2 Cheap Gold Miners Providing Positive Production Guidance February 7, 2013 |

posted on

Feb 07, 2013 09:25AM

Edit this title from the Fast Facts Section

Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in NGD over the next 72 hours. (More...)

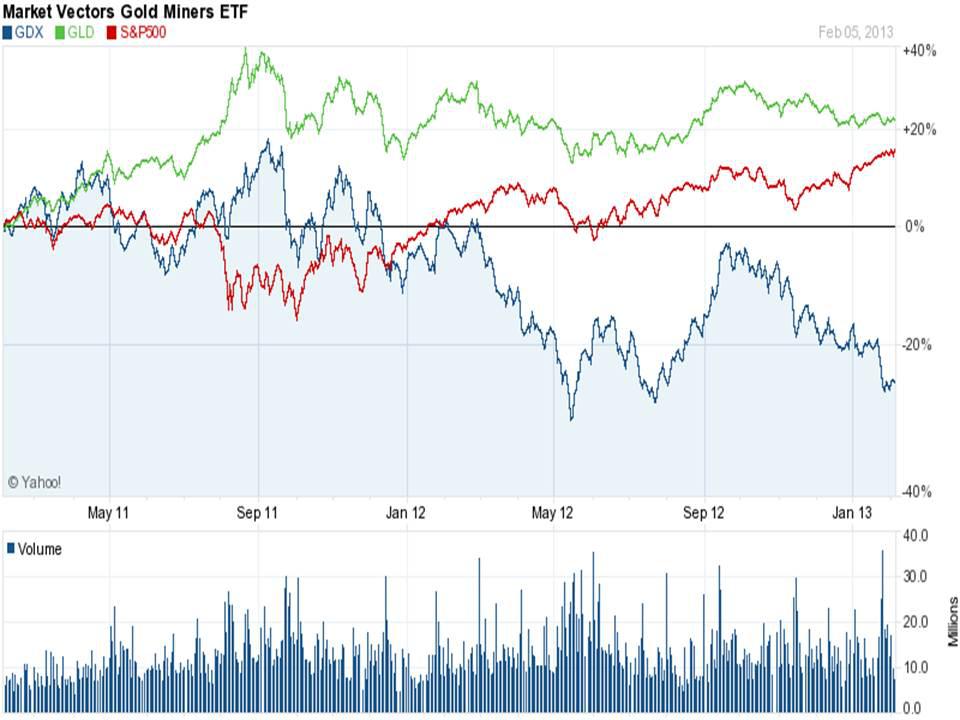

Gold mining stocks have been one of the worst performing sectors over the last two years. They have deeply lagged behind the overall market and the price of gold (See Chart). Miners have been plagued by cost overruns, strikes and increasingly meddlesome governments. However, as my late father was prone to say, "Everything reverts to the mean". I noticed in the last 24 hours that two cheap miners reported solid production guidance. Both are worth consideration by value and growth investors.

(click to enlarge)

New Gold (NGD) is a gold mining company with around a $5B market capitalization. It primarily explores for and mines gold, silver, and copper. The company's operating properties include the Mesquite gold mine in the United States; the Cerro San Pedro gold-silver mine in Mexico; and the Peak gold-copper mine in Australia.

4 reasons NGD has upside from $10 a share:

Golden Star Resources (GSS) owns and operates the Bogoso/Prestea gold mining and processing operations that cover approximately 40 kilometers of strike along the southwest-trending Ashanti gold district in western Ghana, and the Wassa open-pit gold mine and carbon-in-leach processing plant located to the east of Bogoso/Prestea in southwest Ghana.

4 reasons GSS is solid speculative growth play at just $1.60 a share: