Beleaguered uranium investors are finally getting some good news...

As regular readers know, the uranium price collapsed in 2011. It had seen an incredible boom... And then Japan's Fukushima Daiichi nuclear power plant failed after being struck by a massive earthquake and tsunami. Japan, the world's third-largest producer of nuclear power, shut down its fleet of power plants.

The shutdown clobbered the uranium market. First, there was a lack of demand for new uranium fuel. And then the power plants, shut down indefinitely by the Japanese government, sold their stockpiled uranium fuel into the market.

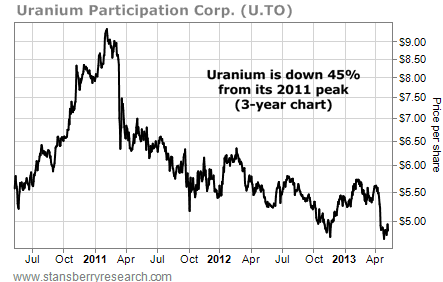

The chart below shows the price action in Uranium Participation Corp. This fund follows the spot price of uranium. The combination of lost demand and extra supply sent the spot price of uranium down 45% from its peak in 2011 to the bottom last month.

But it's possible we've seen the final bottom here.

Japanese engineering firm Mitsubishi Heavy Industries and French nuclear power company Areva SA just announced an agreement to build a new nuclear power plant in Turkey. The new reactor will be Turkey's second. It will take 10 years to build.

According to Bloomberg, the $22 billion project is the first order for a new reactor from a Japanese company since the Fukushima Daiichi disaster.

Also, the first of Japan's 48 idled nuclear power plants could come online in July, with two more in November and another two in December.

This is a major step toward a full-blown resumption of power production from Japan's nuclear power sector. And the new demand should be a significant tailwind to uranium prices through early 2014.

There are a slew of interesting junior uranium explorers out there, sitting at multiyear lows. But it's safer to wait for confirmation of this uptrend before you buy.

The bad news for some of North America's biggest energy producers is getting worse...

Back in early March, we pointed out that

Canada's "tar sand" producers were in trouble. The tar sands are full of thick asphalt-like bitumen. It's expensive to mine. And the companies that operate here must upgrade the bitumen before conventional refiners can work with it.

When oil prices are low, that makes life hard for the big names in this space, including Suncor and Canadian Oil Sands. And the price for Western Canada Select – the benchmark price for tar-sand production – is under major pressure.

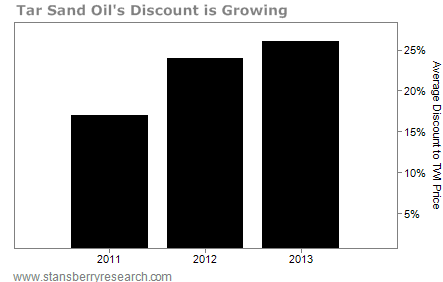

Because tar sand crude is lower-quality crude, it always sells at a discount to West Texas Intermediate, the benchmark U.S. price. That discount is getting bigger.

Take a look at the chart below... The average discount for Western Canada Select is up from 18% in 2011 to 26% so far in 2013.

I expect this trend to continue. As I said in March, we have a

glut of oil in North America today. We're producing an enormous amount of high-quality "sweet" crude. That makes the thick, low-value stuff from the tar sands even harder to sell.

This is a serious problem for Canadian tar-sand producers. Keep clear.

– Matt Badiali