The Coming Week's Biggest Potential Market Movers

posted on

Oct 18, 2010 08:21AM

Edit this title from the Fast Facts Section

http://seekingalpha.com/article/230350-the-coming-week-s-biggest-potential-market-movers?source=dashboard_macro-view

COMING WEEK’S BIGGEST POTENTIAL MARKET MOVERS Systemic Risk From Foreclosure Scandal To Hit This Week? Watch US Big Banks Earnings Announcements We find it hard to believe markets can continue to ignore such a risk, though the timing of when the fear really hits remains elusive. Note also that it was only on October 13th that bank stocks as a group really began to dive, with the biggest names like Bank of America losing about 9% from Wednesday to Friday. Virtually all of the remaining marquee banking names report this week, including America’s 3 largest mortgage lenders, Bank of America (BAC), Citigroup (C), and Wells Fargo (WFC), as well as a host of less known but prominent financials. See the below earnings calendar highlights for details. Likely Ramifications QE 2 Enthusiasm Waning? PRIOR WEEK Noteworthy But Not Market MovingI haven’t felt this kind of impending trouble since Dubai World announced last November that it would halt its debt repayments. That action was bound to focus markets on the biggest unrecognized systemic market risk, what became the EU sovereign debt and banking crisis.

After reading about 90 pages of articles on the topic, I conclude we appear to have a new potential systemic risk in the US foreclosure fraud scandal. Simply put, massive uncertainty about the very sectors that ignited the global financial crisis that began in 2007 – US real estate and banking, the key sectors of the world's key economy.

The mechanics of how this has happened are beyond the scope of this article. The basic point is that as part of the process of bundling low quality mortgages into A-rated debt securities, we face uncertainty about who (if anyone) has valid title to the tens of millions of US properties worth trillions of dollars. This came about as a direct result of both negligence and outright fraud involving virtually every major name in America’s banking and mortgage servicing industry, as well as the US courts and regulators themselves.

We’ve heard of “too big to fail.” Do we now have “too big to prosecute?”

This in turn once again casts doubt on the value of the related mortgage-backed securities, and the balance sheets of the huge chunks of the US banking and real estate sector. Again, the key words are doubt, uncertainty. Markets don’t know how bad the damage is yet.

Cost estimates from asset write-downs and legal liability vary. A New York Times article Friday quoted estimates of $6-$10 billion for the banking industry, but also cited a widely circulated report from hedge fund Branch Hill Capital that suggested Bank of America (BAC) alone could face $70 bln in losses just from mortgage securities that it may be forced to repurchase from assorted investors.

That uncertainty alone risks being enough to send global markets of all kinds plunging.

This latest uncertainty, lest we forget, comes in addition to the rising wave of mortgage resets for the coming year, of a magnitude not seen since that of 2007-8 that spawned the subprime crisis.

The story has been brewing for some time, (and we highlighted it last as a potent market mover in last week’s review of coming market movers inUS, EU Banking Crises: The Other ‘Race To The Bottom’) but the issue only started hitting the major media and blog sites over the past week.

Global markets, however, have continued to show few signs of noticing the problem. As shown by the S&P 500 daily chart below (click to enlarge), equities closed higher this week, holding almost all of their roughly 12% gains since the beginning of September.

S&P 500 DAILY CHART 04oct17

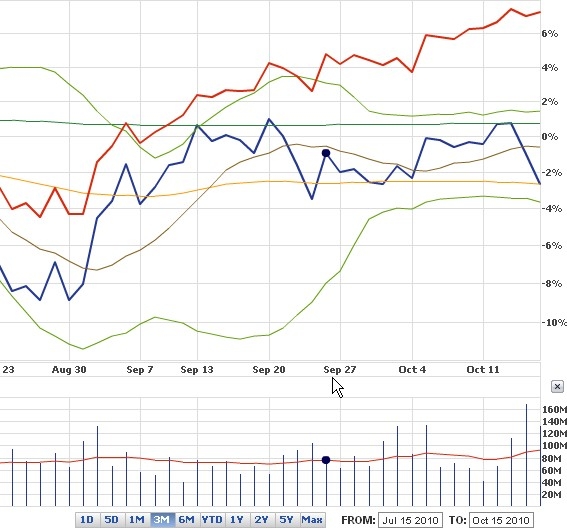

Cracks are appearing however. For example, the daily chart below (click to enlarge), of the financial sector ETF, XLF, shows the financial sector has not participated in the October rally on anticipation of new Fed stimulus.

Daily Chart Comparing Financial Sector ETF (XLF- Blue) vs. S&P 500 (Red) 02oct17 (hat tip to R. Hsu of Asia Edge)

Cracks are appearing however. For example, the daily chart below (click to enlarge), of the financial sector ETF, XLF, shows the financial sector has not participated in the October rally on anticipation of new Fed stimulus.

Daily Chart Comparing Financial Sector ETF (XLF- Blue) vs. S&P 500 (Red) 02oct17 (hat tip to R. Hsu of Asia Edge)

Their earnings reports and conference calls take on new importance as bank executives will face questions about their bank’s exposure to the scandal. Guidance for Q4 and beyond will likely include their assessments thus far of the near and longer term damage.

Concerns about deflation, a prime driver of Fed stimulus expectations, are another factor weighing on large US banks, which perform worse in lower interest rate environments.

Beyond the financial sector, the real estate sector itself is likely to suffer badly as title to anything with a mortgage from the last 5 years is now in question. On the bright side (?!) new and older properties unencumbered with questionable mortgages from 2005-10 may get an unanticipated lift. Maybe.

There’s nothing like a new threat of systemic risk to send markets into a sharp pullback and reverse most current trends. Though ‘foreclosuregate’ directly affects the US financial and real estate sectors, the flight to safety would likely give the USD some relief given the likely negative effects on global risk assets and currencies, though it’s unclear whether it would fare better than the JPY or especially the CHF, which has the advantage of a better underlying economic fundamentals vs. either the dollar or yen.

Even if markets can avoid a foreclosuregate inspired selloff, they cannot keep rising forever on expectations for new US QE, which has been almost the sole driver of risk appetite for over 2 weeks.

Consensus appears to be that additional anticipated stimulus should bring a 0.2% boost in GDP, yet markets have already risen about 5% since the Fed started telegraphing the move in early October, spurring a wave of commentary suggesting that QE 2 is already more than priced in, and potentially could disappoint in timing or size.

Other Key US Q3 Earnings Announcements

The pace of big name earnings announcements peaks next week with leaders in most sectors present. If markets can avoid a bout of profit taking from fears about US banking and housing, other major announcements could be significant for fueling or dousing the ongoing rally. Here’s a list of highlights from next week’s earnings calendar. We’ve highlighted the big bank announcements.

Their earnings reports and conference calls take on new importance as bank executives will face questions about their bank’s exposure to the scandal. Guidance for Q4 and beyond will likely include their assessments thus far of the near and longer term damage.

Concerns about deflation, a prime driver of Fed stimulus expectations, are another factor weighing on large US banks, which perform worse in lower interest rate environments.

Beyond the financial sector, the real estate sector itself is likely to suffer badly as title to anything with a mortgage from the last 5 years is now in question. On the bright side (?!) new and older properties unencumbered with questionable mortgages from 2005-10 may get an unanticipated lift. Maybe.

There’s nothing like a new threat of systemic risk to send markets into a sharp pullback and reverse most current trends. Though ‘foreclosuregate’ directly affects the US financial and real estate sectors, the flight to safety would likely give the USD some relief given the likely negative effects on global risk assets and currencies, though it’s unclear whether it would fare better than the JPY or especially the CHF, which has the advantage of a better underlying economic fundamentals vs. either the dollar or yen.

Even if markets can avoid a foreclosuregate inspired selloff, they cannot keep rising forever on expectations for new US QE, which has been almost the sole driver of risk appetite for over 2 weeks.

Consensus appears to be that additional anticipated stimulus should bring a 0.2% boost in GDP, yet markets have already risen about 5% since the Fed started telegraphing the move in early October, spurring a wave of commentary suggesting that QE 2 is already more than priced in, and potentially could disappoint in timing or size.

Other Key US Q3 Earnings Announcements

The pace of big name earnings announcements peaks next week with leaders in most sectors present. If markets can avoid a bout of profit taking from fears about US banking and housing, other major announcements could be significant for fueling or dousing the ongoing rally. Here’s a list of highlights from next week’s earnings calendar. We’ve highlighted the big bank announcements.

G-20 Meeting In South Korea Friday

There appears to be more potential for disappointment than major improvement in tensions on competitive devaluation, though expectations are not high. That means continuation of support for emerging market currencies, also commodities on continued USD weakness.

UK Comprehensive Spending Review (CSR) To Pressure the Pound And Broader Markets?

On Wednesday the UK presents both minutes of the Bank of England Monetary Policy meeting and details of its spending cuts to reduce the UK’s budget deficit, which currently stands at 11.5% of GDP.

Chancellor George Osborne announced GBP £80bn of cuts between 2010/11 and 2014/15, the equivalent of 6% of GDP over 5 years, with most departments due for 25% budget cuts.

UK austerity is believed by many to already be priced in, but we’re not so sure. The GBP has benefitted from austerity talk, but may suffer once the specific threats to GDP are clearer.

China Data

Wednesday Q3 GDP, September retail sales, industrial production, fixed asset investment. Last month this group helped feed a market rally, and could be influential again in the absence of other major surprises.

Other Key Economic Calendar Events

US

Main events beyond those cited above include numerous Fed speeches which together may provide some clarity about November’s assumed new stimulus. Remember that long term TIC flows will be reporting August net investment in US vs. non-US securities, which is too early to see how, if at all, certain nations are managing their own currency interventions. We’ll see that in next month’s report.

EU

EU finance minister discuss Euro reforms starting Monday, assorted PMI Wednesday and Thursday.

Continued Expectation That New US Stimulus Will Be Announced At Next Fed Meeting November

Consensus is that the anticipated roughly $500 bln of new stimulus will not add more than roughly 0.2% to GDP, yet markets are up for the past weeks nearly 5% on this alone.

Foreclosure Fraud Scandal Ramifications Hit Bank Shares, But Not Broader Markets

Concerns About EU Debt/Banking Crisis Quiet For Now

Axel Weber, head of the German Bundesbank, said that the ECB should stop buying the bonds of Europe’s peripheral economies, maintaining a relatively hawkish tone compared to the Fed. Spreads on bonds from the PIIGS have improved, and the ECB hasn’t bought much of their bonds over the past week. Markets ignored widespread strikes in France protesting pension reforms.

Conclusions

In sum, greater potential for reversal of current trends, primarily from events surrounding US earnings and the growing awareness of the extent of the US foreclosure fraud’s impact on the financial and housing sectors. Trouble in these can potentially take down global markets, and cannot be ignored.