Copper Prices On The Move: Near, Mid And Long Term Update November 28, 2011 |

posted on

Nov 28, 2011 01:59PM

Edit this title from the Fast Facts Section

BACKGROUND

The verdict is still out on copper. The market has not confirmed a bottom at 2.99, based on the front month spot price. The monthly chart pattern and the oscillators I use have not given buy signals yet. So, what is the near, mid and long- term picture? What is copper telling us economically? Questions that some answer, some wonder if they can be answered, while others still warn-- if you are looking for 100% certainty, don’t bet on copper to oblige.

Supply and demand will ultimately command direction and price. Copper remains closely correlated to the global economies and markets. Copper is an excellent conductor of electricity and heat and is used in technology, electronics and the automotive industries. The average auto carries between 45 to 100 lbs. of copper; PCs, mobile phones, tablets and many other electronic gadgets also use copper wiring and contacts. Commercial and residential construction have a long history of copper usage. The ubiquitous nature of copper remains an important indicator, as an uptick in demand would suggest recovery within the manufacturing and construction sectors.

The caveat is emerging economies fed by and led by China. Chinese demand for the “red bull” is expected to keep it in short supply into 2012. Demand should exceed supply in 2011 by 495,000 metric tons, a 50% year-over- year increase according to Japan’s largest producer (Pan Pacific Copper Co.) and drop back towards 31,000 tons in 2012. A downward change in Chinese demand would have a negative ripple effect throughout the sector.

Consider, prior to the urbanization of China that began in 2002, copper traded as low as $1,319 a ton and remained below $2,000 a ton for 5 years, recently peaking at $10,148 a ton in February 2011. Reports indicate that Chinese warehouses have depleted their copper stocks giving support to stronger imports by China. Market volatility will remain in the picture and possibly create some strong and quick swings of both price and emotion as reports increase or decrease China’s demand for copper.

Demand for copper has existed for thousands of years. A pendant discovered in northern Iraq dates back to approximately 8700 BC. The ancient Egyptians developed and used copper tubing. Archeological digs have found plumbing fixtures in tombs and temples of rulers, giving a strong testament to copper’s malleability since other metals are susceptible to corrosion. Gold dates back to 4000 BC, with an additional 1000 years passing before silver and lead were used. Over 10,000 years of history has secured copper's place as an economic indicator.

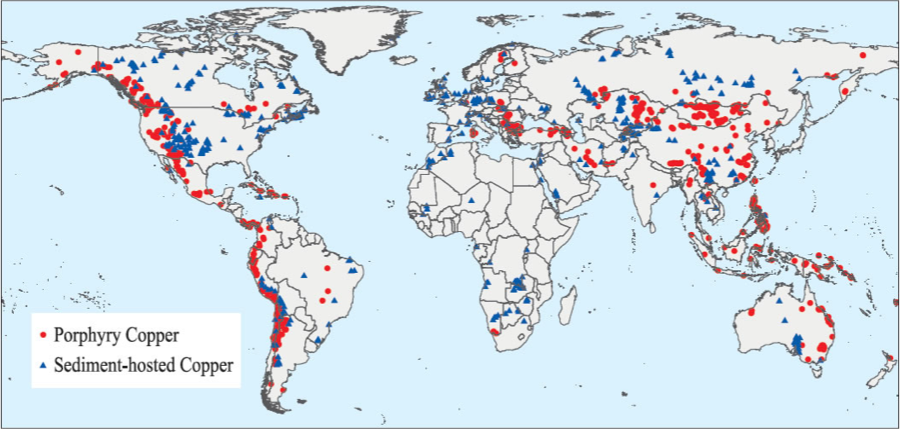

Four areas of the world contain 90% of copper reserves:

Familiar forms of copper include pure copper, brass (copper – zinc alloys) and bronze (copper – tin alloys).

United States History

Found mostly in the American West, large-scale copper mining began in the later 19th century, as developing mining techniques opened the way for increased exploration. Demand rose as the electrical and communications grids spread across the country.

The two main segments of industry in the U.S. are:

Major structural changes have altered the playing field over the past few decades. The United States held “by a country mile” the top producer and consumer positions of new mined copper. At their height, U.S. based companies controlled about 45% of the free world production, which included accounting for the majority share of the mine outputs in Chile and Peru.

Today, the U.S.’s share of world mine production is approximately 18%. Chile, with the largest reserves, exports most of their 23% share. Russia, China, Australia, Canada, and Zambia remain important players in mining sectors.

SUPPLY & DEMAND

Recycled scrap (copper, brass, bronze) accounts for more than half of all copper consumed in the United States. The ratio of ‘new’ scrap (production scraps) vs. ‘old’ scrap (electrical cable and auto parts) is roughly 55% to 45%. One third of recycled scrap is lost to the smelting or refining streams. Two thirds goes to brass mills that produce alloy ingots for fabrication use by foundries, powder plants and the aluminum, chemical, and steel industries.

Copper demand also comes from the building and construction sectors, the utilities sector (power generation and transmission), and the Industrial Manufacturing and Consumer Products sectors (electronics, industrial machinery, transportation vehicles, appliances, heating and cooling systems and telecommunications.)

The United States Geological Society (USGS) concluded back in the late 20th century that roughly 350 million tons of copper have been discovered (U.S. only) leaving approximately 290 million tons undiscovered. Globally, the numbers are 590 million tons discovered and 750 million tons (estimated) undiscovered.

Source: by USGS

Near, Mid, and Long-Term Pictures

Copper Spot Prices:

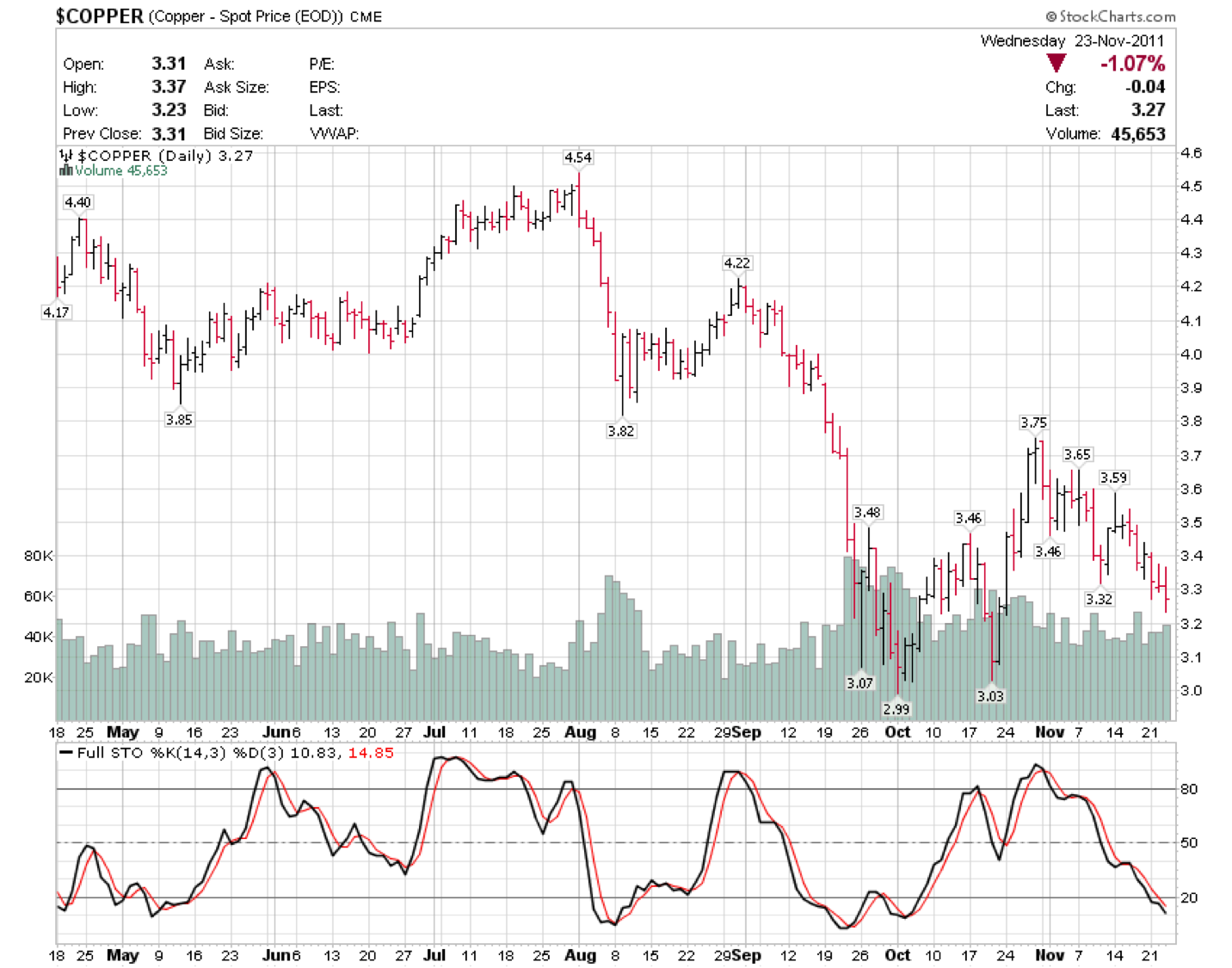

Copper sits at an important junction in terms of direction. The daily, weekly, and monthly charts paint a clearer picture.

Near term expectations are leaning more towards the downside. The boundaries for resistance and support are 3.59 to 3.32. A break of 3.59 with follow through would clear the path for at least a test of 3.75. Above 3.75 upside momentum could pick up some steam. A break below 3.32 with follow through should make way for additional downside and a retest, if not break of 2.99. Technically, an upside move would generate more energy with both the stochastic and RSI oscillators sitting right at oversold.

Click to enlarge

Mid-term, the pattern underway along with the oscillators suggests copper will have an easier time declining than building a strong advance. Support on a mid-term basis should come in at the 2.53 area and then 2.10 before the market would mount a sustained advance. Resistance to watch is the 3.75 zone. A break with follow through takes resistance (stronger) to the 4.54 zone. Technically, the stochastic oscillator is teetering on giving a sell signal, the RSI is pointing down right off of the overbought level.

Long-Term, copper prices may be lining up some buying opportunities, while copper carries a similar uncertain directional feel. The oscillators are moving into oversold readings, and additional downside would accomplish that. Momentum would likely force a test of 2.99 and a break and drop to support at 2.10. Long-term players might want to resist temptation and work out entry levels on a break below 2.99 (with follow through) or a break above 3.85 (with follow through).

Economic Indicator

From an article published in March 2011, I included statements from metalminer.com which remain valid today:

“In spite of some concerns that Beijing is trying to cool a potentially overheating economy, the commodities super cycle story, driven by Chinese demand, is still going full steam ahead. We’re not about to be provocatively contrary to that view, but we have our concerns that all of the presumed drivers may not be quite as full on as headline reports would have us believe, and for that reason we would call into question how much further copper has to go. “ (Source: metalminer.com)

Over the past few quarters it appears that the number of economic “wild fires” has increased, and we don’t know yet as to their containment or threat of spreading. At the same time, we are also witnessing selective growth across some sectors. The housing, construction, and manufacturing sectors have built in some price benefits from higher consumer spending. Chinese demand is expected to remain steady (at firm), which may ripple out and provide price support.

I stand in agreement with metalminer.com on concerns as to how much further copper has to go – either up or down. Keep in mind that the yellow caution flag remains out for now. The long, mid and near term pictures are all affected, and some portfolio realignment might be done on an “as needed” basis.

Economically then, some recovery (selective sector wise) should continue into 2012 if not 2013 – 2015. The broad based indices may even reach new highs in the process (albeit on negative input) and much of this will come from what comprises each index and what weight factor has been given to the components.

Copper and copper mining sectors may have seen the highs for the mid to long term. I would not be expecting new highs in spot prices or several of the focused mining companies anytime soon. If this is the case, the economic recovery will be limited and contained. Not wide or evenly spread out across a healthy growing middle class economy.

Producers

Lihua International (LIWA)

Lihua International, Inc. is principally engaged in the production of copper replacement cable and wire products, which include copper clad aluminum (CCA) wire and pure copper wire produced from refined scrap copper. The Company manufactures and sells three major types of copper replacement wire and cable products: CCA wire, pure copper wire and pure copper rod. The pure copper wire and pure copper rod products are produced from refined scrap copper utilizing its scrap copper recycling and cleaning technology and process.

Lihua International, Inc. has three different CCA products: CCA fine wire, CCA magnet wire and CCA tin plated wire. CCA fine wire is the raw material for CCA magnet wire and CCA tin plated wire. The Company sells its products primarily in China, either through distributors or directly to users, including distributors in the wire and cable industries and manufacturers in the consumer electronics, automotive, utility, telecommunications and specialty cable industries.

Fundamentally, LIWA is a small to mid cap stock. The current market cap is 187.1 million. Over the last four years LIWA has demonstrated good growth primarily due to the urbanization of China. Expectations for a pick up in Chinese demand should translate to higher prices over the near to mid term. Revenue growth has been explosive, reporting 32.7 million in 2007 and 370.5 million in 2010 (source 10-K). Currently on a TTM basis, the company is set to report more than 595.0 million for 2011. However, cash flow has not remained as steady – Total cash flow from Operations has dropped from 29.7 million in 2010 to 23.9 million currently with a large change in Working Capital beginning in 2009 at -19.1 million to -29.2 currently.

Technical Picture

The monthly (long term) chart pattern gives a strong indication that current or near to mid term strength will run into a resistance zone beginning at 7.30 and then 8.40, with 9.40 likely curbing upside momentum. The stochastic oscillator dipped into oversold reading back in June of this year, and has been moving sideways since. The RSI oscillator gave a buy signal in early November and continues to point up.

Click to enlarge

The weekly (mid-term) chart pattern carries the same resistance zone as the monthly. The stochastic oscillator gave a buy signal in early to mid-October. The RSI oscillator confirmed with a buy signal in early November. Together they give support to the 4.35 low remaining in place until the upside resistance zone is reached.

The daily (near term) chart pattern carries the same strong upside resistance zone at 7.30 to 9.40. Near term resistance should also be found at 6.55 to 6.75. Expectations (near term) would be for resistance to contain additional upside before a smaller dip back to support (again near term) at 5.45, 5.15, and 4.90 before the advance picks up again moving up into resistance at 7.30 to 9.40.

Mining Companies

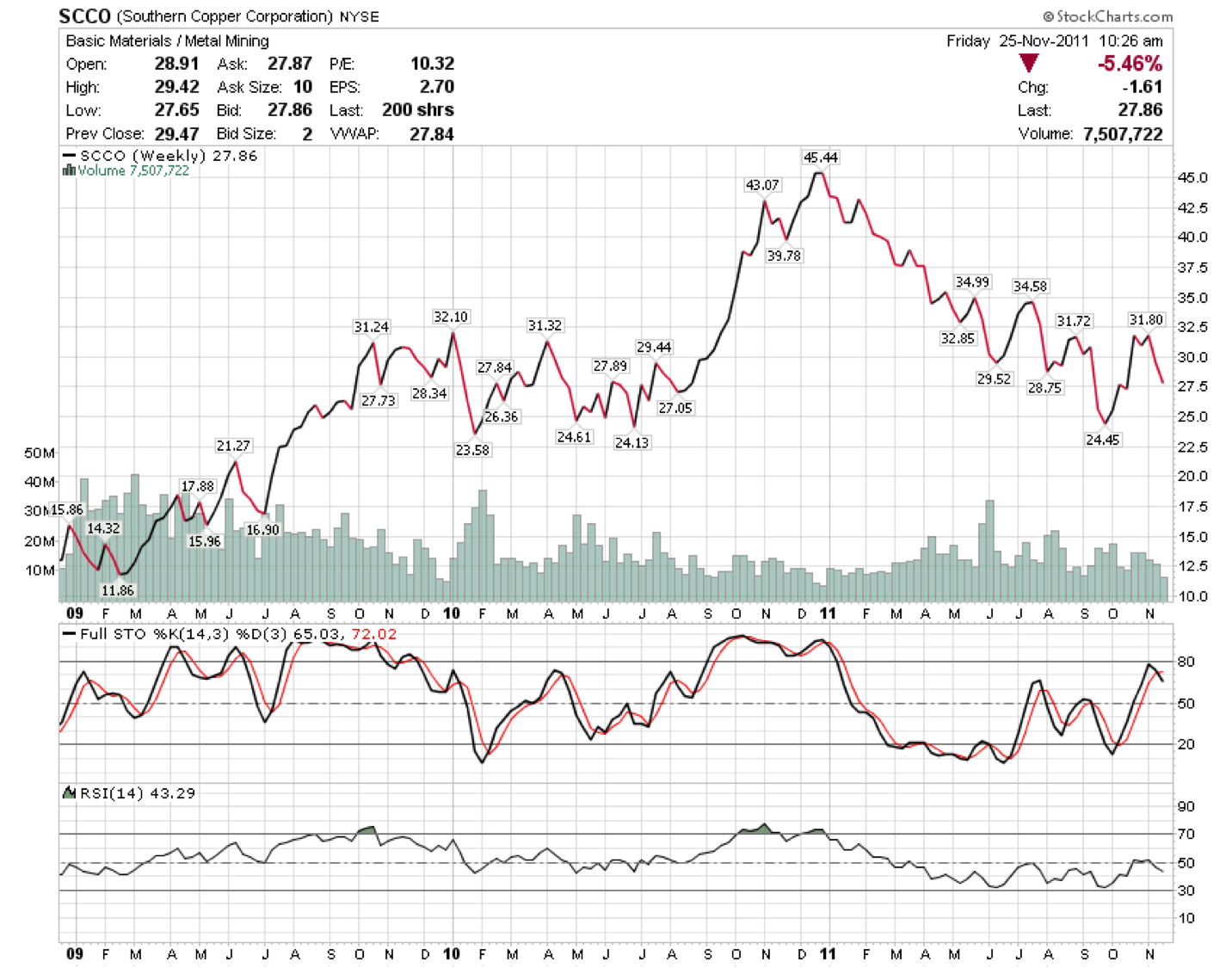

Southern Copper Corporation (SCCO)

SCCO Is an integrated copper producer. SCCO produces copper, molybdenum, zinc and silver. All of the Company's mining, smelting and refining facilities are located in Peru and in Mexico, and it conducts exploration activities in those countries and Chile. Its Peruvian copper operations involve mining, milling and flotation of copper ore to produce copper concentrates and molybdenum concentrates; the smelting of copper concentrates to produce anode copper, and the refining of anode copper to produce copper cathodes. The Company operates in three segments: Peruvian operations, Mexican open-pit operations and Mexican underground mining operations

Click to enlarge

Southern Copper's current market cap is 24.9 billion, SCCO trades at a P/E of 12.5 with an EPS of 2.35, yielding 8%.

Near term support at 27.75 was reached, and momentum may push prices to next support at 26.75 before an upside move begins. Near term resistance begins at 29.50 to 30.50 (pause only) and then 32.80, 34.10.

Mid term support remains at the 24.45 low (weekly closing basis). A break below this level may accelerate any downside momentum. Mid term resistance (stronger) comes in at 32.80 and then 35.25 to 37.75.

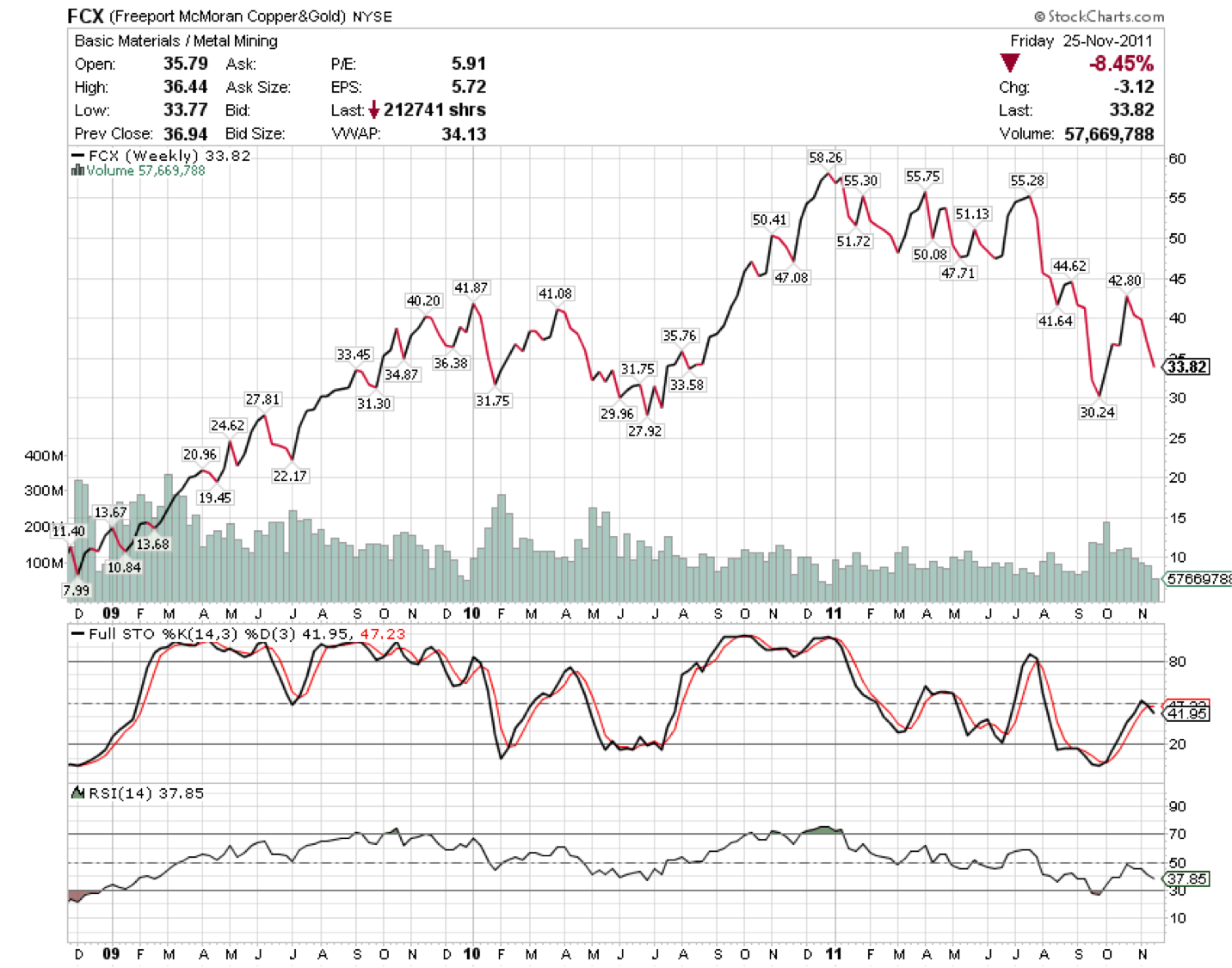

Freeport – McMoRan (FCX)

FCX is a copper, gold and molybdenum mining company. Its portfolio of assets includes the Grasberg minerals district in Indonesia, mining operations in North and South America, and the Tenke Fungurume (Tenke) minerals district in the Democratic Republic of Congo (DRC). The Grasberg minerals district contains the recoverable reserves of copper and the gold reserve. It also operates Atlantic Copper, its wholly owned copper smelting and refining unit in Spain. FCX operates seven copper mines in Arizona, and New Mexico. It operates four copper mines in South America in Peru, and Chile. In Indonesia, PT Freeport Indonesia operates the mines in the Grasberg minerals district. In Africa, Tenke Fungurume S.A.R.L. (TFM) operates the Tenke Fungurume (Tenke) mine.

Freeport - McMoRan relies on revenue from a continued global urbanization, making Chinese and Indian demand key to meeting expectations. With a market cap of 35 billion, FCX also owns and operates gold mining operations in addition to copper mining operations.

The break of near and long term support at the 35 level suggests standing aside for now in FCX. If you are a long term trader with an existing position, the current outlook includes the potential for a drop back to the 29.30 area before FCX will mount a sustained advance. Once FCX does turn higher there will be stronger pockets of resistance to get through over the mid term. The zone begins at 41 and eases up at the 47.50 area.

Click to enlarge

Bottom Line

Even though I feel the top may be in for the mid to long term for copper and its supply chain, there will be multiple opportunities for near, mid and long term traders. Be sure to include due diligence to insure these sectors meet your criteria and trading objectives.

Disclosure:

I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.