Gold, silver heading up: Roger Wiegand The Gold Report | February 16, 2012

posted on

Feb 16, 2012 11:34AM

Edit this title from the Fast Facts Section

Roger Wiegand, editor of Trader Tracks, says cycles will bring gold and silver higher in the first half of 2012: gold up to $2,050/oz and silver up to $44/oz or even $50/oz. He sees plenty of opportunities for volatility given the political and economic situation in the U.S. and the EU. In this exclusive Gold Report interview, Wiegand reveals names of mining companies poised to profit.

The Gold Report: Roger, you attributed the recent uptick in the gold price in part to large funds bidding up the price. But these funds have also shown their willingness to sell their gold positions to cover their short positions. Can gold investors look forward to more volatility this year?

Roger Wiegand: Gold is coming back very strongly right now. People in India, China, Japan and Canada are buying lots of physical gold. In addition, some central banks that were selling gold are now buyers.

We anticipate two more rallies between now and the end of April. On the six-week rallies, we should go up to $1,807/ounce (oz), then pull back, then go up to $1,923/oz, then pull back, and go on up to $2,050/oz by June.

TGR: Is the upward price pressure driven by funds coming back into gold, or is there something else?

RW: That’s a large part of it, Brian. If a big fund comes in and buys the CRB Commodities Fund Index, it has to place quite a bit of cash.

There are eight or nine commodities in the CRB. For example, if a fund buys a basket of commodities for $100 million (M), half of it would be crude oil, along with gold, silver, grain and a variety of other things. When a fund buys a basket like that, it cannot move too quickly because of the amount of cash invested. Normally, it would be looking at a minimal 90-day trading operation. If the prices turn against it, the fund can leave with the click of a mouse. But normally it rides the intermediate trend working to stay in the trade for several weeks.

In August, someone paid $25M for 10,000 gold spreads, priced between $1,900/oz and $2,300/oz. Another order came in last week for 5,000 more contracts, which went as high as $2,600/oz. Somebody with a lot of money, probably a big bank or a fund, is buying long spread positions in gold all the way from $1,900/oz to $2,600/oz.

TGR: Are you piggybacking on that?

RW: We are not out that far yet. My highest position for the first half of 2012 is close to $1,900–2,000. Other analysts are coming up with similar numbers.

TGR: Throughout Q411, the gold price remained weak, largely on concern over the situation in Europe. What is your best guess as to what happens next in Europe?

RW: Greece will default, but I think it will be an orderly default. I think Portugal will default. Italy and Spain are on the edge, but they are so big that a way might be found to manage them.

If things get disorderly in Greece, it could cause a contagion that would spread across Europe very quickly. First, stock markets would crash. Second, and more importantly, it would mess up the bond markets, which are 70 times larger than the stock markets.

The U.S. banks have big investments in Europe. If things go upside-down in Europe, New York will be in a world of hurt. Japan and China also have investments and export markets in Europe. Everybody is tied together in this problem.

When the stock markets are at their weakest and most vulnerable, they are prone to a big selloff, a selloff that some people would call a crash. I consider it a crash when the selloff is 50% or worse. A 20% selloff, which some people call a crash, I call an adjustment.

Consider gold as an investment during an adjustment. If gold goes to $2,450/oz by the end of 2012 or early 2013, there will be normal, profit-taking correction. When that happens, the gold price could drop back to $1,920/oz. People will say that is the end of the gold market. Not true. It would be just another correction that happens to be wider than previous corrections. We have repeatedly reported the precious metals would trade with more volatility and wider daily trading ranges, and when a correction arrives, it would be large.

TGR: As your followers know, you’re a technician. What do your charts tell you about macro trends for gold prices in the short, intermediate and long term?

RW: Short term, which for us would be two to four weeks. We are now doing the typical ABC correction after a five-wave up on Elliot Wave. At the juncture when the ABC is done, normally the price is will go higher on a new rally, starting all over in five waves up, or the ABC will turn into a five-wave trade down. That could happen as many as three more times by spring.

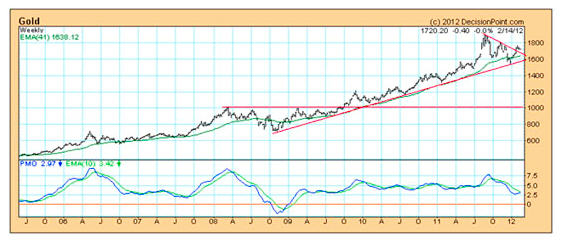

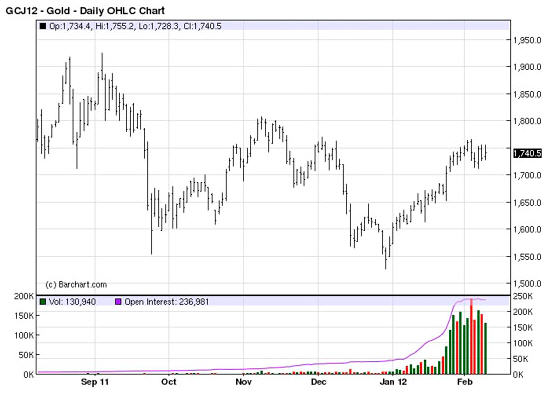

For example, looking at my April futures chart , I see gold at a low of $1,524/oz and a high of $1,758/oz. The support in the middle of the chart is about $1,607/oz, maybe $1,615/oz. If we had a harder sell before the middle of March, it could go down to roughly $1,632/oz.

In the intermediate, which would be three months, we are looking at a couple more cycles for both gold and silver. By the end, we expect gold will be at $1,923/oz. If we are fortunate, we will go all the way to $2,050/oz. And a newsworthy event could drive the investment posture higher.

The long view, which covers all of 2012, is tougher to figure. This is largely due to the inability to pinpoint what will happen in politics, government and markets for Q412. Our posture right now is to stay out of it and watch what happens over the next three or four months.

TGR: In 2009, you made a 95% return by trading spreads on gold, silver and soybeans. What sort of offbeat trades are you making now to mitigate risk?

RW: The open trades now in our newsletter would be silver for March, multiple gold spreads for April, May spreads for crude oil and silver, gold for June, and a July spread for corn.

We are pretty loaded-up on gold and silver, with the bias toward gold. The silver market got a good whack on the head when it went from $49/oz to $26/oz. When a market gets hit that hard, it usually takes six to eight months to come back. This morning, silver was $34.45/oz, with a lot of congestion between $30.48/oz and $34.48/oz. When silver can get past $34.48/oz, it should be a quick move to $36/oz, then $38/oz. My low-side minimum forecast for silver in the first half of 2012 is $38.85/oz. We have a pretty good chance of getting up to $41.44/oz.

If things really begin to get quite volatile this year, I think you could break $50/oz. Our next higher number for silver is $59.85/oz. Some of our smart analyst friends who are a little bolder, have numbers in the $60s and one is even above $70/oz.

TGR: What are some silver plays that are well positioned to capitalize on buoyant silver prices?

RW: Endeavour Silver Corp. (EDR:TSX; EXK:NYSE; EJD:FSE) has been very good to us for a long time. Its price today is $10.97. The company is well managed and it has some very productive properties in Mexico and Chile. It has matured from an explorer into an intermediate operating miner. In 2010, it produced more than 3 million ounces (Moz) silver and 17 thousand ounces (Koz) gold, and 2011 was even better. Its property in Mexico just seems to get bigger and bigger. We would highly recommend that people who own it hang on to it.

TGR: It is trading not far from its highs. Can it go much higher?

RW: Silver and gold companies follow the price of the underlying metals.The silver market being knocked back to $33/oz from $50/oz probably had more of an effect on Endeavour than issues internal to the company. When the silver prices begin to rise, share prices will follow. We think Endeavour’s shares have a long way to go on the high side simply because of its production.

TGR: Are you bullish on other silver stories?

RW: We have two. One is Comstock Mining Inc. (LODE:NYSE.A), which is in the Comstock Lode silver region in Nevada. It has a wonderful story. The price was as high as $3.75/share, then got stuck near $1.75 on a silver selloff. That is about as low as that stock is going to go in our opinion.

A six-month delay in obtaining drill permits held the stock back. Right now, we think it is headed back to its previous highs and perhaps higher. The company also had a change in management. Its new manager knows what he’s doing. The primary owner has spent a lot of money to get the company set up. This is a longer view opportunity, not a short-term trade.

TGR: Is there potential for further discoveries on its existing property?

RW: Absolutely. Now that it has the drilling permit, the company can expand within the property. It is in one of the most prolific mining areas in the history of the U.S., the legendary Comstock. The current owner of Comstock Mining bought up a lot of lawsuits, got everybody paid, took over the property, put the assembly together, then got a team and started drilling, and off we go.

TGR: If it took so long to get drilling permits, won’t it take even longer to get mining permits?

RW: Perhaps. Permitting is always a problem. But Nevada is mining friendly, so it will get going. It will have a longer view, but the fundamentals are good.

TGR: What is your other silver story?

RW: It is Global Minerals Ltd. (CTG:TSX.V; DPF:FSE), in Slovakia. This is an old mine with tremendous reserves. Management has cash. Slovakia is a modernized country.

Global Minerals has a high-grade, silver and copper antimony vein-type deposit in a historic mine district in the eastern part of the country. The mine has four horizontal, underground drifts, totaling 3,000 meters. It has the cash, it can get the permits, it is in a mining friendly area and it has good management, but it needs time to pump water out of the mine. That process should be finished in May. Then, exploration and drilling can expand.

At this point, we are keeping an eye on it. When the dewatering is done and drilling begins, I think the stock will move. The reserves are incredible—14 Moz silver, 48 million pounds (Mlb) copper, Measured and Indicated. In addition, it has 13.5 Moz silver and 29.8 Mlb copper Inferred. I think that it has a long way to go on the upside, based just on reserves.

The stock is now at $0.51/share. Granted, it is a risky company, but I think it is pretty exciting.

TGR: As part of the EU, Slovakia is one of the few countries with a significant rate of gross domestic product growth projected for 2012. If this is an old mine, why has it taken until now for a company to bring it to market?

RW: Remember that Slovakia was under a Communist regime for some time. There was no capitalization or major investment there for many years. Once it joined the EU, there was a lot of consumer and commercial growth. Mining usually comes later. Someone had to buy the property, get control of it, lay out budgets and get ready to mine. That does not happen very quickly. So it has been a question of politics, of growth and of getting a company in there that knows what it is doing to make it work.

TGR: Again, there could be permitting issues.

RW: Permits are always a risk, but the impression I have is that it is located in a mining-friendly region.

TGR: Let’s move to gold equities, some of which have shot out of the blocks this year. What are some of the names you follow?

RW: There are two that really stand out. One is Timmins Gold Corp. (TMM:TSX.V; TGD:NYSE.A). It is in Mexico. We have met and had presentations with the management; we have gone over this very carefully and have recommended it for a long time.

The beauty of Timmins is that it seems to move faster in a gold or a silver rally than others. The stock is trading around CA$2.82 but we see it doing much better based upon the performance of gold and silver this year. The company has delivered: it upgraded the mine and has top management and good growth. Bruce Bragagnolo, who is in charge, is an attorney in Vancouver who has been around the mining business a long time. He knows what to do and has good control of the company.

Timmins has expansion opportunity and is on a steady path for growth. We like a producing company at this share price.

TGR: Initially, Timmins had trouble with its San Francisco mine in Mexico, but in December 2011 it produced 8,500 oz gold, its best month ever. Its stated goal is to produce 100 Koz annually from the San Francisco mine. Consistent production of 8,500 oz/month would put it above that. What are its chances of doing that?

RW: I would say good. Timmins is very careful about its forecasting, measurements and dimensions of everything it does. Everything it has said it was going to do, it did, and on schedule. That is hard to do in the mining business. Timmins has upgraded all of the equipment, it has cash on hand and it is in a safe spot as far as its operations are concerned. We just think this will be one of the real good ones.

TGR: What about another?

RW: Our other one, which is a bigger, is Pretium Resources Inc. (PVG:TSX; PVG:NYSE). Bob Quartermain, who founded and built Silver Standard Resources Inc. (SSO:TSX; SSRI:NASDAQ), is the president. After Bob retired, he bought two key properties from Silver Standard, raised a lot of cash and got Pretium moving very quickly.

Pretium has the Brucejack gold mine in British Columbia, where it discovered some major glory holes with extremely high values. It raised more than $280M in 2011. It hit the ground running, with a plan for 50 geologists and engineers, 3 helicopters and 70,000 feet of drilling. Brucejack has high-grade gold resources stated at 5.06 Moz gold Measured and Indicated and 3.33 Moz gold Inferred. It has additional feasibilities and more drilling still going on.

Considering the quality of the management and its past performance, the funding, the location and what it has done so far, one analyst forecast Pretium at $33/share. The stock is trading around $17.08 on the New York Stock Exchange (NYSE) and the trading range runs from $8–17/share. We recommended it at $6.50/share. It went to $13/share, and we said take the profits. It came back to $8 or $9 a share and the chairman of the company bought $15M shares on the open market for himself—that is belief in your product. Then, of course, the stock just went up again.

What really got Pretium moving was being listed on the NYSE. Readers should keep in mind that when a stock goes from the NYSE Amex Equities or from the Toronto Stock Exchange to the NYSE, it goes to the head of the line as far as the big money investors are concerned. In my view, Pretium has a lot more upside than most of the others on the NYSE. We can easily see a double on Pretium over the next couple of years.

TGR: As part of your efforts to teach people how to invest more effectively you are offering a chart training class April 26 in Tempe, Ariz. What will your students learn?

RW: This will be a one-day event in conjunction with the Gorman Resource Wealth Conference, which follows in the two days after my event. I am going to guide people through some simple charting exercises and examples. People will get a workbook and I will show slides. They can ask questions. I am going to release some proprietary data, so people can understand what I am trying to do and what they can do on their own. I want to make things as simple and as straightforward as possible.

People who would like to attend can call Linda Gorman of Resource Consultants at 800-494-4149 or 480-820-5877 to register for both my trading class and the Gorman Wealth Conference. The Wealth Conference is headlined with six nationally known speakers including myself.

It’s going to be a lot of fun, and I’m looking forward to it.

TGR: Roger, thank you very much for talking with us today and good luck with your class.

For more of Roger Wiegand’s ideas about investing, read his interview in The Energy Report.

Roger Wiegand, aka Trader Rog , produces Trader Tracks Newsletter, a weekly publication to provide investors with short-term buy and sell recommendations and insights into the political and economic factors that drive markets. An insatiable reader, he digests a variety of domestic and international publications and weaves the economic, political, monetary and market news and commentary into his opinions and analyses. After 25 years in real estate, Wiegand has devoted intensive research time to precious metals, currencies, energy and financial markets for over 18 years. His varied background, which also includes graphics, writing, editing, sales, marketing, commercial printing, consulting and trading, helps shape the view he shares. Wiegand also pounds out a weekly “Rog’s Corner—After the Bell” column for Jay Taylor’s Gold, Energy & Tech Stocks newsletter. You can read and hear him on the Korelin Economics Report for daily opinions and market trends. Wiegand has been writing essays on Kitco and providing audios and interviews. He is a featured speaker at wealth and resource conferences around the year. Visit webeatthestreet.com or contact Claudio Bassi at 718-457-1426 for newsletter subscription information.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

Source: Brian Sylvester