The Graphite Investment Boom Is Just Starting

posted on

Apr 12, 2012 08:26AM

Edit this title from the Fast Facts Section

http://seekingalpha.com/article/489981-the-graphite-investment-boom-is-just-starting

Introduction

Graphite is quietly emerging as a strategic industrial material in short supply, similar to the rare earth commodities. Years of underinvestment in new supplies, and growing demand sources, have caused prices to rise sharply in the past few years. China, as the world's dominant supplier, has significantly curtailed exports in an attempt to exert greater control in the market. As a result, it's not entirely surprising that the EU named graphite as one of 14 critical materials along with the rare earth elements.

EU Names Graphite a "Critical Material"

A new global rush to find quality graphite supplies has just begun. However, not all graphite is created equally, and there is significant quality variation that determines its price and value, which can range up to a few thousand dollars per ton. When investing in graphite companies, it's essential to find the emerging producers with the right quality graphite to supply the fast growing end markets, assets with proximity to infrastructure, and a management team with skin in the game that can advance the mining project. I believe the two best companies positioned for significant valuation expansion are Northern Graphite (NGPHF.PK) and Zenyatta Ventures (ZENYF.PK).

Overview of the Graphite Market

Graphite, commonly known for its use in No 2 pencils, is quietly finding new applications that are poised to greatly expand its demand in the coming years. Currently, graphite is primarily used in the steel industry where it is added to bricks which line furnaces to provide strength and resistance to heat, used to line ladles and crucibles, and added to steel to increase carbon content. In fact, Japan is the largest world importer of graphite, and will almost certainly boost imports in the coming years as they set to rebuild infrastructure in the wake of the devastating earthquakes they recently experienced. Graphite is also used extensively in the automobile industry in gaskets, brake linings and clutch materials. It has a myriad of other industrial uses including electric motors (carbon brushes), batteries, lubricants and pencils.

Near-Term Demand Driver: Lithium-ion Batteries

However, its largest potential market is for lithium-ion batteries to support increased production of hybrid electric vehicles ("HEV") and electric vehicles ("EV"). It is estimated that there is over 2 to 3 kgs of graphite in a HEV and 25-50 kgs in an EV using lithium-ion batteries. Almost every major automotive producer currently has or is working on an HEV or EV. Examples include the Chevrolet Volt and the Nissan Leaf. Canaccord Capital Inc. estimates that the HEV and EV market will grow to 11 million units by 2015 and that by 2020 the market penetration rate of HEVs and EVs will reach 10-20%. According to Canaccord, this will increase incremental global lithium carbonate demand for battery applications by 286,000 tons. The natural flake graphite required to meet this demand is over 1.5 million tons, which is well above current annual worldwide production of natural flake graphite.

The spherical or potato shaped graphite used in lithium-ion batteries can only be made from flake graphite that can be economically purified to 99.98%C. Only 40% of the one million tons of graphite produced annually is flake and not all is suitable for lithium-ion battery applications. Synthetic graphite offers the only alternative to natural graphite for the manufacture of lithium-ion batteries. However, natural graphite has a performance advantage, although the gap is narrowing, and it is much less expensive as synthetic graphite is made from petroleum coke which is tied to the price of oil.

Future Demand Driver: Graphene

New discoveries in graphene, a derivative of graphite, may greatly expand graphite demand in coming years above and beyond levels currently contemplated. Graphene is essentially the thinnest one-atom thick layer extracted from graphite. Graphene is believed to be one of the strongest, lightest, and most conductive materials and could have major technological applications. The following articles and video illustrate the magnitude of recent research discoveries. The Nobel Prize in Physics was awarded to researchers examining the properties of graphene. While it still may be early to estimate the timing and size of grapheme and its applications making it into commercial production, it's clear that exciting opportunities exist. I encourage you to watch the video posted below to see the exciting applications being worked on.

Flexible Touch Screen Made with Printed Graphene

Future Demand Driver: Pebble Bed Nuclear Reactors

Another potential major demand driver in the coming years may be from the growth of Pebble Bed Nuclear Reactors. A Pebble Bed Reactor ("PBR") is a small, modular nuclear reactor. The fuel is uranium embedded in graphite balls the size of tennis balls.

PBRs have a number of advantages over large traditional reactors in addition to their lower capital and operating costs. First, they use an inert gases rather than water as a coolant. Therefore, they do not need the large, complex water cooling systems of conventional reactors and the inert gases do not dissolve and carry contaminants. Second, its passive safety removes the need for redundant active safety systems. In other words, a PBMR cools naturally when is shut down. Finally, PBRs operate at higher temperatures which makes more efficient use of fuel and they can directly heat fluids for low pressure gas turbines.

The first prototype is operating in China and the country has firm plans to build 30 by 2020. China ultimately plans to build up to 300 gigawatts of reactors and PBRs are a major part of the strategy. Perhaps, this explains why China has significantly tightened its grip on its own graphite supplies and been restricting world exports. Small, modular reactors are also very attractive to small population centers or large and especially remote industrial applications. Companies such as Hitachi are currently working on turn key solutions. Researchers at West Virginia University estimate that 500 new 100 GW pebble reactors will be installed in the US by 2020 with an estimated graphite requirement of 400,000 tons. This alone is equal to the world's current annual production of flake graphite without taking into account PBMR demand from the rest of the world, growing industrial demand and growing demand from other applications such as Lithium-ion batteries. It is estimated that each PBMR requires 300 tonnes of graphite at start up and 60-100 tonnes per year to operate.

Graphite is in the Early Stage of its Cycle like Rare Earths Were in 2009

The U.S. Geological Survey provides an excellent overview of the current state of the Graphite market:

The U.S. has no current production, and is entirely dependent on imports. China, Canada, Mexico, Brazil and Madagascar account for 98% of the total tonnage produced. While China produces an estimated 80% of the world's graphite, it only exports 40% of production due to its own internal domestic consumption. In addition, China currently imposes a 20% export duty and a 17% value-added tax on graphite, and an export permit is required. Given stagnate graphite prices for most of the past decade, Chinese production is at similar levels to 2001. Lack of investment and mine planning, the closure of marginal operations and the fact that mines are getting deeper and older, leads to questions about the ability of supply to increase in the coming years to meet expanding demand. The recent increases in graphite prices are signaling the impending supply/demand imbalance.

According to a recent report by Industrial Minerals magazine, the global graphite market is experiencing a "limited availability" of material and that "the days of cheap abundant supply from China is over" as demand and prices continue to surge. Prices for a range of grades have continued to rise since the start of the year as supplies from China, the world's biggest graphite producer, have experienced shortages owing to seasonal shutdowns over the winter period and restricted supply. All graphite mines from the main mining area in Hunan province in China have been closed for extended periods, constraining supply. The Hunan province, usually producing 200,000 tpa or more amorphous graphite a year, has been very strictly controlled since September 2010.

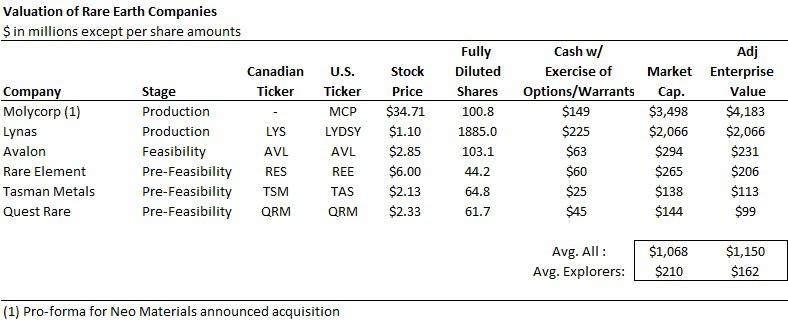

I believe the Graphite cycle is now where Rare Earths were in 2009. The companies that were early to identify and progress their assets saw significant valuation expansions. Take for example Avalon Rare Metals (AVL). Its market cap was tiny at under $50m in 2008-2009. As the world started to realize China's dominance in rare earth would cause major strategic shortages, AVL saw its market cap swell to nearly $1 billion even though they'd never produced 1 ounce of material. Today, the company still boasts a $300 million market cap and is still years away from production. AVL was viewed as a first mover in the emerging producer stage, much like NGC is today. Numerous other companies followed AVL in announcing rare earth finds, raising capital and listing their shares. Today AVL is joined by other explorers such as Rare Element Resources (REE), Tasman Metals (TAS) Quest Rare Minerals (QRM). Molycorp (MCP) and Lynas (LYSCF.PK) who quickly made it into production by re-starting old mines now carry billion dollar valuations. Nonetheless, the aspiring rare earth explorers still have large enterprise values in the hundreds of millions, and are still years away from production.

Click to enlarge.

Two Companies Positioned to Benefit from the Graphite Boom

Below I've outlined my two favorite graphite investments, each for different reasons, but both with significant upside potential.

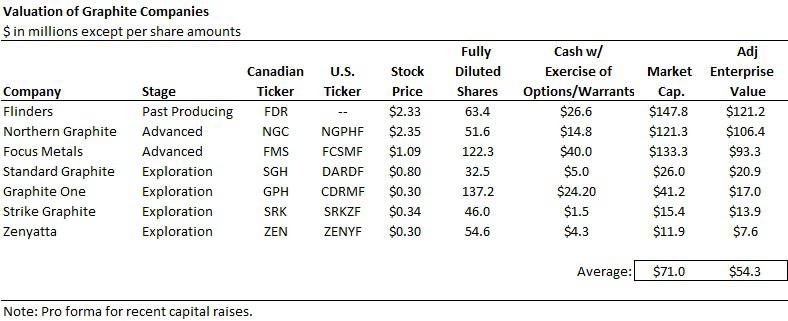

Northern Graphite (NGPHF.PK)

Northern Graphite is by far the blue chip graphite investment in Canada. The company has a large, well-known deposit called the Bissett Creek project. Below I summarize the key highlights of the company and its asset.

Key Highlights

It's easy to see why NGC has garnered so much attention from the business and investment community recently. Given the mine current economics, it's entirely possible the NGC's shares can easily double from here to over $6/share. To arrive at this figure, I conduct an NPV analysis with $30m/yr of cash flow, 40 year mine life, and a 10% discount rate. Analysts estimates have been rising recently as the company has delivered successively positive news results that confirm the quality of its graphite. For example, Mackie Research recently upped their price target to $4.40 per share. As the project gets further de-risked with the release of the BFS, and announcement of an off-take agreement, the price targets will continue to rise toward my full valuation.

There are other useful things potential shareholders might want to review as part of their due diligence. For example, the video entitled "The Miracle Material: Graphene" highlights NGC as the one company sitting on billions of dollars of graphite capable of supplying the high growth market for graphene. At the end of the video, there is a partial interview with NGC's CEO.

BNN, the premier business new network in Canada, also recently hosted NGC's CEO last month in an interview. This was a pleasant surprise to see a company with under a $100m market cap to appear on their national TV.

Zenyatta Ventures (ZENYF.PK)

Zenyatta Ventures is less advanced and more speculative at the moment than NGC, but holds potential for much greater upside. The company recently identified what appears to be a very large graphite deposit of high value.

Key Highlights

Summary

The investment community if finally realizing the large supply/demand imbalances that are occurring in the graphite market. I believe we are in the early innings of boom in graphite demand for alternative energy and technology applications, yet the supply-side has failed to adjust because of many years of underinvestment. China's changing policies in the recent years are the main driver; a decade ago, they flooded the market with cheap graphite which depressed prices and suppressed new mine development. Now that China has restricted graphite in a similar fashion to its rare earth policy, graphite prices have risen significantly. The company best positioned to profit from these changing trends is Northern Graphite due to its high quality graphite asset and earliest start towards production in late 2013. Zenyatta Ventures is also an intriguing investment opportunity with its recent graphite find, compelling valuation, and pending catalysts that should unlock value for shareholders.

Disclosure: I am long NGPHF.PK.