Meanwhile, Greenwich Alternative Investments, a hedge fund database and research firm reported on Thursday:

Hedge Funds Dramatically Outperform Equity Markets Despite Losses…Year-to-date, the GGHFI and the GI2 shed -8.85% and -8.82%, respectively, while the S&P 500 Total Return, MSCI World Equity, and FTSE 100 Indices have lost -19.29%, -25.59%, and -24.07%, correspondingly. 24% of constituent funds in the GGHFI ended the month with gains.

“Rash Decisions”

Bloomberg reported that some of the long-only industry’s biggest funds, such as Fidelity’s Magellan, were down well over 40% YTD. Arguing (appropriately) that investors should look at the long run - a point often ridiculed when made by hedge funds - a Fidelity official told Bloomberg:

…the market’s higher volatility may cause some long-term investors overwrought with fear to make rash decisions that alter a well diversified portfolio.

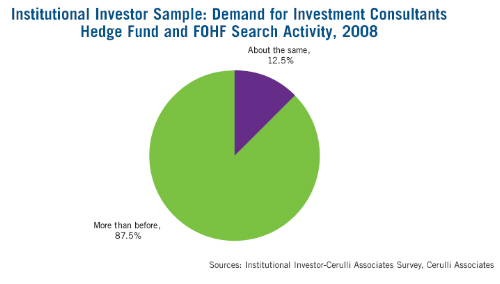

Long-Only Demand “Stagnant”

The challenges faced by long-only investment industry haven’t been confined to just the retail segment. Cerulli, a research firm specializing in the institutional asset management business, released new findings last from a survey of institutional investment consultants. The headline of the firm’s press release says it all:

Investment Consultants Focus Search Activity in Alternative Asset Classes-Hedge Funds and Funds of Hedge Funds-While Demand for Traditional Long-only Products is Stagnant: Many long-only products have difficulty in generating consistent alpha, and institutions would rather index core asset classes using ETFs, index funds, or derivatives.

How much a “focus” will consultants need to have in order to satisfy demand? This much…

“Consultants Are Struggling”

Almost 9 out of every 10 institutional investors surveyed by Cerulli said their hedge fund search activity would be “more than before”. So how are consultants responding? Cautiously, that’s how. Perhaps too cautiously, according to Cerulli:

…While most consultants acknowledge institutional demand for alternatives, many are not staffed in a manner to satiate plan sponsor demand. Small consultants were especially forthcoming about their lack of alternatives expertise, with only 31% reporting strong hedge fund due diligence capability, 31% reporting strong private equity teams, and only 25% reporting strong derivatives expertise. Consultants are struggling to build adequate alternatives practices, as analysts with alternatives experience are lured by large salaries and bonus potential at hedge funds and funds of hedge funds.

Witch Hunt

Meanwhile, a US Congressional committee exploring “the causes and effects of the crisis on Wall Street” wants to have a chat with hedge fund manager John Paulson this week. The committee’s invitation (available here) requested that Paulson explain to it…

- “…the level of risk associated with your hedge fund or other hedge funds”

- “…the likelihood that your hedge fund or other hedge funds could suffer significant losses”

- “…the systemic risk or impact on the economy that could follow from significant losses by or collapse of your hedge fund or other hedge funds.”

Other lucky invitees include hedge fund George Soros, Jim Simons, and Ken Griffin. Oddly, all of these guys are also among the highest paid managers in the world. For some reason, the committee seems to have passed over many lesser-paid experts. Perhaps it has something to do with another issue the committee wants them to address (on national television)…

…provide the following documents…The compensation paid to you and the next two highest paid officers in your firm and the formula used to calculate this compensation. Please include with your response a table showing the compensation paid to each individual, broken out by year and type of compensation (e.g., overhead fee, carried interest, bonus, etc.).

No word yet on whether the same questions will be posed to managers of hedge funds’ more volatile cousins, the long-only funds

We have an interesting situation at Noront Resources (TSX:NOT) where Rosseau are attempting to ursurp the status quo armed with personnnel from the Aurelian debacle.

The proxy can but be called immature and certainly the ex-directors of Aurelian; four in number who filled their pockets to the detriment of the retail shareholders; would be out of their depth when coming up against real miners.

Let me quote a critique I found on the Noront board at agoracom.com by hoov, but before doing so, let me ask you one question, 'how desperate are Rosseau?'

Subject: Rosseau Circular....a tissue of lies, half-truths, and deception. What a coincidence! After months of recurrent attacks by bashers, and in the midst of the most recent one, the short-selling market manipulating monster finally reveals itself to us. And this circular is more of the same......lies, half-truths, rumours, and deception, intended to instill shareholder fear, and reduce confidence in management of Noront. It is far from being a sober, dispassionate analysis. I've read the Rosseau Circular through a number of times now, and I'd like to isolate and analyze the points used to criticize Noront management.1. First, they allege that Noront has squandered opportunities since August 2007, when Eagle 1 took our SP to lofty heights (7.42), and thereafter imply that management is solely responsible for the current SP.I should think, first off, that if those "squandered opportunities" exist, that they should be easily defined and described. And yet, no specific examples are presented. Not one. Instead, I can think of some fine "opportunities&qu... that Noront has created in the meantime, called Eagle 2, Blackbirds 1 & 2, At-12. And, the resource at Eagle 1 has been defined by 43-101. I think that's pretty good for one year's progress.Secondly, I can think of external forces at play which have influenced our SP. We've talked about them incessantly over many months. Things like something called a credit crisis, worldwide recession, market fear/capitulation, market manipulation (especially (naked) short selling......what these Rosseau boys do). I would be hard-pressed to find any cause that can attribute any of this to Noront management.....and Rosseau doesn't even try.2. (a) Noront *recently* wasted 15 million on Windfall.<cough> Excuse me?Where on Earth did that bloated figure come from? Given the time frame alluded to in the prior allegation (i.e. after August 2007), the idea of recent expenditures of anything more than a fraction of that amount is absurd. Noront raised 15 million in a private placement about two years ago, to fund the Windfall ramp and bulk sampling program. By not acknowledging this, Rosseau intentionally creates a false impression.Windfall, and the commitment to drive a ramp towards the gold vein deposit, entirely precedes the ROF discoveries, and historic spending (that's where 15 mil figure comes from) should not be confounded with current budgets. The decision to drive a ramp towards the gold was entirely prudent, given then current estimates that surface drilling to define the deposits would cost a similar amount, would not define grade with certainty (we're talking vein gold, here), and would likely end up requiring a ramp anyway.They further allege that funds raised earlier this year have been diverted from the ROF to Windfall, via "unduly promoting" the McFauld's discoveries, and then diverting "substantial"... funds to Windfall. That is an outright falsehood. Noront has been absolutely forthright about its cash budgets with respect to all its properties. Funds were fully raised and committed to Windfall prior to February 2008, when the PP for McFauld's exploration was done. Furthermore, investments in Noront are not specific to any one property. To confound investor expectation with management practise is utterly absurd.And who said the investment at Windfall was *wasted*????? I saw some very nice photographs of museum-quality gold ore coming out of that ramp. And from a location not previously known to host gold. It is, at a very minimum, premature to call the investment wasted. Rosseau elsewhere criticizes Noront for failing to proceed from an exploration company towards being a mining company, and yet they would negate and dismiss clear efforts to do so at Windfall? Talk about sophistry.2. (b) ....and spent $1 mill on other properties, diverting cash, human resources and focus.In all but a couple of cases, once again these properties have been in Noront's portfolio for a long time. JV partners are operators at many of them, so they require little investment or oversight. Others have had so little attention paid to them that nothing whatsoever has been spent on them in recent times. In fact, recent MD & A reports have made clear that management is not diverting money and resources away from the ROF. Instead, look at how many new staff had been added! Since 2007, office staff has more than doubled, and expert management has been added a number of times. Whatever management these other properties demanded, those efforts are surely much *diluted* now, compared to previous years.And just from a more exploration-based philosophical perspective, how is it that you can criticize a mineral exploration company for thoroughly investigating any opportunities which have come its way? What else is it that you would expect them to do? Walk away?Noront management has clearly expressed its intention of separating the funding and management of the ROF from its other assets. All this would do, IMHO, is to make formal what is surely happening in practise already.3. (a) Alleging that the 11 Ring of Fire JV projects are drains and distractions on administrative and operating resources.Poppycock! Those are claims Noront chose for immediate mineral investigation. Of all the thousands of claim blocks under Noront's control, they entered into agreements to push specific clusters of blocks forward, and obtained other people's investments of resources to pay for it all. These are Noront's choices of targets. (I'm certain they didn't throw darts at a map!) They would have been chosen for drilling anyway. But someone else is paying for it. There is no change in administration, but there is a *reduction* in operational expenditure.In addition, these agreements have contractural time-lines. They force directed investment (read drilling) in a timely way. If the drills don't turn, or funding doesn't come, the JV collapses, and no dilution of interest occurs. With Noront's immense land holdings, getting those drills turning is the priority. When they say "take(ing) valuable manpower and scarce drills away from Noront’s 100%-owned high priority prospects".....wh... is the allegation really suggesting? That somehow Rosseau already knows which properties to drill? That they know the rest of the ROF is not worth exploring? I see no evidence that Noront has misused its drills or manpower. Think Blackbird.Elsewhere, Rosseau reveals their *real* concern about the JVs.....3. (b) The re-structuring of ownership interests makes Noront a less attractive target for a major.Now we're looking at strategy. The quick flip, vs. long-term investment via e.g. buy-in, other JVs, or self-development.It is my opinion, based on what Rosseau presents here, and from its historical investments, that what they want to do is break up Noront, and flip it as quickly as they can. In fact, I suspect Rosseau is acting as a proxy for a major. When they say they want to improve shareholder value, I believe they have only their own interests at heart. In and out as quickly as they can, so they can go on to short and raid some other victim.In contrast, Noront has always taken the long view. From the moment the Eagle 1 resource was defined, they spoke of mining it and selling the ore. In fact, they had their hands slapped by the TSX for suggesting feasibility issues had been addressed according to OSC regulations. When chromite was hit, again, talk was immediately about the value of the ore on the market, not in situ. No talk about getting maybe 10% for in situ, but instead, full market value based on mining, concentrating, and shipping ore.For this issue, it comes down to personal decisions, but since this is my analysis, I'm going to supply my opinion. IMHO, far greater value accrues to Noront from taking the long view, mining and shipping ore, or even from nothing more than NSRs, than from breaking up the company and flipping its still poorly defined assets. Noront is well on the way to turning blue sky into ore in the ground, and with each increment, the long term value increases. With a sell-out, no further increments are possible.3. (c) squandering of "leadership position" via JVs, rather than accretion and consolidation.Give me a break. Noront continues to stake land, both on its own, and as a part of a staking syndicate. Noront has expressly stated that it desires to control 80% of the ROF.One does not accomplish such a task overnight. IMHO, the opportunities to take over weaker stakeholders are only just now presenting themselves. It's no secret that funding for juniors is going to be a critical issue with respect to their viability. We'll just have to see how things shake out.But, more directly to the point raised, just how is new management going to accomplish this? Massive dilution of existing shareholder value? You can be sure these vultures would profit more from that than we would. Diversion of scarce resources from drilling? No, wait, that's a criticism of existing management.Bottom line is Rosseau is suggesting something Noront has already said they'd do. Again, it comes down to a fast flip vs. long-term accretion of value.4. (a) replacing Richard.I don't know.....does he need replacing? He's certainly attracted some amazing talent to the company. That's a testament to the man. He's got experts with respect to take-overs/mergers, TSX listings, finance, geology, and a host of top-notch consultants.Rosseau doesn't even suggest a man to replace him. They apparently have no faith in their ex-Aurelian president.4. (b) listing on TSXWe've been talking about that for a long time. Noront cannot talk about it. It's forbidden. Rosseau isn't, and they're taking advantage of that.Lately, people have noted a subtle change in content from Noront about this issue. Whereas before they would say they're not currently working on it, now they restrict themselves to "no comment".....as required of them, if they are in fact proceeding with such a move.It takes time, and we'll know about it when it happens. IMHO, it's already not far off. Rosseau offers nothing here, either.4. (c) spin-off of non-core assetsManagement has expressly stated a number of times that this will happen. We've also discussed how complicated it might be, with Windfall still not subject to formal resource estimates, and implications with respect to possible TSX listing. These two issues may be intertwined in regulatory red-tape.Richard's a lawyer, and he's got people with direct experience in getting this done. It takes time, and he can't talk about it until it's all sorted out. Rosseau is again just blowing smoke. They'd be in the same position as existing management finds themselves. When Rosseau says they see no evidence of progress, that's pure sophistry once again. These are all or nothing propositions. There can be no progress reports.5. Exaggeration and undue promotion by Richard.To support this, Rosseau provides only a second-hand anecdotal report from the Financial Post, that the geology was similar to Voisey's Bay, and that "it could even be bigger". Without any context, we cannot even know Richard's true intent with the statement. Moreover, Noront's grades are higher than Voisey's, and the geology strongly suggests that there is more nickel out there. That it hasn't yet been found doesn't disprove the fact that Richard may be right.....it could be bigger.I recall suggestions that Noront might have 15-30 million tonnes of chromite. Funny, now I'm hearing there might be 100 million, with deposits open on strike. Today, on the FWR hub, I hear 150 million.Rumours always attach to exploration plays. If you want proven reserves, buy some Billiton. But don't criticize a man for being excited about his exploration plays.More smoke, IMHO.Frankly, I haven't been persuaded that any one argument they've raised has validity, let alone the lot of them. However, let's move on to consider the nominees for board positions.Let's see, four of them come from Aurelian. Hmmmm, seems they're out of work right now, after selling out their company for a 60% premium over a massively depressed SP. I guess I know what they're good at.Another guy is a director from Temex, which seems to be involved in a large number of JVs in the ROF. Some of them with Noront. Now that would be a change, wouldn't it?And a couple of others who are willing to resign if more qualified people can be found.Honestly, not one of these nominees holds a candle to the men we've already got. They're openly seeking a couple of better qualified directors. And they don't have a president in mind, to give life to their "vision". And this is somehow an improvement?Bottom line, the choice seems to be between breaking up Noront and flipping the ROF claims, or taking the longer road to higher values. Rosseau claims to be willing to do things that existing management has already dedicated themselves to accomplishing, so what's new there? Apart from these "commitments"... they offer nothing but platitudes.What's the damn rush? Rosseau is greedy. That's my analysis.