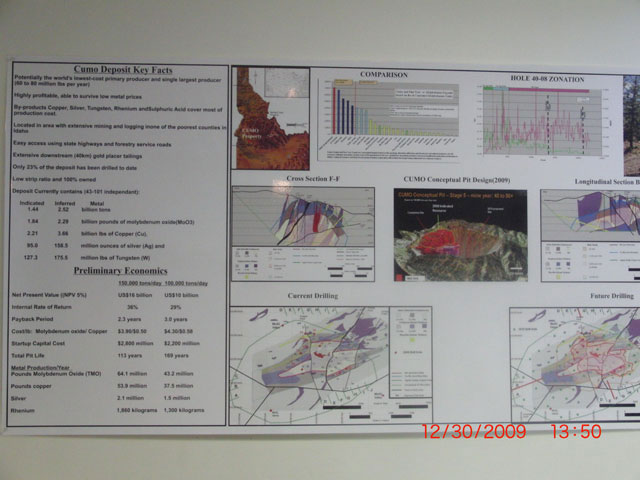

The company has drilled out a 43-101 resource of about 2.9 billion tons. That is monster. The value of all the contained metal is about $78 billion dollars using today's prices. There is moly, copper, silver, tungsten and an unusual element called rhenium.

Voisey's Bay only contains $38 billion dollars worth of nickel at today's price. When you want to compare Mosquito, think Voisey's Bay and double it.

I don't doubt for a moment that there are naysayers who would be quick to point out that minerals in the ground don't represent real value because you don't mine them all and you don't recover them all. That's perfect true. And perfectly meaningless at the same time.

But for the sake of argument, I went to Shaun Dykes, Exploration Manager for Mosquito. He worked up a similar spreadsheet for me showing the gross metal value on a recovered basis. It's still $66.9 billion. Wow.

If the naysayers are still not happy, on the 23rd of November, the company came out with a Preliminary Economic Assessment of Cumo. (PEA) This PEA shows two different models. One calls for production of 100,000 tons a day. That model shows a Net Present Value (NPV) of a mere $10 billion dollars. The model using a figure of 150,000 tons a day shows an NPV of $16 billion.

So take your pick, all of these numbers mean something. You can use $78 billion for a figure of metal in the ground on a gross basis. Or you can use $67 billion for gross metals on a recovered basis. Or you can use $16 billion dollars NPV for 150,000 tons per day production. Or you can use $10 billion NPV for 100,000 tons per day. The value of the company on Thursday Dec 31 was $71 million Canuk dollars. I'd say that's pretty cheap. Net Present Value ought to mean something but for now, it's not even close.

Based on the 150,000 tons per day production rate, the IRR is a healthy 36% with a 2.3 year payback period and a potential mine life of 113 years. Using the 100,000 tons per day figure, the IRR slides to a still healthy 29%, a payback period of 3 years and a potential 169 years mine life. The Capex for 150,000 TPD is $2.8 billion dollars and $2.2 billion for a 100,000 TPD rate.

The naysayers could say that the figure of $16 per pound for moly is unrealistic and moly could crash. That's perfectly true. And perfectly meaningless. Moly has crashed. Two years ago moly was $33 a pound. Moly dropped to $8 a pound in May of 2009 before recovering to $19 a pound in August of 2009. If the figure Mosquito was using was based on a price of $30 for moly it would be accurate to say there is a lot of potential downside. But using $16 moly isn't a bad number. At a production rate of 100,000 TPD, Mosquito can produce moly for $4.30 a pound.

On a per ton basis using current prices, the metal in the ground is worth about $22.59. Mosquito's estimated mining cost at 100,000 TPD is about $7.80. Those are far better margins than most gold and silver companies. And this a mine with a potential 150 year life.

The Capex is going to be big. 100,000 TPD is a giant mine. But these are giant numbers. $2 to $3 billion to get started is a good number. This is a situation where you want to be thinking off take and determining just who your customers will be. China comes to mind immediately. So the question now has to be, how do you get the Chinese interested? The answer is pretty simple, the Chinese already are involved.

China needs a reliable source of moly. China is the world's biggest steel producer and you need moly for steel. China has $2.3 trillion in foreign exchange reserves with much of it denominated in US dollars.

It's pretty much a use it or lose it basis. I don't think anyone seriously believes the US dollar will be around very much longer. With $124 trillion in debt on an economy only producing $14 trillion a year in GDP, it's obvious to anyone that can count that the US either defaults on the debt or goes into hyperinflation. I think it will be hyperinflation. If I owned a lot of US bucks, I'd be looking for something real to spend those soon to be worthless pesos. In that case, a high Capex project is far more desirable than a low Capex project.

Our resident naysayers may well want to point out that the US Treasury just blocked Chinese investment in a gold mine in Nevada called FirstGold. The Chinese were buying 51% of the mine for about $9.5 million. The Treasury maintained the mine was too near Fallon Naval Air Station located some 50 miles away as an excuse to kill the deal. I have no doubt others will disagree with me but the money involved was so tiny that for the US government to take the position that they are concerned with a $9.5 million dollar Chinese investment in a US company would be suicide on the part of the government. It's entirely possible that security issues were the concern.

The Chinese could buy up to 49.9% of Mosquito on the open market with no legal issues under various companies. In that case, as financier of the project, they would still be in the driver's seat. If the US government tried to stop Chinese investment in a Canadian company with an Idaho mining project, the day after the announcement, the dollar would drop 20% overnight as the Chinese flooded world markets with now worthless US government toilet paper.

In Economics 101 we are taught that when a country spends their national currency abroad, eventually that currency has to be traded for something they own or produce. Those US dollars abroad eventually have to return to the US in exchange for something. I suspect the Chinese have about as much US used toilet paper as they can stand.

All companies have very real issues. I had a long heart to heart talk with Shaun Dykes about Mosquito and I'm satisfied that the company is at least thinking about how to proceed. Their issues are identified and under control

When I was a young Marine fighter pilot, we used a phrase all the time that said, "If you have the name, you have to act the part." It was true then and it's true now. In my mind, this is a giant project. Mosquito needs to make a giant transition from acting like a junior collecting beanie baby mining projects to a major production company. Mosquito needs to expand the management bandwidth as fast as they can. They need to dump all the other meaningless projects into JVs with other juniors or spin them off into another company.

I have to compliment the company on having the foresight to pick up the project and to move it to this scale. With any multi-element project, it's often hard for investors to get a handle on just what the company is mining and what it's worth. With the price fluctuations of the last year, it has been especially difficult. But the Chinese are way ahead of ordinary investors on this deal. They were buying at $.35. They have so much skin in the game that no matter how the company moves forward, they are pretty much assured a giant profit. It is in their best interest to find another Chinese company that needs a 100-year supply of moly.

I liked the deal enough that 10 minutes after they started filling me in on the details, I called my broker and bought some shares. I don't see this as anything but a slam-dunk. 5% of the NPV of the 100,000 TPD rate would still be $500 million. Frankly I don't see why the company isn't there already.

Unlike Montana, Idaho is an extremely mining friendly state. I don't see any long-term legal issues; there is nothing in the mining that is particularly difficult or dangerous. It's an ordinary mining story times 100, that's all.

Back of the envelope calculations show mining could begin in 2015. I suspect the investment community will understand this story immediately. The company has put to rest the naysayers by providing a giant 43-101 and a PEA with rock solid numbers. They do need to do a lot of promotion but this is a story that tells itself.

There will be a new updated 43-101 released in March. Drill results from a monster hole will be out in about two weeks. Look for them. I expect something in the 400-500 meter range of $30-$40 rock. Time will tell but watch for them if you are not satisfied that they have the real deal right now.

We own shares. We are biased. The company would be insane to not advertise but literally I'm headed out the door on a trip to Europe and Africa and haven't had a chance to discuss advertising with the powers that be at Mosquito.

As always, you don't share your profits with us and we don't share your losses. You alone are responsible for your own due diligence. The company is approachable and I would encourage any potential investor to look seriously into the information available. I'd like to see the company do a major fund raising at a higher price and move this forward as soon as possible. Just after they change that awful name.

|

|

|

|

|

|

|

|

Mosquito Consolidated Gold Mines Ltd

MSQ-V $1.18 (Dec 31, 2009)

MQCMF-OTCBB 60.3 million shares

Mosquito Consolidated website

Bob Moriarty

President: 321gold