Don't Expect Palladium to run out of Gas

posted on

Nov 09, 2017 07:50AM

NI 43-101 Update (September 2012): 11.1 Mt @ 1.68% Ni, 0.87% Cu, 0.89 gpt Pt and 3.09 gpt Pd and 0.18 gpt Au (Proven & Probable Reserves) / 8.9 Mt @ 1.10% Ni, 1.14% Cu, 1.16 gpt Pt and 3.49 gpt Pd and 0.30 gpt Au (Inferred Resource)

https://oilprice.com/Metals/Commodities/Dont-Expect-Palladium-Prices-to-Plunge.html

By Viktor Katona - Nov 08, 2017, 10:33 AM CST

Over the past month, there has been a deluge of news heralding a new era of palladium, which has soared above the $1000 per ounce mark for the first time in the past 16 years. Moreover, palladium also overtook platinum and is still being traded at a premium to it. The overwhelming majority (78 percent) of the world’s palladium is used in gasoline-fueled cars’ catalytic converters, with minor volumes going into electronic resistor production and dental construction. A plethora of factors has been conducive to the latest palladium surge – rising gasoline sales in Europe, robust car sales in the predominantly gasoline market of China, hurricane-damaged households buying new cars in the United States, all this against the background of tight palladium production supplies. But will the current price level stay or is a massive bust lurking behind the corner? Evidence suggests the former.

The main reason behind palladium’s overtaking platinum lies within the development course the global automotive industry has taken. Whilst palladium is used primarily in gasoline cars, palladium’s sister metal platinum is generally applied in diesel cars – following Volkswagen’s diesel emission scandal and shattered confidence in Diesel cars (most notably in Europe where the market share of once-prevailing diesel cars has fallen below 45 percent) the two metals have been moving into opposite directions. Moreover, hybrids combine a gasoline engine with an electric motor, further boosting the utilization of palladium. Palladium’s usage in automotive catalytic converters rose by more than 55 percent in the last 10 years, whilst its more traditional method of use, as a jewelry item, has been in a state of freefall, decreasing to a mere quarter of its 2006 demand.

Related: Can Oil Prices Hit $65 This Week?

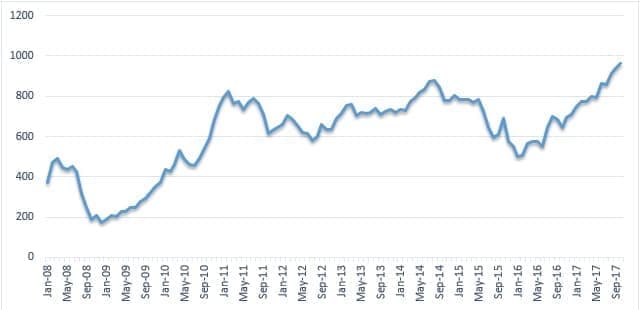

Graph 1. Annual palladium supply vs. median annual palladium price.

(Click to enlarge)

Source: Thomson Reuters, Johnson Matthey.

The average annual palladium price median (Graph 1) does not really convey the intensity with which palladium prices reacted to post-2008 developments. In February-March 2008, for instance, palladium prices hovered around $500 per ounce, by the end of the year, however, it came crashing down to $170-180 per ounce levels. Palladium prices witnessed sharp falls in almost regular 7-year intervals between 2000 and 2015, under various circumstances. The 2001 price plunge was the direct result of the hype the Russian palladium stock sale generated in the 1990s, and brought about a period of several years during which the prices oscillated in the $200-350 per ounce interval. The promising 2008 price surge was cut short by the ensuing financial crisis, as a consequence it was only in 2010 when palladium found itself above the $600 per ounce mark.

Another decrease took place in 2015 (see Graph 2) at a time when market participants feared that a Chinese stock market crash might pull with itself down the consumption sector, too. As all this took place against the background of Europe struggling to resolve the Greek debt crisis, needless to say fears about the whole EU eventually crumbling down abounded, palladium’s slump was inevitable. Today’s outlook, however, is significantly brighter – with supply having difficulties meeting demand, demand growth on virtually all continents (only Japan is expected to need less, now accounting for 12 percent of the market) against the background of emission rules becoming increasingly more stringent, one can safely place their bets on palladium keeping its ground.

Graph 2. Monthly Palladium Spot Prices ($/ounce).

(Click to enlarge)

Source: Thomson Reuters.

Supply lagging behind demand is by no means a new phenomenon in the world of palladium trading. However, historically this gap was bridged by Russia marketing its treasury deposits, the total of which, although strictly labeled ‘top secret’, were reported to amount to 6200 tons by the time the Soviet Union collapsed. In the 1960s, when palladium was five times cheaper than platinum, the Soviet government decided to stock the metal instead of putting it to market, thus creating a cushion for posterity. The cushion was exhausted pretty quickly by the cash-strapped Yeltsin government, for instance, in 1996 Russia exported thrice as much palladium as it produced. After 2000, when palladium peaked at $1125 per ounce and its world sales reached an all-time record of 300 tons, the Russian treasury stock has been driven to almost complete depletion.

Related: Russia Aims To Dominate Middle East Energy

Since 2012, the palladium market is stuck in a situation of supply deficit, which, even with the more robust reutilization of autocatalyst scrap (expected to quadruple as compared to 2000 levels), is still 30-40 tons per year short of balancing even. Therefore, it is quintessential that the two nations currently controlling most of the palladium market, Russia and South Africa, find ways to increase their output. Nornickel is Russia’s only major producer of palladium (97 percent of the nation’s total output) is also the world’s leading producer, with a market share of 40 percent. Contrary to the more platinum-rich South African ores, the palladium-platinum ratio in Russia’s leading production basin around Norilsk stands at 3-4:1. This is, however, counterweighed by South Africa’s massive reserves (its platinum-group reserves, albeit mostly platinum, account for 95 percent of the world’s total), which have not been developed appropriately due to labor unrest, frequent disruptions in electricity supply coupled with high power costs and mounting debts.

As a consequence, in 2018-2019 it will be Russia that will be responsible for most of production increase, largely due to significant efficiency increases in the Talnakh concentrator now that its three-stage modernization programme has finally been completed. Canada might add a few tons annually thanks to promising developments of the Iles des Mines project, however supply will remain at the tail-end of demand for the next few years. Apart from economic circumstances, geopolitical conditions (especially strains in the US-Russia relationship where Nornickel sanctions are often flaunted, but very unlikely to happen) will also alter only slightly, therefore it would be politic to expect palladium prices average at around $1000 per ounce in 2018. Further on, most likely in early 2020s, the market logic might reverse the current trend – as palladium was brought into the gasoline-car catalyst market as a cheaper substitute of platinum, platinum which is now cheaper could be brought back to lower costs. But that is a matter for the future, now palladium rides high.

By Viktor Katona for Oilprice.com