Re: Re: Whats New-Reason for oil price collapse

in response to

by

posted on

Dec 06, 2008 07:13AM

Connacher is a growing exploration, development and production company with a focus on producing bitumen and expanding its in-situ oil sands projects located near Fort McMurray, Alberta

Why if oil supply is decreasing and demand is increasing is the price collapsing? What is happening? Is Peak Oil therefore a myth?"

I addressed parts of this question in an October blog post but there's more to dig in to, particularly regarding some common misconceptions about what's happening with supply and demand. I'll take William's question as a framework for addressing some of these issues:

"IF OIL SUPPLY IS DECREASING..."

Strictly speaking, the global oil supply has been decreasing since we started drilling in the mid-1800s. What we really care about is the ever-increasing flow of oil from underground reservoirs to markets because that's what feeds ever-increasing global demand. The oil industry generally talks about 'production' (i.e., extracting oil out of the ground and 'producing' it into a usable barrel), so this part of the question is, more accurately stated, "If global oil production is declining..."

But, production isn't necessarily declining right now. To explain why, we first need to pick apart what we really mean by the word "oil" -- which isn't as clear-cut as most people think. Analysts generally divide oil into two kinds, conventional and unconventional:

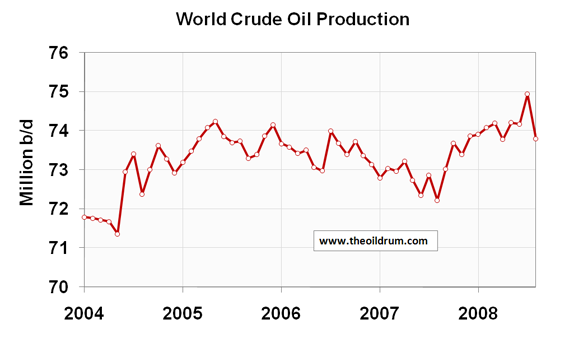

Conventional oil is the stuff we've been getting out of places like Texas and Saudi Arabia for decades, and which made up about 86% of total global oil production last year. Until this past July, when oil prices skyrocketed to all-time highs, "conventional" oil production had been hovering between about 72.3 and 74.2 million barrels per day (mbpd) for about four years.

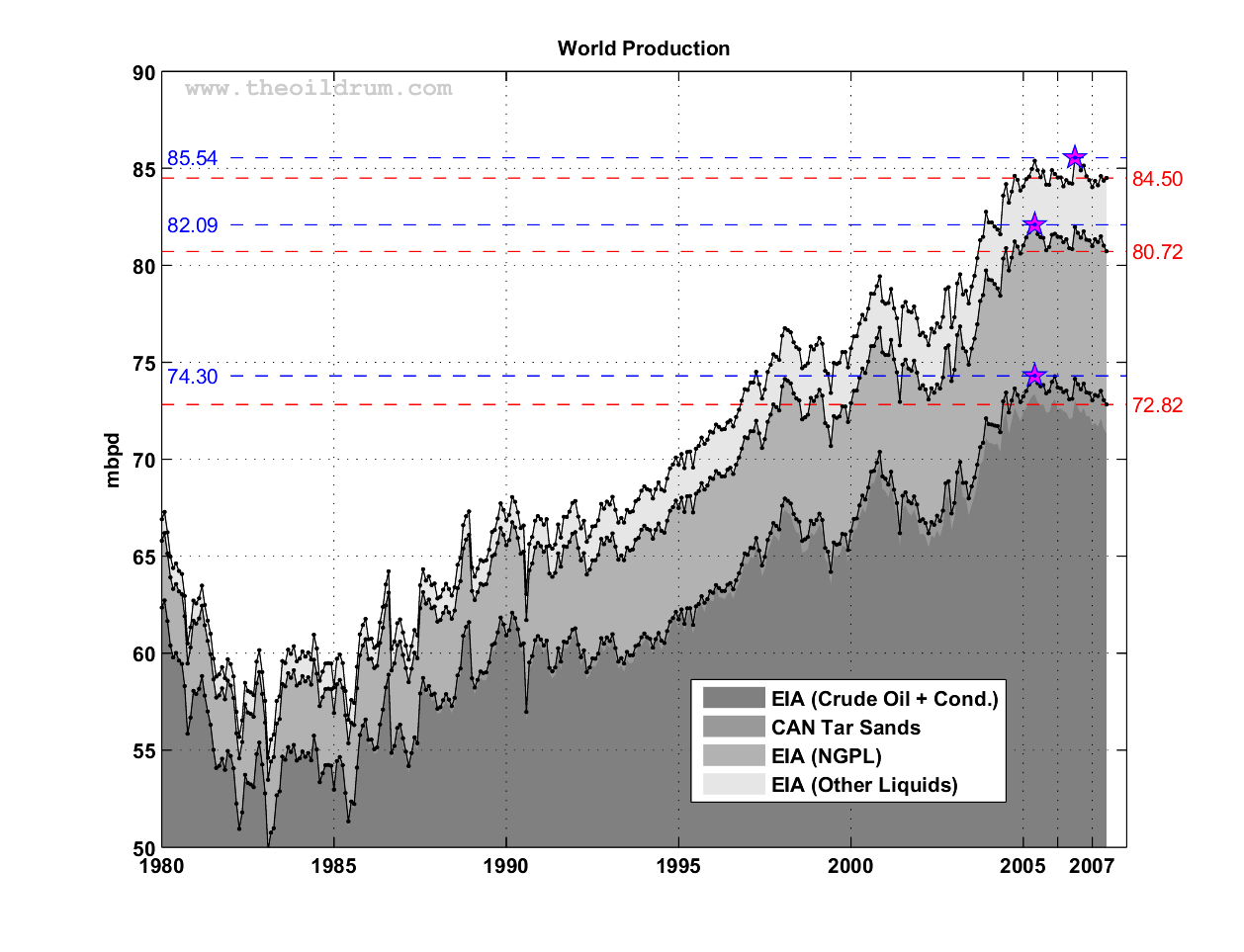

Then there's unconventional oil, which is generally considered to include low-grade resources like tar sands, oil shale, and 'heavy oil', plus even more logistically challenging resources like deepwater oil and polar oil. Some analysts talk about unconventional sources and use this broader umbrella to include natural gas liquids and biofuels.

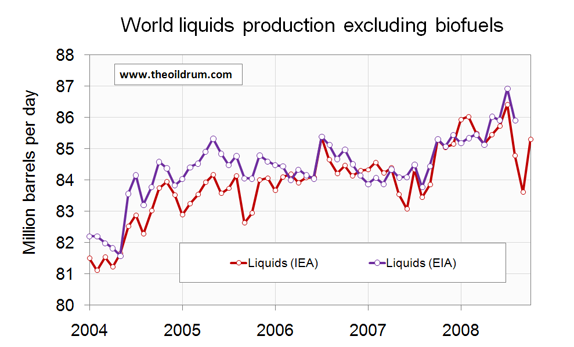

Unlike conventional oil, unconventional sources grew noticeably from 2004 to 2007 -- and together, the total flow of both (sometimes collectively just called 'liquids') grew from about 83 mbpd in mid 2004 to about 86.5 mbpd in mid 2008. That's paltry growth, however, compared to a relatively steady increase of oil production since the end of the first Gulf War in the early 1990s (excepting production decreases following the economic crisis of 1997 and the attacks of 9/11). Thus,

"...AND DEMAND IS INCREASING..."

Oil demand has indeed been increasing for years, and not just in places like China and India but also in the West... until very recently. The subprime mortgage debacle and the record high oil prices that started late last year obviously contributed to the economic slowdown, and the financial crisis that slammed Wall Street this Fall now looks to keep us firmly in a recession. Also, recent news of China facing major cuts in industrial production suggests we won't see global oil demand growth for some time. Thus,

"...WHY IS THE PRICE OF OIL COLLAPSING?"

It's pretty clear that if global oil production is levelling off but still increasing slightly, and global oil demand is edging downward, we'll have a fall in oil prices.

But that's only part of the picture. The record-high oil prices of last Fall to this summer meant that oil producing countries and oil companies were working overtime to send more oil to market -- both to cash in on the juicily high prices (especially important to the less robust economies of Venezuela, Iran and Russia) and to keep oil from going too high lest it hurt the economies of the consuming nations (especially important to Saudi Arabia).

Fast-forward to Summer 2008: oil prices hit an all-time high of $147 and oil (non-biofuel liquids) production hit an all-time high of just under ~87 mbpd, just as the US was moving into its third quarter of a recession and right before the financial crisis was about to explode on Wall Street. Perfect recipe for a price collapse.

In addition to those supply and demand dynamics, speculation also played a role in the oil price roller-coaster. I recently asked Richard Heinberg his thoughts on this -- here's what he said:

Part of what happened with the oil price spike/collapse was that hedge funds piled on to commodities investments as (a) the value of the dollar was tanking and (b) oil supplies were flat (barely meeting demand), and then dumped commodities when (a) the credit crunch came on strong and they had to cover their losses elsewhere, and (b) the dollar rebounded, as other currencies sank (because their economies were more immediately vulnerable to the credit crisis and everyone wanted a safe monetary haven--and there is still no good alternative to the US dollar for that purpose).

So as usual, the reality of what's going on is significantly more complicated than the simple explanations being tossed around in the media and in the halls of government. Thus,

"IS PEAK OIL STILL RELEVANT?"

(The reader asked "Is peak oil therefore a myth?," but I take this as the gist of the question.)

One of the biggest misconceptions about peak oil is that it is a prediction about the world's oil supply. The peak oil concept actually has more to do with the flow of oil to the global market, as discussed above.

The peak oil concept is useful because it cuts through short-term supply and demand variables to the underlying physical and economic realities of oil production. And the basic reality (from an economic view) is this:

That reality should be fairly obvious for the long term perspective: while we can extract ever more technologically challenging oil deposits at $300 or even $500 per barrel, at such cost and price levels other energy sources will look a lot more attractive.

For the short term perspective, however, that reality is less obvious -- which is partly why we hear much more in the news about big new finds of oil (almost always unconventional and increasingly expensive to produce) than about impending permanent decline, i.e. peak.

Here's where the distinction between conventional and unconventional oil is important. More unconventional oil becomes unprofitable to produce as the price of oil falls; $80 is a commonly cited cutoff point for some of the big tar sands projects, for example. Sure enough, we've heard reports of tar sands projects and even refinery projects being shelved or delayed since oil plummeted below $100 a few months ago.

Now, remember that unconventional oil isn't just a tap that we can turn on and off. It's 'unconventional' precisely because it's logistically more difficult to produce than regular oil. Putting a bunch of oil derricks on the Oklahoma flatlands is peanuts compared to developing a multi-billion dollar, state-of-the-art deepwater project that can extract oil from below many thousands of feet of ocean and seabed, and requires a small army of highly-trained engineers and geologists to operate. Some of the big deep-sea projects can take from six to nine years from discovery to regular production.

Now, remember that unconventional oil isn't just a tap that we can turn on and off. It's 'unconventional' precisely because it's logistically more difficult to produce than regular oil. Putting a bunch of oil derricks on the Oklahoma flatlands is peanuts compared to developing a multi-billion dollar, state-of-the-art deepwater project that can extract oil from below many thousands of feet of ocean and seabed, and requires a small army of highly-trained engineers and geologists to operate. Some of the big deep-sea projects can take from six to nine years from discovery to regular production.

So when these unconventional oil projects get shelved because prices are falling, they're not going to suddenly start producing oil immediately when prices go back up. Meanwhile, we keep drawing on the world's supply of conventional oil -- which pretty much everyone agrees is very near peak since discoveries of conventional oil peaked back in the 1960s. When demand does rise again and prices go up, there'll be that much less conventional oil available and the unconventional oil won't necessarily be there to step in right away.

Indeed, some commentators have said that peak oil will turn out to have been July 2008 at ~87 mbpd, for the simple reason that by the time the global economy demands more than 87 mbpd it'll be prohibitively expensive to deliver that much, and both demand and 'supply' (flow) will be forced back down. Thus,

I've left out any discussion of how the current low oil prices will delay much-needed changes in consumption and efficiency, as well as current thinking on likely oil production decline rates (see the quote below for a snippet), but overall I hope this answers the question. And thank you, William, for asking it! We always welcome comments on our newsletters and articles (although I can't promise to write a lengthy blog post in response to each one).

For further reading on the data and other details, I highly recommend ASPO-USA's Peak Oil Weekly Reviews and the monthly Oilwatch by Rembrandt on The Oil Drum.

A parting thought from Tom Whipple from the December 1st edition of Peak Oil Weekly Review:

It is starting to dawn on many that, should oil prices and demand remain low for an extended period, new investment in oil production will fall to such an extent that, with worldwide depletion, now thought to be in the range of 5 to 6 percent a year, there simply will not be enough new oil to power an economic recovery.

{kind=link}

{kind=link}

{kind=link}

{kind=link}