Three Reasons the Nickel ETF Is Soaring (from Jim Sinclair)

posted on

Mar 06, 2010 11:58AM

NI 43-101 Update (September 2012): 11.1 Mt @ 1.68% Ni, 0.87% Cu, 0.89 gpt Pt and 3.09 gpt Pd and 0.18 gpt Au (Proven & Probable Reserves) / 8.9 Mt @ 1.10% Ni, 1.14% Cu, 1.16 gpt Pt and 3.49 gpt Pd and 0.30 gpt Au (Inferred Resource)

Three Reasons the Nickel ETF Is Soaring

Since the most recent global recession began (and the subsequent stimulus measures took effect), many of the relationships between asset classes that have historically guided investment decisions have weakened considerably. The correlation between US equity and bond markets has gone through the roof, an indication of an increasingly liquidity-driven market.

Commodities, which have traditionally been embraced for their low correlation with stocks and bonds, have frequently moved in lockstep with equities, as demand for many resources is now dependent on the health of the global manufacturing industry (see Five Ways To Give Your Portfolio Much Needed Diversification) .

So far in 2010, many metals have moved in response to changing outlooks for demand in emerging markets, which now account for a significant portion of global demand (copper, which is primarily derived from Chilean mines, has obviously been impacted by some unforeseen circumstances).

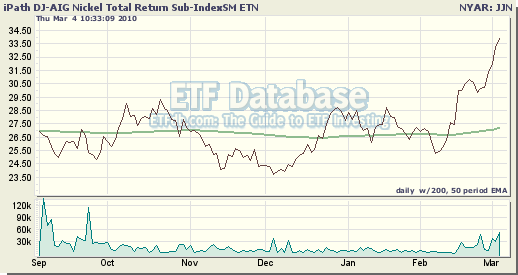

To this point in 2010, one metal has distanced itself from the pack, boosted by increasingly strong demand. Nickel prices have skyrocketed this year, as the iPath Dow Jones-UBS Nickel Subindex ETN (JJN) has gained more than 20% to date in 2010 and is up about 40% since early December. The metal’s impressive run-up has investors wondering just how long the nickel rally can last. A look at the three primary factors driving prices sheds some light on the issue:

3. Looming Nickel Deficit

Last year demand for stainless steel, which accounts for about two-thirds of nickel demand, fell by nearly 5% as a result of the economic downturn as manufacturers looking to reduce swollen inventories. The result was a nickel surplus of 45,000 tons. This year, demand for stainless steel is on the rebound, and analysts anticipate a deficit of 20,000 tons, the result of big increases in orders from stainless steel makers.

2. China’s Insatiable Metal Appetite

China certainly felt the pinch of the recent downturn, but the emerging market’s quick recovery and return to impressive economic growth has resulted in a new-found importance to the global economy. China is the world’s largest user of stainless steel, so the outlook for growth can have a major impact on raw material prices. Last month, investors expressed anxiety over China’s plans for winding down stimulus packages enacted last year. But any concerns have been eased by bullish comments from Beijing and data releases suggesting a bullish outlook for the country’s manufacturing operations.

“Demand from the principal applications for stainless – white goods, process industries, transport and construction have remained strong in China and are recovering well in the rest of Southeast Asia,” writes Stuart Burns. China recently resumed production of stainless steel to full capacity, and is expected to boost output by nearly 20% this year.

1. Reclaiming Lost Ground

Nickel climbed steadily during bull markets in 2006 and 2007, as strong demand for stainless steel pushed prices to new heights. By April 2007, nickel topped $52,000 per ton, prompting the United States Mint to criminalize the melting and export of five cent coins (the value of the coin’s components was nearly nine cents). But the new regulations quickly became moot, as nickel began a rapid decline that foretold the upcoming recession and made the losses endured by many other assets very tolerable. By January 2009, nickel prices had fallen by nearly 80% to less than $11,000 per ton.

So although nickel prices have jumped by more than 100% over the last 14 months (recently trading over $20,000 per ton), the metal remains far below pre-recession levels. This gives some investors confidence that there is still some wind left in the sails of the recent rally.

{kind=link}