Canada is not immune

posted on

Jan 23, 2012 12:29PM

Golden Minerals is a junior silver producer with a strong growth profile, listed on both the NYSE Amex and TSX.

[Editor's Note: The following is from Chris Horlacher, TDV's Toronto, Canada Correspondent]

One typically doesn’t look to government bureaucracies for hard-nosed, objective discussions on the economy. Far too often official reports are skewed to paint a much rosier picture than what is unfolding in reality. Case in point, the repeated denials from Ben Bernanke and the Federal Reserve, Fannie Mae and various oversight committees circa 2006 that the US housing market was anything but an excellent place to invest your money.

So, imagine my surprise when the December 2011 Financial System Review, published quarterly by the Bank of Canada (BoC), landed in my inbox and I discovered that it contained a very sobering look at Canada’s economy and the many systemic risks we are facing! It’s not surprising that this report was not picked up by the main stream news, because if they did the popular opinion of Canada’s invincible, recession-proof economy, may begin to crumble.

The report identifies five key areas of economic risk faced by Canada in particular, which I will summarize here. We begin with a brief analysis of global macrofinancial conditions and are immediately told that the Bank’s economic outlook in all areas has been revised downwards significantly over the past six months. Europe is judged to be in a recession and recovery prospects in the US look bleak. The report points out that, amazingly, Canadian bank stocks are still trading at 70% above their book value, whereas US, UK and Euro bank stocks are well below this level. The Bank states that this is due to investors placing higher confidence in Canada’s banking system, however if you’ve read my reports on the Canadian housing market (and look at the facts presented in this report) you might also come to the conclusion that much of the confidence is unfounded and could rapidly deteriorate as well.

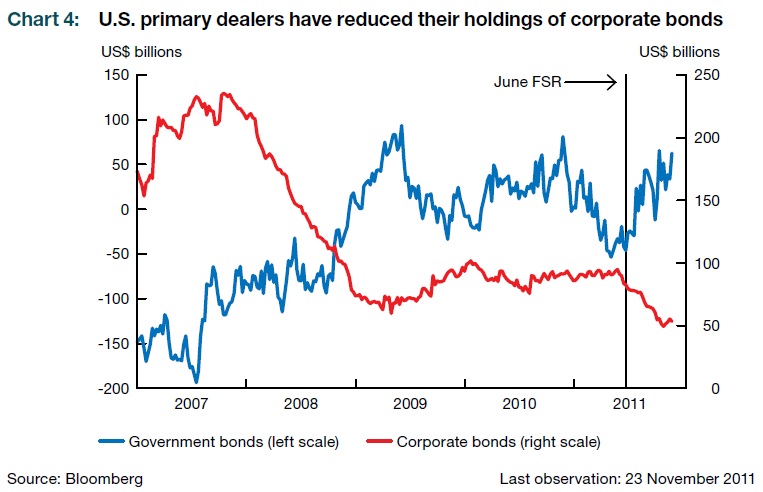

The report also confirms the statement made by many investment experts, such as Peter Schiff and here at TDV, that capital flight into government debt is crowding out private investment. This is part of what is prolonging the depression. Instead of financing economic recovery through investment in new ventures, projects and economic reorganization, primary dealers are instead simply financing the growth of government. This only further dampens the private economy and forms the vicious cycle that is sure to keep the economy in a recession.

As previously mentioned, the BoC identified five major areas of risk facing the global economy, which are as follows:

Global Sovereign Debt

It’s somewhat telling that the BoC decided to list this first, as it illustrates just what a massive problem this is becoming. Tens of trillions have been invested in the debt of governments who are now facing massive budgetary and fiscal crises. An “adverse spiral” has been rated the principal threat to domestic financial stability and that this risk has already partly materialized. Incredibly, the BoC even considers the eventuality of the US dollar losing its reserve currency status:

“Until now, debt-service burdens in both [the USA and Japan] have been held down by favourable borrowing conditions – stemming in part from structural factors such as the high level of liquidity in the market for US Treasuries, the role of the US dollar as the international reserve currency and high domestic savings in Japan. There remains, however, a small but significant risk that this advantage could be lost if investor confidence suffers from repeated failure to undertake the needed fiscal consolidation.”

Unsurprisingly, the BoC considers the numerous bailout and liquidity measures undertaken by central banks and the IMF to be “steps in the right direction” even though they specifically note that any relief that these measures provided was temporary at best and that the situation in Europe continues to deteriorate, with yields on sovereign debt moving sharply higher in a number of Eurozone members.

The chapter concludes that the debt crisis “can be resolved if policy-makers address the situation in a forceful manner… based on credible fiscal arrangements and enhanced governance.” In other words, even more government involvement in the financial system. This has already proven to be useless, as the BoC admitted in an earlier segment of this chapter so one has to ask why they believe that more of the same is necessary.

Economic Downturn in Advanced Economies

In the next risk, the BoC notes what everyone should now be aware of; global economic activity is slowing down markedly. Household and bank deleveraging is dragging the world economy deeper into recession. Further downturns in advanced economies would have a substantial impact on Canadian businesses, households and financial institutions transmitted through bank losses and deteriorating credit quality. The BoC notes that while some banks have increased their capital buffers other banks still have razor-thin cushions and high exposures to underperforming assets. The obvious conclusion we should reach from this is that there continues to be massive, systemic risks in the financial system that could send waves of destruction throughout the global economy.

There are also concerns over asset quality for the global banking sector. The report notes that the US real estate market is vulnerable to further deterioration and that stagnant wage growth is impairing the ability of borrowers to service their mortgage debt. A massive overhang in the supply of housing also persists. Banks have foreclosed on a large number of properties and are unable to liquidate them at what the BoC calls “reasonable prices”. Unbeknownst to the BoC, a reasonable price would be one where buyers would be willing to buy. The fact that banks possess this huge stock of houses actually indicates that they’re asking unreasonable prices for them. Non-performing loans in the UK and Eurozone are at nearly 7% of total loans and climbing. In the US these loans now represent about 2.3%, down from a high of about 3.5% in 2009, and in Canada it is at about 1% of total loans and showing a small decline since 2010. Despite Canada’s low levels, the Bank concludes that:

“If economic activity declines significantly, a growing number of Canadian households and businesses would experience financial difficulties, which would translate into an increase in loan losses at financial institutions. If banks curtail credit, this would trigger an adverse feedback loop through which declines in economic activity and stress in the financial system would reinforce each other.”

This statement mirrors what I had predicted in my article “The Canadian Moral Hazard Corporation”, where an economic downturn would impair the quality of mortgages, causing a string of defaults to ripple through the banking system, in turn necessitating massive bailouts and debt monetization by the Bank.

Global Imbalances

The report also notes that current account imbalances (trade surpluses and deficits) remain an important source of risk. These imbalances, and the lack of exchange rate flexibility that allows them to persist, have created a global economic configuration marked by unsustainable debt accumulation in some advanced economies that is counterbalanced by asset accumulation in some emerging-market economies. While the report doesn’t mention any specific names, it could not be clearer that they’re referring to China’s accumulation of trillions of US dollars and US treasuries. The Chinese renmimbi is being closely managed by the Central Bank of China at an exchange rate of 6.4 to the US dollar and has held it down for over a decade. In the 1980’s the renminbi was intentionally devalued against the dollar as China pursued their plan of creating an export-driven economy. This manipulation has ensured that the US dollar remained overvalued against the renminbi and the consequence of this has been US dollars being used to purchase Chinese goods at tremendous rates. While devaluing a nation’s currency against those of their trading partners has long been held as a way to stimulate exports, one has to wonder if forcing exporters to accept less than fair value for their products is really conducive to creating a healthy economy.

The Bank is concerned, and rightly so, that this imbalance could unwind in a rapid and disorderly way. This has been referred to as a “decoupling” scenario by many investment industry experts. Large and abrupt movements in the value of the renminbi would impose significant losses (and gains) on financial institutions worldwide. The Bank also stated that the reserve accumulation in surplus countries could distort the financial system of those countries, resulting in asset price bubbles. This is becoming apparent in China, as they have constructed entire cities that cannot be occupied at current prices. It appears that China, who has experienced year over year GDP growth in excess of 8% for many years, may be in for a correction very soon.

Low Interest Rate Environment in Major Advanced Economies

The report further notes that interest rates are at or near their all-time historic lows and that this is likely to persist. According to the BoC, “accommodative monetary policy is necessary to support the global economic recovery” and this is consistent with what we’ve heard coming out of the Federal Reserve. This simply isn’t the case though. The crisis was brought about by central banks setting interest rates lower than the market would bear so further suppression is unlikely to induce the necessary repairs. Here the BoC really displays that despite knowledge of the facts, it lacks the theory necessary to properly interpret them and they wind up making the wrong diagnosis and prescribe remedies sure to only further the harm done to the economy.

The Bank notes that low interest rates put pressures on institutional investors like pension and insurance funds. Low rates increase the actuarial value of their liabilities while simultaneously reducing the return on their assets. This can lead to excessive risk-taking by these institutions as they attempt to balance their assets and liabilities.

What the Bank doesn’t mention though, is the inflation risk brought about by low interest rates. Low rates stimulate increased borrowing, which in turn expands the money supply. The reason why banks became so highly leveraged to begin with was the endless supply of cheap credit from central banks. It’s unfortunate that this risk isn’t explored in the report because it represents a much greater, and more fundamental, issue facing the global economy. Realizing this also plants the seeds for recovery as it becomes obvious that what is needed is higher interest rates, which would stimulate retrenchment by banks and the liquidation of bad assets. Continuously low rates only prevent these imbalances from normalizing.

Unfortunately, a low interest rate environment is taken as a foregone conclusion and the BoC proposes measures that would further impair the ability of institutional investors to deal with the risks they face on an individual basis. Prescribed portfolios and the herding of capital into more risky derivative products are suggested as a means of dealing with the risks produced by low interest rates.

Canadian Household Finances

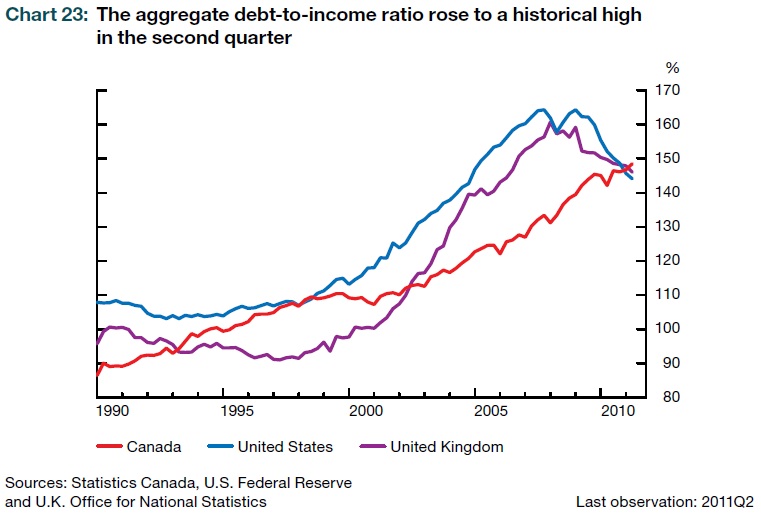

The final risk begins by stating something that I have been saying myself for some time now, that “The rising indebtedness of Canadian households in recent years has increased the possibility that a significant proportion of households would be unable to make debt payments in the event of an adverse economic shock.” With all the other risks identified in the report, I would say that such a shock is now inevitable, the only question being at what time and from what direction it will arrive. The aggregate debt-to-income ratio is at a historic high and as of Q2 2011, now exceeds that of the USA and the UK.

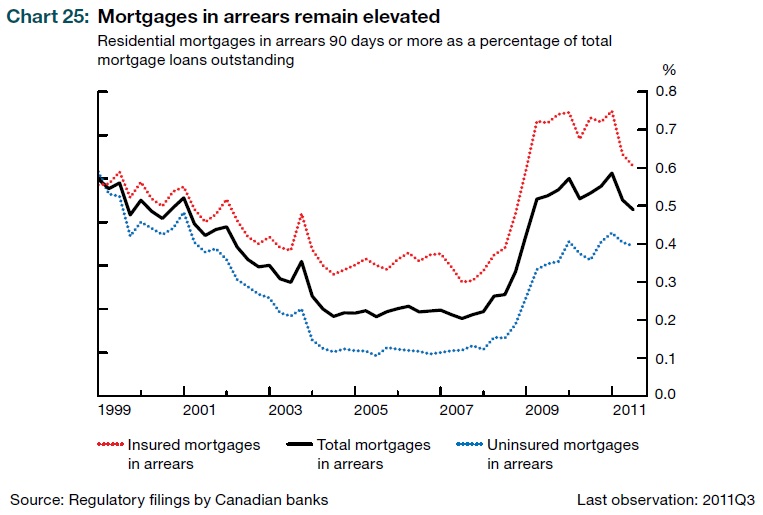

This is a good measure of leverage that illustrates the ability of borrowers to service their debts. Canadians are now in an even worse position to be able to do this than two economies that have been ravaged the most by recent economic events. The BoC expects that this ratio is going to continue to rise, further endangering the financial condition of Canadians and making them even more susceptible to financial shocks. While aggregate credit-to-GDP ratios have been declining, they still remain at or above levels seen during previous recessions in 1990 and 1981. Furthermore, the amount of mortgages in arrears is also elevated.

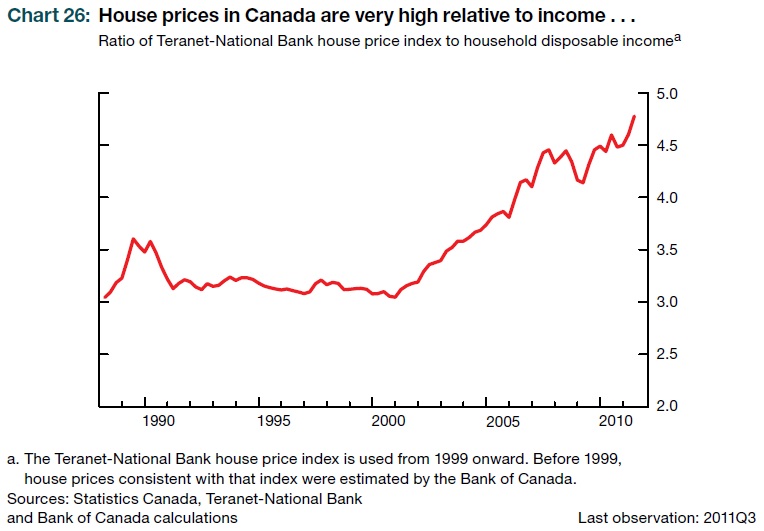

The BoC points out, as I have in the past that Canadians are especially vulnerable to two inter-related events; a significant decline in house prices and a sharp deterioration in labor market conditions. Since most mortgages are insured, a moderate fall in house prices could initiate a negative feedback loop with the real economy, destroying household net worth, access to credit and other factors. Never, however, does the BoC consider how this would affect the finances of the Canadian Mortgage Housing Corporation, but as I predict, it would be severe as well. Housing prices are far higher, relative to incomes, than they were during the last housing bubble and so a decline at this point appears inevitable.

The baseline price-to-income ratio of housing appears to be around 3.0 and we are currently at about 4.8. Based on these facts we are looking at a potential overall decline of 35% or more in average real housing prices. The Bank performed a stress test based on various assumptions on income growth, debt accumulation, unemployment rates and interest rates. They project that a 3-percentage point rise in the rate of unemployment, coupled with a six-week increase in the average duration of unemployment would double the proportion of loans in arrears from 0.65% to 1.3%. Based on my own analysis of the CMHC, if all those loans in arrears went in to default (which is the next step), it would nearly wipe out all of the capital of the CMHC. Also remember that bureaucracies are notorious for under-estimating adverse economic consequences and so the events simulated by the BoC could even be considered a best-case scenario. It is quite likely that the shock will be much, much worse.

Conclusions

The report is replete with facts and observations suggesting that Canada is in a dire economic situation that could rapidly deteriorate, with consequences being felt by every Canadian. Unfortunately it appears that they have failed to see the real destabilizing force behind all of the imbalances present in our system. It is the low interest rate environment, produced by the BoC itself that has led us to the precipice. While it is clear that those at the Bank have access to all of the necessary facts, they lack the understanding needed to prescribe real solutions to the problems and as a consequence they are likely to persist for much longer than they need to.

Furthermore, the report confirms my fear that in the face of a real downturn the BoC will not be able to resist the urge to intervene and will only wind up compounding the damage that has already been done. The BoC continues to view itself as a benevolent planner rather than acknowledge its own role as source of risk. They will continue to interpret events in their own favor and use them to justify further intervention in the market, which is just throwing gasoline on the fire.

Link to the article; http://www.dollarvigilante.com/blog/2012/1/19/the-economic-outlook-for-canada-is-dire-says-the-bank-of-can.html